Office Real Estate Market Braces For Tough Times As $540 Billion Debt Repayment Looms In 2024

The office real estate market has entered a challenging year, grappling with significant challenges represented by disruptive industry trends and upcoming financial maturities.

As highlighted by recent data from Trepp, an astounding $2.77 trillion of commercial real estate debt, accounting for half of all outstanding commercial real estate debt, is set to mature between 2023 and 2027. Of this, nearly $500 billion is due in 2024 alone.

This looming maturity cliff, coupled with declining property values and high-for-longer interest rates, presents a daunting challenge for both lenders and borrowers in refinancing this volume of debt.

Commercial Mortgage Maturities by Lender Type

| Year | Total Due ($ Billion) | Banks ($ Billion) | CMBS ($ Billion) | Life Cos ($ Billion) | GSE ($ Billion) | Other ($ Billion) |

|---|---|---|---|---|---|---|

| 2023 | $541.2 | $270.4 | $107.7 | $42.5 | $58.4 | $62.2 |

| 2024 | $544.3 | $277.2 | $81.7 | $46.7 | $68.9 | $69.7 |

| 2025 | $533.2 | $283.1 | $53.3 | $49.1 | $82.3 | $65.3 |

| 2026 | $561.4 | $298.3 | $40.7 | $52.3 | $102.3 | $67.9 |

| 2027 | $602.0 | $313.8 | $40.7 | $55.9 | $120.4 | $71.2 |

| 2028 | $565.9 | $293.3 | $35.7 | $57.1 | $113.3 | $66.5 |

| Total (2024-2028) | $2,806.7 | $1,465.8 | $252.1 | $261.1 | $487.2 | $340.5 |

Office Real Estate Industry Confronts Major Hurdles

Dr. Stephen Buschbom, the research director at Trepp, stated in a recent note that higher interest rates and tighter liquidity created significant challenges for new transactions and refinancing maturing loans. He compared the current situation in the commercial real estate (CRE) and CRE debt markets to past economic cycles.

“Maybe the office delinquency rate hits 7%, and I think if you're talking about urban office, non-defeased, that still is a reality,” he wrote.

Buschbom noted an increase in loan modifications and creative capital structuring, expressing hope for a potential decrease in rates later in the year.

However, the expert also highlighted additional complications that may arise from banking regulations and geopolitical risks, potentially restricting liquidity further.

“The fact that you are seeing heavily discounted office transactions in San Francisco at least tells me that — if somebody is willing to start catching what we’re all calling a falling knife, whether or not you think they’re going to get cut, still speaks to where we’re at in the real estate cycle,” Buschbom stated.

Fed Beige Book’s Warnings

The latest Fed Beige Book, which provides qualitative economic assessments, revealed suppressed commercial real estate transactions in the Kansas City district. Moreover, the report stated that “CRE loan modification activity was inhibited by lenders’ concerns about credit performance and borrower liquidity.”

Lauren Hochfelder, co-CEO of Morgan Stanley Real Estate, recently shared in a Bloomberg interview that after two years of sluggishness in the commercial real estate markets, specific factors are bringing back buyers and sellers into the waters, though some are smoother than others.

Amidst the changing landscape of global supply chains, Morgan Stanely noted the resurgence of reshoring to the U.S. and friend-shoring has generated demand for warehouses, particularly along the Mexican border, where construction activity is thriving. Additionally, healthcare is showing promise as people allocate more resources to it, resulting in positive trends in medical and life sciences offices.

However, there are also choppy areas in the commercial real estate market, characterized by an oversupply of properties and excessive debt, as indicated by Hochfelder.

CRE Stocks On The Decline

While last quarter there was initial optimism for rate cuts in 2024 to provide relief to the real estate sector, the year’s start challenged these expectations.

U.S. economic strength and rising global instability factors led Fed members to reconsider early rate cut hopes. The probability of a March rate cut, as implied by the market, dropped from 73% to 57% in just one week, according to CME Group Fed Watch.

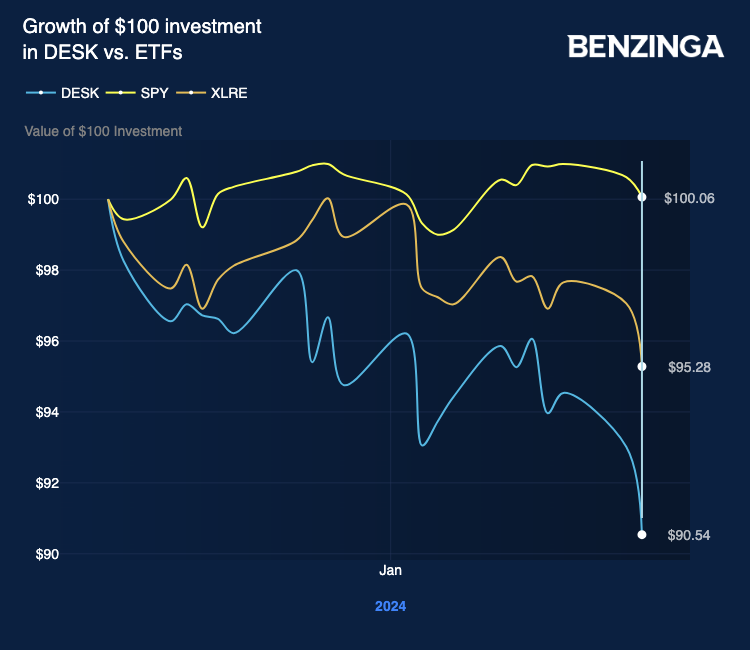

In response to these challenges, stocks in the office real estate sector, as followed by the VanEck Office and Commercial REIT ETF (NYSE:DESK), declined by 10% from their late December peak.

The chart presented below shows that this segment of the market has not only underperformed in comparison to the SPDR S&P 500 ETF Trust (NYSE:SPY) but also relative to the broader real estate sector, as indicated by the Real Estate Select Sector SPDR Fund (NYSE:XLRE).

Worst-Performing CRE Stocks Year-To-Date

| Company Name | Stock price (USD) | Return (%) |

|---|---|---|

| Office Properties Income Trust (NYSE: OPI | 3.65 | -50.14 |

| Orion Office REIT Inc. (NYSE: ONL) | 5.03 | -12.06 |

| Hudson Pacific Properties, Inc. (NYSE:HPP) | 8.29 | -10.96 |

| Paramount Group, Inc. (NYSE:PGRE) | 4.69 | -9.28 |

| Vornado Realty Trust (NYSE:VNO) | 25.89 | -8.35 |

| Kimco Realty Corporation (NYSE:KIM) | 19.93 | -6.50 |

Read Now: How to Invest in Real Estate Online

Photo: Jason Dent on Unsplash