UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to __________

Commission File Number

(Exact name of Registrant as specified in its Charter)

British Columbia, (State or other jurisdiction |

| (IRS Employer |

(Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Exchange Act:

Title of Each Class |

| Trading Symbol(s) |

| Name of Each Exchange on Which Registered |

Securities registered pursuant to Section 12(g) of the Act: Common Shares, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

| ☐ |

| Accelerated filer |

| ☐ | |

| ☒ |

| Small reporting company |

| |||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of the shares of common shares on The Nasdaq Stock Market on the last business day of the registrant’s most recently completed second fiscal quarter 2023, was $

The registrant had

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement relating to the 2024 Annual Meeting of Shareholders, to be filed within 120 days of the Registrant’s fiscal year ended December 31, 2023, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

i

EXPLANATORY NOTE

Unless the context otherwise indicates, references to the “Company,” “Perpetua Resources,” “Perpetua,” “we,” “us,” or “our” in this Annual Report refer to Perpetua Resources Corp. and its subsidiaries and the “Corporation” refers only to Perpetua Resources Corp.

See the “Glossary of Technical Terms” for more information regarding some of the terms used in this Annual Report.

CURRENCY AND EXCHANGE RATE INFORMATION

Unless otherwise indicated, references herein to “US$”,”$” or “dollars” are expressed in U.S. dollars . References in this Annual Report to Canadian dollars are noted as “C$.” Our consolidated financial statements that are included in this Annual Report are presented in U.S. dollars, unless otherwise stated.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report are “forward-looking statements” within the meaning of “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”) and “forward-looking information” within the meaning of applicable Canadian securities laws. All statements, other than statements of historical fact included in this Annual Report, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this Annual Report, the words “anticipate,” “believe,” “expect,” “estimate,” “intend,” “plan,” “project,” “outlook,” “may,” “will,” “should,” “would,” “could,” “can,” the negatives thereof, variations thereon and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. Forward-looking statements are based on certain estimates, beliefs, expectations and assumptions made in light of management’s experience and perception of historical trends, current conditions and expected future developments, as well as other factors that may be appropriate.

Forward-looking statements necessarily involve unknown risks and uncertainties, which could cause actual results or outcomes to differ materially from those expressed or implied in such statements. Due to the risks, uncertainties and assumptions inherent in forward-looking information, you should not place undue reliance on forward-looking statements. Factors that could have a material adverse effect on our business, financial condition, results of operations and growth prospects can be found in Item 1A, Risk Factors, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and elsewhere in this Annual Report. These factors include, but are not limited to, the following:

| ● | planned expenditures and budgets and the execution thereof, including the ability of the Company to discharge its liabilities as they become due and to continue as a going concern; |

| ● | access to capital and suitable financing sources to fund the exploration, permitting, development and construction of the Project; |

| ● | permitting timelines and requirements, including with respect to the timing and outcome of the Final Environmental Impact Statement (“FEIS”), the draft Record of Decision, the Final Record of Decision and other permitting processes; |

| ● | the intended environmental and other outcomes of the Fund (as defined below) related to the Nez Perce Tribe’s Clean Water Act (“CWA”) lawsuit, good faith discussions between the Company and the Nez Perce Tribe with respect to future permitting and activities at the Project and the anticipated source of funding of the Company’s payments required under the Settlement Agreement (as defined below); |

| ● | regulatory and legal changes, requirements for additional capital, requirements for additional water rights and the potential effect of proposed notices of environmental conditions relating to mineral claims; |

| ● | analyses and other information based on expectations of future performance and planned work programs; |

| ● | possible events, conditions or financial performance that are based on assumptions about future economic conditions and courses of action; |

| ● | assumptions and analysis underlying our mineral reserve estimates and plans for mineral resource exploration and development; |

| ● | timing, costs and potential success of future activities on the Company’s properties, including but not limited to development and operating costs in the event that a production decision is made; |

| ● | potential results of exploration, development and environmental protection and remediation activities; |

| ● | future outlook and goals; |

1

| ● | current or future litigation or environmental liability; |

| ● | global economic, political and social conditions and financial markets, including inflationary pressures and elevated interest rates; |

| ● | changes in gold and antimony commodity prices; |

| ● | our ability to implement our strategic plan and to maintain and manage growth effectively; |

| ● | loss of key executives or inability to hire or retain key executives or employees to support the construction, permitting and operations; |

| ● | labor shortages and disruptions; |

| ● | cyber-attacks and other security breaches of our information and technology systems; and |

| ● | other factors and risks described under the heading “Risk Factors” in Item 1A of this Annual Report. |

Statements concerning mineral resource and mineral reserve estimates may also be deemed to constitute forward-looking information to the extent that such statements involve estimates of the mineralization that may be encountered if a property is developed.

With respect to forward-looking information contained herein, the Company has applied several material factors or assumptions including, but not limited to, certain assumptions as to production rates, operating cost, recovery and metal costs; that any additional financing needed will be available when needed on reasonable terms; that the current exploration, development, environmental and other objectives concerning the Company’s Stibnite Gold Project (the “Project” or “Stibnite Gold Project”) can be achieved and that the Company’s other corporate activities will proceed as expected; that the formal review process under the National Environmental Policy Act (“NEPA”) (including a joint review process involving the United States Forest Service (“USFS” or “Forest Service”), the State of Idaho and other agencies and regulatory bodies) as well as the environmental impact statements will proceed in a timely manner and as expected; payment and other settlement conditions under the final Settlement Agreement filed on August 8, 2023 and approved by the United States District Court for the District of Idaho on October 2, 2023 to resolve the CWA litigation (the “Settlement Agreement”) will proceed on the anticipated timeline and terms, the parties will engage in good faith discussions regarding the Project and the Fund (as defined below), that the Project will receive necessary permits and approvals, that Perpetua will be able to successfully obtain financing for the Project, and that all requisite information will be available in a timely manner; that the current price and demand for gold and other metals will be sustained or will improve; that general business and economic conditions will not change in a materially adverse manner and that all necessary governmental approvals for the planned exploration, development and environmental protection activities on the Project will be obtained in a timely manner and on acceptable terms; and that the continuity of economic and political conditions and operations of the Company will be sustained.

