Canadian Consumer Debt Continues to Grow Despite Macroeconomic Relief

Key findings from TransUnion report:

- Despite stabilization of macroeconomic conditions, total consumer debt and delinquency rates continue to rise

- Gen Z consumers continue to drive credit market activity

- Credit card balances hit new milestone of $124 billion and delinquency rates rise even as average monthly card spend declines

TORONTO, Feb. 19, 2025 (GLOBE NEWSWIRE) -- Total consumer debt in Canada hit a historic high of $2.5 trillion as outstanding balances across all credit products grew by 4.5% year-over-year (YoY) in Q4 2024, according to TransUnion's Q4 2024 Credit Industry Insights Report (CIIR). Balances grew due to a combination of increases in both mortgage debt and non-mortgage debt. Non-mortgage debt increased 5.8% YoY with balances continuing to rise across revolving products in Q4 2024. Line of credit balances grew 4.2%, while credit card balances continued a more rapid pace of growth, increasing 9.2%. Although the rate of growth has been slowing, the overall increase remains significant.

Credit participation grew by 2.5% YoY, with 32.3 million Canadians holding at least one open credit product, a trend fueled in part by the recent decline in interest rates and inflation. Millennial and Gen Z consumers were at the forefront of this increase, collectively holding $1.1 trillion in outstanding balances, a 10% rise YoY. Gen Z consumers were the fastest-growing segment, with a 29% increase in credit participation as they diversify their debt beyond credit card debt.

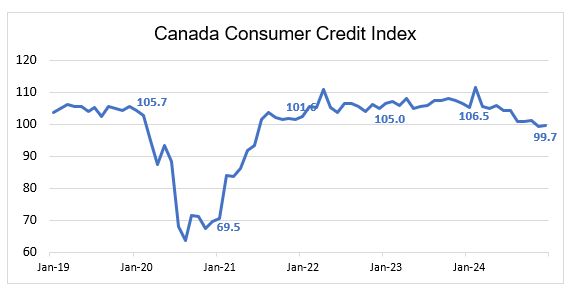

Canada Consumer Credit Index Hits Lowest Level Since 2021

The Canada Consumer Credit Index fell YoY to 99.8 in Q4 2024, its lowest December level since 2020. The decline indicates a deterioration in the overall health of the Canadian retail credit market, reflecting declining consumer behaviours and weakening market conditions. Although all elements of the index were lower than the prior years' values, slowing balances, declining demand and continued increase in delinquency rates were the strongest drivers of the decline.

Credit Card Market Growth Slowing

Credit card balances continued to grow, marking 31 months of consecutive YoY balance growth. However, this growth has moderated in recent quarters, indicating a stabilization in the market may be expected in 2025.

Bankcard originations trended lower in recent quarters, though totals remained elevated in comparison to pre-2018 levels. The recent decline in origination totals was seen across most risk tiers, with subprime leading the decline, influenced by the decrease in new Canadians entering the market after a significant reduction in immigration volume.

In an effort to manage delinquency rates, lenders have become more conservative within their risk tier targets at origination. Overall, bankcard originations dropped by 3.7% YoY, with the largest decline led by subprime at 6.9% YoY, while prime and near prime consumers grew by 3.7% and 0.4% respectively. The risk mix of originated bankcard accounts and credit lines remains consistent with 2018 and 2019 levels, indicating market moderation, metric stabilization and reversion to more familiar business cycles.

Originations growth fell across all generations. Gen Z showed the least year-over-year impact, remaining relatively flat at a decline of only 0.1% from prior year as more young adults in this generation continue to enter the credit market each year. The remaining generations saw a significant drop off from prior years, as demand in these groups for additional credit may have waned as the economy improved.

| Year-over-Year Card Origination by Generation | ||||

| Q3'22 - Q3'23 | Q3'23 - Q3'24 | |||

| Baby Boomer | 6.2% | -9.0% | ||

| Gen X | 9.3% | -6.8% | ||

| Gen Y/Millennial | 11.6% | -2.9% | ||

| Gen Z | 28.5% | -0.1% | ||

Lower inflation in recent quarters, combined with continued employment resiliency for consumers, may be driving consumers towards an improved financial health, where they balance their monthly expenses and monthly budgets. Reduced lender appetite may also play a role in this slowdown, resulting in a decrease in new credit card originations. However, despite the slowing of originations, credit card balance growth remained strong, up 9% YoY, though below the previous year's 13% growth. The growth fueled a new balance milestone of $124 billion in Q4 2024. This was driven by higher revolving balances as consumers paid down a smaller portion of their balances. Approximately 64% of outstanding balances were revolving in Q4 2024 (+157 bp YoY) indicating that consumers are increasingly carrying balances on their cards from month to month.