These risks are not exhaustive. Because of these risks and other uncertainties, our actual results, performance or achievement, or industry results, may be materially different from the anticipated or estimated results discussed in the forward-looking statements in this Annual Report. New risk factors emerge from time to time, and it is not possible for our management to predict all risk factors nor can we assess the effects of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in, or implied by, any forward-looking statements. Our past results of operations are not necessarily indicative of our future results. You should not rely on any forward-looking statements, which represent our beliefs, assumptions and estimates only as of the dates on which they were made, as predictions of future events. We undertake no obligation to update these forward-looking statements, even though circumstances may change in the future, except as required under applicable securities laws. We qualify all of our forward-looking statements by these cautionary statements.

2

GLOSSARY OF TECHNICAL TERMS

Conversion Factors

To Convert From |

| To |

| Multiply By |

Feet |

| Metres (m) |

| 0.305 |

Metres |

| Feet (ft) |

| 3.281 |

Miles |

| Kilometres (km) |

| 1.609 |

Kilometres |

| Miles |

| 0.6214 |

Hectares |

| Acres (ac) |

| 2.471 |

Grams |

| Ounces (Troy) (oz) |

| 0.03215 |

Grams/Tonnes |

| Ounces (Troy)/Short Ton (oz/ton) |

| 0.02917 |

Tonnes (metric) |

| Pounds (lbs) |

| 2,205 |

Tonnes (metric) |

| Short Tons (st) |

| 1.1023 |

Grams |

| Ounces (Troy) (oz) |

| 0.03215 |

The following is a glossary of certain terms used in this Annual Report:

Assay means, in economic geology, to analyze the proportions of metal in a rock or overburden sample; to test an ore or mineral for composition, purity, weight or other properties of commercial interest.

CERCLA means Comprehensive Environmental Response, Compensation, and Liability Act, referenced informally as “Superfund.”

CIM means the Canadian Institute of Mining, Metallurgy and Petroleum.

Deposit means a mineralized body which has been physically delineated by sufficient drilling, trenching, and/or underground work, and found to contain a sufficient average grade of metal or metals to warrant further exploration and/or development expenditures; such a deposit does not qualify as a commercially mineable ore body or as containing ore reserves, until final legal, technical, and economic factors have been resolved.

g/t Au means grams of gold per metric tonne of material.

Grade means the amount of valuable metal in each tonne of ore, expressed as grams per tonne (g/t) for precious metals and as percent ()% for antimony.

km means kilometre(s).

m means metre(s) (equivalent to 3.281 feet).

M means million.

Mineralization means the concentration of metals and their chemical compounds within a body of rock.

Mineral Reserve or mineral reserve means an estimate of tonnage and grade or quality of indicated and measured mineral resources that, in the opinion of the qualified person, can be the basis of an economically viable project. More specifically, it is the economically mineable part of a measured or indicated mineral resource, which includes diluting materials and allowances for losses that may occur when the material is mined or extracted.

Mineral Resource or mineral resource means a concentration or occurrence of material of economic interest in or on the Earth’s crust in such form, grade or quality, and quantity that there are reasonable prospects for economic extraction. A mineral resource is a reasonable estimate of mineralization, taking into account relevant factors such as cut-off grade, likely mining dimensions, location or continuity, that, with the assumed and justifiable technical and economic conditions, is likely to, in whole or in part, become economically extractable. It is not merely an inventory of all mineralization drilled or sampled.

Ore means a mineral reserve of sufficient value as to quality and quantity to enable it to be mined at a profit.

3

Ounce or oz means a troy ounce or twenty penny weights or 480 grains and is equivalent to 31.1035 grams.

Oz/t or oz/st means a troy ounce per short ton.

Plan of Restoration and Operations or PRO for a mining project on National Forest Lands is a summary of activities intended or proposed to occur on federal lands. The PRO provides the Forest Service with a list of the proponents’ contact and legal information, name of mining district or mineralized area, surface disturbance map, description of the type and magnitude of proposed operations, estimated timing of activities, and plans for reclamation of disturbed areas during and following mining related activities.

POx means pressure oxidation.

2016 PRO means the PRO that was filed by the Company with the U.S. Forest Service in September 2016.

Sampling means a technique for collecting representative sub-volumes from a larger volume of geological material. The particular sampling method employed depends on the nature of the material being sampled and the kind of information required.

NOTICE REGARDING MINING PROPERTY DISCLOSURE RULES

The material scientific and technical information in respect of the Stibnite Gold Project in this Annual Report, unless otherwise indicated, is based upon information contained in the Technical Report Summary (the “TRS”), dated as of December 31, 2021, and amended as of June 6, 2022, developed for the Stibnite Gold Project in accordance with the mining property disclosure rules specified in Regulation S-K 1300 (“S-K 1300”) promulgated by the U.S. Securities and Exchange Commission (the “SEC”). The TRS summarizes, in accordance with the mining property disclosure rules specified in S-K 1300, the technical report titled “Stibnite Gold Project, Feasibility Study Technical Report, Valley County, Idaho” dated effective December 22, 2020 and issued January 27, 2021 (the “2020 Feasibility Study”), which was prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. These standards differ from the mining property disclosure rules specified in S-K 1300. Accordingly, information concerning mineral deposits from the TRS set forth herein may not be comparable with information made public by companies that report in accordance with NI 43-101.

All disclosure contained in this Annual Report regarding the mineral reserves and mineral resource estimates and economic analysis on the property is fully qualified by the full disclosure contained in the 2020 Feasibility Study and the TRS.

Information of a scientific or technical nature in this Annual Report has been approved by Christopher Dail, AIPG CPG #10596, Exploration Manager for Perpetua Resources Idaho, Inc. and a qualified person (as defined in NI 43-101 and as defined in S-K 1300).

See also “Cautionary Note Regarding Forward-Looking Statements.”

4

PART I

Item 1. Business

Overview

The Corporation was incorporated under the Business Corporations Act (British Columbia) on February 22, 2011 under the name “Midas Gold Corp.” The Corporation changed its name to “Perpetua Resources Corp.” on February 15, 2021.

The Corporation’s head office is located at Suite 201 – 405 South 8th Street, Boise, Idaho, U.S.A. 83702 and its registered and records office is located at Suite 1008 – 550 Burrard Street, Vancouver, British Columbia V6C 2B5.

The Corporation is a development-stage company engaged in acquiring mining properties with the intention of exploring, evaluating and placing them into production, if warranted. Currently, its principal business is the exploration and, if warranted and subject to receipt of required permitting, redevelopment, restoration and operation of the Stibnite Gold Project in Idaho, USA. The Corporation is currently undertaking an extensive permitting process for redevelopment and restoration of the Project.

Mineral exploration and development are expected to constitute the principal business of the Corporation for the coming years. In the course of realizing its objectives, it is expected the Corporation may enter into various agreements specific to the mining industry, such as purchase or option agreements to purchase mining claims and/or joint venture agreements.

The Corporation’s principal mineral project is the Stibnite Gold Project, which contains several gold, silver and antimony mineral deposits. The Corporation’s current focus is to explore, evaluate and potentially redevelop three of the deposits known as the Hangar Flats Deposit, West End Deposit and Yellow Pine Deposit, all of which are located within the Stibnite Gold Project as well as reprocess certain historical tailings located on the Project. These development activities would be undertaken in conjunction with a major restoration program designed to address legacy impacts related to historical mining activities in the Project area.