Average credit card debt per borrower hit $4,681 in Q4, but has also been slowing relative to prior years, with average debt per borrower rising 6.0% YoY in Q4 2024 as opposed to 7.2% the year prior. Prime and below risk segments are increasingly tapping into their available credit, highlighting potential pockets of growing financial needs and a greater dependence on revolving debt to cover daily expenses.

Despite positive economic indicators, including lower interest rates boosting home-related purchases, ongoing economic uncertainty, and high prices for goods and services have continued to weigh on consumer spending decisions. There has been a corresponding drop-off in average monthly card spend, which fell 2.6% from prior year. Overall pressure on consumers related to the higher costs of living and lower savings rates contributed to a rise in bankcard delinquency rates. Bankcard serious consumer-level delinquency levels, defined as 90 or more days past due (DPD), continued to climb higher to 0.93% in Q2 2024, up 9 bps YoY.

"In an environment where new account growth is slowing, credit card issuers need to focus on optimizing account management strategies," said Matthew Fabian, director of financial services research and consulting at TransUnion Canada. "Strengthening customer loyalty, fostering prudent balance growth and engaging younger consumers to enhance lifetime value are crucial. Equally important is vigilant monitoring for early warning signs of rising delinquencies."

| Credit Card Lending Metric (Bankcard) | Q4 2024 | Q4 2023 | Q4 2022 |

| Number of Credit Cards (millions) | 50.8 | 47.6 | 44.5 |

| New Card Originations (millions)* | 1.8 | 1.9 | 1.7 |

| Average New Card Credit Limit* | $5,963 | $5,771 | $5,688 |

| Total Credit Card Balances (Market) in $ billions | $124.7 | $114.2 | $100.9 |

| Average Card Balance per Consumer | $4,681 | $4,430 | $4,076 |

| Average Credit Limit Per Consumer | $19,124 | $17,973 | $16,969 |

| Average Monthly Spend | $2,136 | $2,193 | $2,137 |

| Consumer-Level Delinquency Rate (90+ DPD) | 0.93% | 0.84% | 0.75% |

* Acquisition results are presented one quarter in arrears

Non-Bankcard Delinquencies Also Increase Despite Economic Improvements

The current economic landscape is unique in that, despite relatively stable employment, there has been a rise in consumer loan delinquency rates. Solid employment has been offset by high interest rates that have put pressure on consumer wallets.

Overall serious consumer delinquency continues to rise on a year-over-year basis, up 16 basis points to 1.83% and reaching a five-year high, back on par with the pre-pandemic levels. From a demographic perspective, Gen Z consumers are driving high delinquency rates with delinquencies up YoY 26 bps to 2.74% in Q4 2024. Gen Z credit consumers generally have lower risk scores as they are new to credit and have a shorter lending history. They may also be feeling a greater impact from inflation and the high cost of living, which may strain their budgets. Lenders will need to continue applying advanced analytics to grow and retain this segment, as Gen Z will remain a growing proportion of new credit consumers over the next few years and ultimately will become core credit consumers throughout their lifecycle.

YoY Growth in delinquency by Cohort and Risk Segment Q4 2023 – Q4 2024 (bps) | ||||

| Baby Boomer | Gen X | Millennial | Gen Z | |

| Subprime | 91 | 134 | 114 | 189 |

| Near Prime | 11 | 12 | 9 | 14 |

| Prime | 3 | 4 | 2 | 1 |

"As the Canadian credit market expands, Gen Z consumers present a significant growth opportunity for lenders, especially through tailored credit card offerings," Fabian said. "Gen Z are educated and active credit users with a growing propensity to utilize credit throughout their lifecycle. Early management is crucial, as credit cards can be a valuable financial tool for Gen Z when managed responsibly. By implementing strategies such as education and regular credit monitoring, credit cards can become an asset rather than a financial burden for Gen Z consumers, creating loyalty to lenders who provide those services."

** All data is sourced from the TransUnion Canada consumer credit database.

About TransUnion® (NYSE:TRU)

TransUnion is a global information and insights company with over 13,000 associates operating in more than 30 countries, including Canada, where we're the credit bureau of choice for the financial services ecosystem and most of Canada's largest banks. We make trust possible by ensuring each person is reliably represented in the marketplace. We do this by providing an actionable view of consumers, stewarded with care.

Through our acquisitions and technology investments we have developed innovative solutions that extend beyond our strong foundation in core credit into areas such as marketing, fraud, risk and advanced analytics. As a result, consumers and businesses can transact with confidence and achieve great things. We call this Information for Good® — and it leads to economic opportunity, great experiences and personal empowerment for millions of people around the world.

For more information visit: www.transunion.ca

For more information or to request an interview, contact:

Contact: Katie Duffy

E-mail: [email protected]

Telephone: +1 647-772-0969

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f4b9eec1-e70c-45bf-8e6d-7144f3adbf3d

![]()