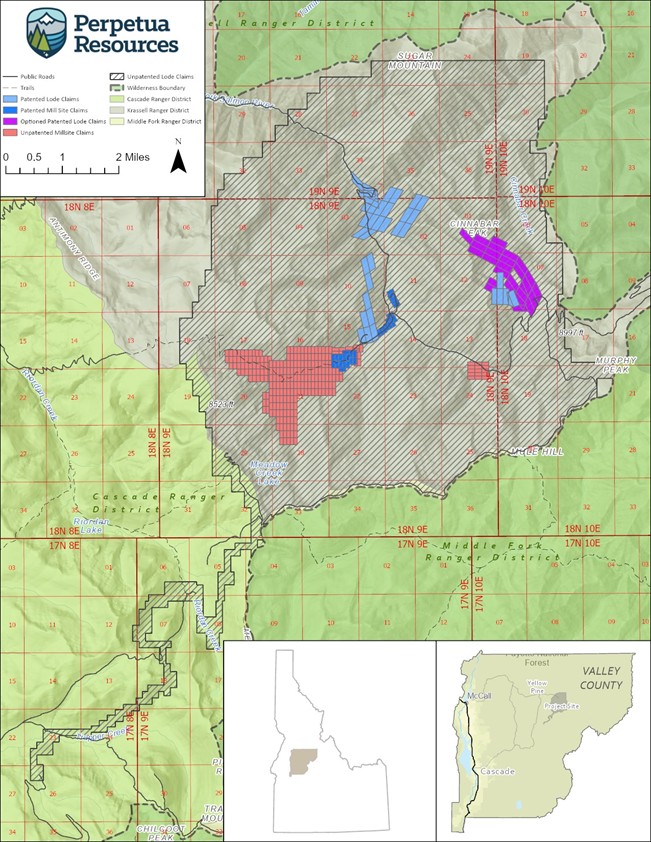

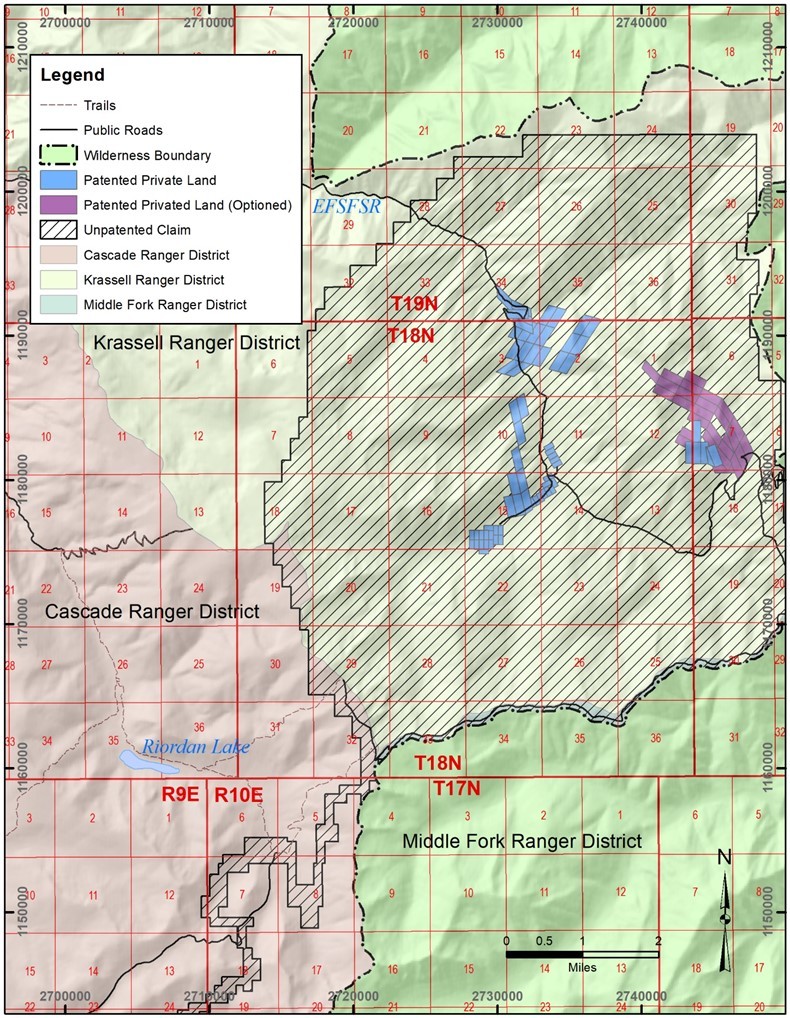

The Corporation’s subsidiaries’ property holdings at the Stibnite Gold Project are comprised of a contiguous package of unpatented federal lode claims, unpatented federal mill sites, patented lode mining claims and patented mill sites. As of December 31, 2023, this land position encompassed approximately 11,548 hectares held in 1,672 unpatented lode claims and mill sites and patented land holdings. A subsidiary of the Corporation acquired these rights through a combination of purchases and transactions and staking under the 1872 Mining Law and holds a portion under an option agreement. Bureau of Land Management claim rental payments and filings are current as of the date of this filing and the claims are all held in good standing. During the years ended December 31, 2022 and December 31, 2023, 53 of the Corporation’s unpatented lode mining claims were relinquished and re-staked with 205 unpatented mill sites over areas non-mineral in character and suitable for mill sites should a development decision be made. Normal maintenance and upkeep of the Project infrastructure continued during the year.

5

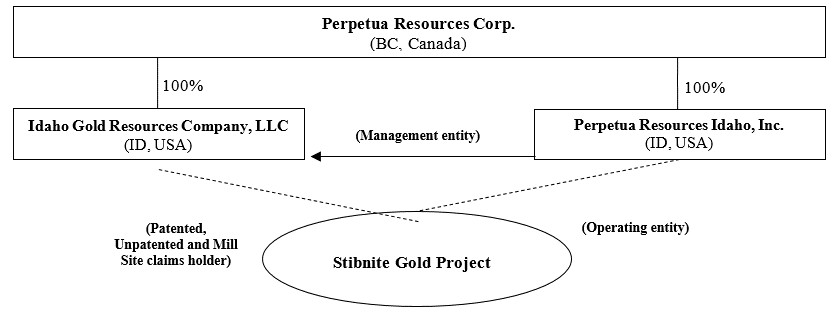

Corporate Structure

The following chart shows the intra-corporate relationships between the Corporation and its subsidiaries. Perpetua Resources Idaho, Inc. (“PRII”) has no ownership interest in the Stibnite Gold Project; rather, it is the designated operating entity and manages the activities on the Project site. The property holding entity, Idaho Gold Resources Company, LLC (“IGRCLLC”), is the surviving entity in a merger with Stibnite Gold Company (“SGC”) effective June 3, 2021 and is managed pursuant to an operating agreement with PRII. PRII and IGRCLLC are wholly owned by the Corporation.

IGRCLLC holds title to the Yellow Pine, Hangar Flats, and West End deposits, all of the patented mill sites and all of the unpatented federal lode mining claims and unpatented mill sites.

Permitting and Environmental Matters

Perpetua Resources focuses on the exploration and mining of the Stibnite Gold Project, the reclamation of prior deposits and historical tailings, and the restoration of the area to address historical activities and legacy contamination. Our project is, therefore, subject to numerous environmental regulations, including federal, state, and local laws. Significantly, we are subject to formal review under NEPA and extensive permitting requirements. In 2016, the Forest Service began its formal review of the Stibnite Gold Project under NEPA. The Forest Service completed scoping in 2017 and subsequently pursuant to the NEPA process, the United States Forest Service and cooperating agencies undertook extensive review of our project and proposed actions through a Draft Environmental Impact Statement (“DEIS”), released by the USFS in August 2020. In response to public and agency feedback on the DEIS, Perpetua Resources proposed modifications to the mine plan analyzed in DEIS Alternative 2 to include reduction of the project footprint, improvements in water quality, and lower water temperatures. Perpetua Resources submitted a refined proposed action to the USFS in December 2020 (the “Modified Mine Plan”).

The USFS then prepared a Supplemental Draft Environmental Impact Statement (“SDEIS”) to further evaluate the project refinements and compare the Company’s proposed site access via Burntlog Route to an alternative option using current roads. After nearly two years of review, the SDEIS was published on October 28, 2022 for a 75-day public comment period. The USFS identified Perpetua Resources’ proposed action, the “Modified Mine Plan,” as the Preferred Alternative and concluded that it would reasonably accomplish the purpose and need for consideration of approval of the Stibnite Gold Project, while giving consideration to environmental, economic, and technical factors. Under NEPA, a “Preferred Alternative” is identified by a Federal agency in a DEIS to let the public know which action the agency is leaning toward selecting as final. However, identification of a “Preferred Alternative” does not represent a final decision and the USFS may still choose various actions based on the Modified Mine Plan or each of the alternatives analyzed in the SDEIS when developing the Final Environmental Impact Statement (“FEIS”).

6

The SDEIS public review period closed on January 10, 2023. On January 1, 2024, the USFS released an updated schedule for the Project. Based on the updated schedule, the Company anticipates that the USFS will publish a FEIS and a Draft Record of Decision in the second quarter of 2024 and a Final Record of Decision (“ROD”) in the fourth quarter of 2024. The publication of the permitting schedule does not indicate any commitments on the part of the USFS regarding the content or timing of a final decision. In developing the FEIS, the USFS may select an action based on components of each of the alternatives analyzed in the SDEIS. Furthermore, the USFS is not bound by the permitting schedule and anticipated milestones may be delayed materially or not be satisfied. We continue to work on obtaining the required ancillary permits in parallel with the agency’s timeline.

Our project is subject to ongoing litigation and could face further litigious challenges in the future. To address historical legacy impacts at the site of the Stibnite Gold Project, Perpetua Resources has voluntarily entered into an Administrative Settlement Agreement and Order on Consent (“ASAOC”) with the United States Environmental Protection Agency (the “U.S. EPA”) and the United States Department of Agriculture, pursuant to the Comprehensive Environmental Response, Compensation, and Liability Act. Finalized on January 15, 2021, the ASAOC provides for a number of time critical removal actions (early cleanup actions) designed to improve water quality in several areas of the site. Upon signing of the ASAOC, the aggregate cost of the obligation was estimated to be approximately $7,473,805. In 2021, 2022 and 2023, the total cost estimate to voluntarily address environmental conditions increased to $17,661,435 due to scope changes, inflation and higher fuel prices. As of December 31, 2023, the corresponding environmental liability was estimated to be $764,607. See also Note 9 to the Consolidated Financial Statements.

Government and Environmental Regulations

Mining operations and exploration activities are subject to extensive national, state, and local laws and regulations in the United States, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances, disclosure requirements and other matters. The Corporation plans to obtain the licenses, permits or other authorizations currently required to conduct its exploration or development programs, and it believes it is currently in material compliance with governing mining, health, safety and environmental statutes and regulations in the United States and Idaho. Except as otherwise noted above, we are not subject to any orders or directions with respect to the foregoing laws and regulations. For a more detailed discussion of the various government laws and regulations applicable to our operations and potential negative effects of these laws and regulations, see section Item 1A, Risk Factors, below.

Our operations are also subject to numerous environmental, health, and safety laws and regulations in the jurisdictions in which we operate. These laws and regulations may require us to take precautions with respect to threatened, endangered, or otherwise protected species and their habitat as well as other natural, historical, and cultural resources, perform environmental assessments or impact statements, implement siting and operational programs or best practices to minimize environmental impacts from our operations, perform investigatory remedial obligations, and obtain federal, state, and local permits, licenses, or other approvals. Failure to comply with these laws and regulations may result in the imposition of significant fines or penalties. Additionally, we could experience significant opposition from third parties to our application for such permits or during the administrative agency review and appeal process after the issuance of such permits. Delays or denial of permits, or the imposition of costly and difficult to comply with conditions, may impair the development of our Project or curtail our planned operations. The following provides a summary of the more significant environmental, health, and safety laws and regulations which our operations are subject to and for which compliance with may have a material adverse impact on our business.

National Environmental Policy Act (“NEPA”)

Our Project is subject to environmental review under NEPA. This law requires federal agencies to evaluate the environmental impact of their actions that may significantly affect the quality of the human environment and is a prerequisite for the granting of a permit or similar authorization for the development of certain projects. As part of the review, the federal agencies are required to consider numerous environmental impacts, such as impacts on air quality, water quality, cultural resources, wildlife, geology, aesthetics, as well as alternatives to the project. The review process can lead to significant delays in approval of such projects and the issuance of the requisite permits which, in turn, can impact both the cost and development of operations. As a result of NEPA review, agencies may decide to deny permits or other support for a project, or condition approvals on certain modifications or mitigation actions. Additionally, authorizations under NEPA are subject to litigation, protest, or appeal, which has the potential to lead to further delays.

7

Pursuant to NEPA, the Forest Service and cooperating agencies undertook additional extensive review of our Project and proposed actions. As a result of this review, a SDEIS was published on October 28, 2022 for a 75-day public comment period which closed on January 10, 2023.

Comprehensive Environmental Response, Compensation, and Liability Act

The site upon which our Project is located has significant legacy contamination. The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) can impose joint and several liability, without regard to fault or legality of conduct, on classes of persons who are statutorily responsible for the release of hazardous substances into the environment. These persons include current owners or operators of a site where a release has occurred. Under CERCLA, such current owners or operators may be subject to strict, joint and several liability for the entire cost of cleaning up hazardous substances and for other expenditures, such as response costs and damage to natural resources. Idaho also has environmental cleanup laws analogous to CERCLA.

Voluntary early cleanup actions can be undertaken pursuant to settlement agreements under CERCLA. We entered into an ASAOC with the U.S. EPA and the United States Department of Agriculture to conduct a number of time critical removal actions focused on improving water quality in several areas of the site.

Protection of Species and Habitat

Our operations are subject to several environmental regulations and guidelines regarding various protected species and their habitats and include the federal Endangered Species Act, the Migratory Bird Treaty Act, and the Bald and Golden Eagle Protection Act, alongside similar state laws. These laws impose significant civil and criminal penalties for violations, including injunctions limiting or otherwise prohibiting operations in certain areas where protected species or their habitat is located. The imposition of such restrictions, such as seasonal limitations, may result in additional costs and delays and could impact the feasibility of our Project.

Clean Water Act

The Clean Water Act (“CWA”) and other similar federal and state laws and regulations may require us to obtain permits for water discharges or take mitigation actions with respect to loss of wetlands. Additionally, such regulations require us to implement a variety of best management practices to ensure that water quality is protected and the impacts of our operations on water quality are minimized. The CWA and analogous laws and regulations provide for administrative, civil and criminal penalties for unauthorized discharges of pollutants in reportable quantities and may impose substantial potential liability for the costs of addressing such discharges.

Mine and Safety Health Administration

Mining operations are regulated by the U.S. Department of Labor’s Mine and Safety Health Administration (“MSHA”) which carries out the provisions of the Federal Mine Safety and Health Act of 1977, as amended by the Mine Improvement and New Emergency Response Act of 2006. MSHA enforces the health and safety rules for all U.S, mines and includes mine inspections regarding compliance with applicable laws and regulations. MSHA has the ability to issue citations and orders and assess penalties for health and safety violations.

District Exploration

No exploration drilling was completed during the reporting period. Activities during the reporting period focused on studies to support permitting and design, engineering and environmental studies to support the ongoing activities related to the ASAOC.

Employees

At December 31, 2023, the Corporation had 33 full time employees and 2 part time employee. 32 employees were directly related to the mineral development activities of the Stibnite Gold Project and the remaining 3 employees were focused on executive management, investor relations and administrative support of the Corporation. A total of 29 employees were employed in Idaho with many of the Perpetua Resources team working remotely. The Corporation also contracts out certain activities with specific skills to assist with various aspects of the Project.

8

Competition

The gold exploration and mining business is a competitive business. The Corporation competes with numerous other companies possessing greater financial and technical research resources. Competition is particularly intense with respect to the acquisition of desirable undeveloped gold properties. In addition, we also encounter competition for the hiring of key personnel. This competition could adversely impact our ability to advance the Project, acquire suitable prospects for exploration in the future on terms we consider acceptable, attract necessary capital funding or acquire an interest in additional properties.

Environmental, Social and Governance (“ESG”)

Our commitment to ESG practices is a core part of our business and has been since our inception, as formalized by our ESG Policy. We seek to guide our operations with responsible and sustainable mining practices and incorporate strong corporate governance values and stakeholder engagement into our business. We engage regularly with key stakeholders and other interested parties, which allows us to better understand their interests, perspectives, and needs. We also believe in both transparency and accountability as key attributes of our governance strategy and seek to deliver information in an open and consistent manner, as denoted by our 2022 Sustainability Report. Our commitment to ESG is also incorporated into our conservation principles which govern the development of our Project and, ultimately, our operations.

Our ESG Policy, Sustainability Roadmap and our 2022 Sustainability Report can be found on the Company’s website. Information on our website is neither part of, nor incorporated into, this Annual Report on Form 10-K.

Availability of Raw Materials

The raw materials we require to carry on our business are readily available through normal supply or business contracting channels in the United States and Canada. Historically, we have been able to secure the appropriate equipment and supplies required to conduct our contemplated programs. As a result, we do not believe that we will experience any shortages of required equipment or supplies in the foreseeable future.

Gold Price History

The price of gold is volatile and is affected by numerous factors, all of which are beyond our control, such as the sale or purchase of gold by various central banks and financial institutions, inflation, recession, fluctuation in the relative values of the U.S. dollar and foreign currencies, changes in global and regional gold demand, in addition to international and national political and economic conditions. The following table presents the annual high, low and average daily afternoon London Bullion Market Association (“LBMA”) gold price over the past five calendar years on the London Bullion Market ($/ounce):

Year |

| High |

| Low |

| Average | |||

2019 |

| $ | 1,546 |

| $ | 1,270 |

| $ | 1,392 |

2020 |

| $ | 2,067 |

| $ | 1,474 |

| $ | 1,770 |

2021 |

| $ | 1,943 |

| $ | 1,684 |

| $ | 1,799 |

2022 |

| $ | 2,039 |

| $ | 1,629 |

| $ | 1,801 |

2023 | $ | 2,078 | $ | 1,811 | $ | 1,943 | |||

2024 (through March 1) |

| $ | 2,078 |

| $ | 1,985 |

| $ | 2,030 |

Data Source: www.kitco.com

Implications of Being an Emerging Growth Company

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”) enacted in April 2012. Certain specified reduced reporting and other regulatory requirements are available to public companies that are emerging growth companies. These provisions include:

| ● | an exemption from the auditor attestation requirement in the assessment of the effectiveness of our internal controls over financial reporting required by Section 404 of the Sarbanes-Oxley Act of 2002; |

| ● | an exemption from the adoption of new or revised financial accounting standards until they would apply to private companies; |

9

| ● | an exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about our audit and our financial statements; and |

| ● | reduced disclosure about our executive compensation arrangements. |

We will continue to be an emerging growth company until the earliest of:

| ● | the last day of our fiscal year in which we have total annual gross revenues of $1.235 billion (as such amount is indexed for inflation every five years by the SEC to reflect the change in the Consumer Price Index for All Urban Consumers published by the Bureau of Labor Statistics, setting the threshold to the nearest $1.0 million) or more; |

| ● | the last day of our fiscal year following the fifth anniversary of the date of our first sale of common equity securities pursuant to an effective registration statement under the Securities Act of 1933 (“Securities Act”); |

| ● | the date on which we have, during the prior three-year period, issued more than $1.0 billion in non-convertible debt; or |

| ● | the date on which we are deemed to be a “large accelerated filer” under the rules of the SEC, which means the market value of our common shares that is held by non-affiliates (or public float) exceeds $700.0 million as of the last day of our second fiscal quarter in our prior fiscal year. |

We have elected to take advantage of certain of the reduced disclosure obligations in this Annual Report and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our shareholders may be different than what you might receive from other public reporting companies in which you hold equity interests.

Available Information

We file or furnish annual, quarterly and current reports, proxy statements and other documents with the SEC under the Exchange Act. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers, including Perpetua, that file electronically with the SEC. We are also subject to requirements of the applicable securities laws of Canada, and documents that we file with the Canadian Securities Administrators may be found at www.sedarplus.ca.

We make available free of charge through our website (www.perpetuaresources.com) our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC or the securities commissions or similar regulatory authorities in Canada. In addition to the reports filed or furnished with the SEC and the securities commissions or similar regulatory authorities in Canada, we publicly disclose information from time to time in our press releases, investor presentations posted on our website and at publicly accessible conferences. Such information, including information posted on or connected to our website, is not a part of, or incorporated by reference in, this Annual Report or any other document we file with or furnish to the SEC or the securities commissions or similar regulatory authorities in Canada.

We have adopted a Code of Conduct and Ethics Policy (the “Code of Conduct”) that applies to our management and to our other employees. We intend to satisfy the disclosure requirement under Item 5.05 of Form 8-K relating to amendments to or waivers from any provision of our Code of Conduct applicable to our principal executive officer, principal financial officer, principal accounting officer and other persons performing similar functions by posting such information on our website (www.perpetuaresources.com). Our other policies and the charters of our Audit, Compensation and Corporate Governance and Nominating Committees are available on our website. Information on our website is neither part of, nor incorporated into, this Annual Report on Form 10-K.

10

Item 1A. Risk Factors.

Investing in our common shares involves a high degree of risk. An investment in our securities is speculative and involves a high degree of risk due to the nature of our business and the present stage of exploration and development of our mineral properties. You should carefully consider the risks described below, as well as the other information in this Annual Report, including our consolidated financial statements and the related notes and Part II, Item 7. entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and in any documents incorporated in this Annual Report by reference, before deciding whether to invest in our common shares. The occurrence of any of the events or developments described below could harm our business, financial condition, results of operations, and growth prospects and could cause them to differ materially from the estimates described in forward-looking statements in this Annual Report. In such an event, the market price of our common shares could decline, and you may lose all or part of your investment. Although we have discussed all known material risks, the risks described below are not the only ones that we may face. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also impair our business operations. Certain statements below are forward-looking statements. See also “Cautionary Note Regarding Forward-Looking Statements” in this Annual Report.

Risks Related to Our Business

Our ability to continue the exploration, permitting, development, and construction of the Project, and to continue as a going concern, will depend in part on our ability to obtain suitable financing.

We have limited financial resources. We will need external financing to develop and construct the Project and to complete the permitting process. Although the Company’s current capital resources and liquidity include up to $24.8 million in funding awarded in December 2022 under the TIA pursuant to Title III of the DPA and an additional $34.6 million conditionally awarded in February 2024, such funding is available only for the specified costs related to permitting, early restoration activities and advancing construction readiness and is not available to fund the Company’s costs pursuant to its ASAOC obligations and certain corporate expenses. The Company’s latest liquidity forecast indicates that available cash resources are expected to be exhausted in the fourth quarter of 2024.We expect to incur other costs in the foreseeable future that are not eligible for DPA funding reimbursement and may incur unanticipated increases to costs under our ASAOC obligations as a result of inflation, fuel or labor costs or other factors. The Company continues to explore various funding opportunities, which may include the issuance of additional equity, new debt, or project specific debt; government funding; and/or other financing opportunities. Although the Company entered into the Sales Agreement with respect to an ATM Offering, sales under the program are subject to certain conditions, including market conditions, and there is no assurance that the Company will be able to raise funds under the program, at acceptable share prices or at all. If additional financing is not secured before the fourth quarter of 2024, the Company would no longer be able to meet its ongoing obligations or progress critical permitting efforts.

Our funding under the TIA is subject to certain conditions, limitations and ongoing obligations. If we fail to satisfy these conditions, we may be unable to obtain all of the funding allocated to Perpetua Resources or may be required to disgorge such funds.

In December 2022, Perpetua Resources was awarded an undefinitized TIA of up to $24.8 million under Title III of the DPA. On July 25, 2023, the TIA was definitized with the DOD, establishing the full not-to-exceed amount of $24.8 million. The TIA contains customary terms and conditions for technology investment agreements, including ongoing reporting obligations. If we fail to satisfy these conditions, we will be unable to obtain remaining funds available under the TIA and, under certain circumstances, could be required to disgorge funds already paid. On February 12, 2024, the Corporation announced a conditional award of up to $34.6 million in additional funding under the TIA. Full funding of the additional award is conditioned on modifying the existing TIA to expand the in-scope work for advancing permits and construction readiness and to extend the outside date to June 30, 2025. The amendment will not change any other material terms of the definitized TIA. The modification is anticipated to be completed in the first quarter of 2024, however, there is no assurance that the Corporation will be able to finalize the amendment on the expected timeline or at all.

Under the funding agreement, Perpetua Resources may request reimbursement for certain costs incurred related to environmental baseline data monitoring, environmental and technical studies and other activities related to advancing Perpetua’s construction readiness and permitting process for the Stibnite Gold Project until December 31, 2024. The funds may be used only for the purposes specified in the TIA and are not available to the Corporation for general corporate purposes other than those specified. Furthermore, the TIA contains limitations on the Corporation’s ability to share or sell certain assets, interests or technology to foreign counterparties, which may limit the Corporation’s ability to raise funding from foreign sources or capitalize on business opportunities with foreign companies.

11

We do not currently have sufficient funds or committed financing necessary to commence construction of the Project, and we may be unable to raise the necessary funds.

Based on the updated schedule published by the USFS in January 2024, the Company anticipates that the USFS will publish a FEIS and a DROD in the second quarter of 2024 and a Final ROD in the fourth quarter of 2024. We have commenced pre-construction engineering and other preparations and, if the DROD and ROD are received on the anticipated schedule, we would seek to commence construction in 2025. According to the TRS, as of December 31, 2020, the total initial capital cost estimate for the Project was approximately $1,263 million. Although we have not updated our capital cost estimates as of December 31, 2023, based on significant inflation and increased financing costs since 2020, we expect the actual cost estimates to be higher than the 2020 estimate. These cost estimates may change materially due to inflation, competition or other unforeseen challenges at the Project site.

We do not currently have sufficient funds or committed financing to commence construction of the Project. Our ability to obtain sufficient funds or committed financing may be impacted by various factors, including, but not limited to, our ability to raise additional funds at acceptable rates or at all; unfavorable interest rates; the incurrence of additional debt, which may be subject to certain restrictive covenants; restrictions on our use of government funding (see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Department of Defense Funding); dilution resulting from additional equity financing (see Item 1A. Risk Factors – Global financial markets can have a profound impact on the global economy in general and on the mining industry in particular); our ability to control certain property as a result of our entry into joint ventures or other similar arrangements; and the loss of certain economic benefits of our property as a result of our entry into royalty agreements.

Our failure to obtain sufficient financing could result in the delay or indefinite postponement of exploration, permitting, development, construction, or production at the Project. The cost and terms of such financing may significantly reduce the expected benefits from development of the Project and/or render such development uneconomic. There can be no assurance that additional capital or other types of financing will be available when needed or that, if available, the terms of such financing will be favorable. Our failure to obtain financing could have a material adverse effect on our growth strategy and results of operations and financial condition.

Perpetua Resources does not have a full staff of technical people and relies upon outside consultants to provide critical services.

Perpetua Resources has a relatively small staff and depends upon its ability to hire consultants with the appropriate background and expertise. Perpetua Resources’ inability to hire the appropriate consultants at the appropriate time could adversely impact Perpetua Resources’ ability to advance its exploration and permitting activities. For example, Perpetua Resources will need to hire additional staff and consultants in order to commence construction of the Project. See section Item 1A, Risk Factors - Perpetua Resources faces substantial competition within the mining industry from other mineral companies with much greater financial and technical resources and Perpetua Resources may not be able to effectively compete.

We have no history of commercially producing precious metals from our mineral properties and there can be no assurance that we will successfully establish mining operations or profitably produce precious metals.

The Project is not in production or currently under construction, and we have no ongoing mining operations or revenue from mining operations. Mineral exploration and development has a high degree of risk and few properties that are explored are ultimately developed into producing mines. The future development of the Project will require obtaining federal and state permits and financing and the construction and operation of mines, processing plants and related infrastructure. As a result, we are subject to all of the risks associated with establishing new mining operations and business enterprises, including, among others:

| ● | The need to obtain necessary environmental and other governmental approvals and permits, and the timing and conditions of those approvals and permits; |

| ● | The potential that future exploration and development of mineral claims on or near the Project site may be impacted by litigation and/or consent decrees entered into by previous owners of mineral rights; |

| ● | The availability and cost of funds to finance construction and development activities; |

| ● | The timing and cost, which can be considerable, of the construction of mining and processing facilities as well as other related infrastructure; |

| ● | Potential opposition from Native American tribes, non-governmental organizations, environmental groups or local groups which may delay or prevent development activities; |

| ● | Potential increases in construction and operating costs due to changes in the cost of labor, fuel, power, materials and supplies, services, and foreign exchange rates; |

12

| ● | The availability and cost of skilled labor and mining equipment; and |

| ● | The availability and cost of appropriate smelting and/or refining arrangements. |

The costs, timing and complexities of mine construction and development are increased by the remote location of the Project, with additional challenges related thereto, including access, water and power supply, and other support infrastructure. Cost estimates may increase significantly as more detailed engineering work and studies are completed. New mining operations commonly experience unexpected costs, problems and delays during development, construction, and mine start-up. In addition, delays in the commencement of mineral production often occur. Accordingly, there are no assurances that our activities will result in profitable mining operations, that we will successfully establish mining operations, or that we will profitably produce precious metals at the Project.

In addition, there is no assurance that our mineral exploration activities will result in any discoveries of new ore bodies. If further mineralization is discovered there is also no assurance that the mineralized material would be economical for commercial production. Discovery of mineral deposits is dependent upon a number of factors and significantly influenced by the technical skill of the exploration personnel involved. The commercial viability of a mineral deposit is also dependent upon a number of factors which are beyond our control, including the attributes of the deposit, commodity prices, government policies and regulation, and environmental protection requirements.

Perpetua Resources’ future exploration and development efforts may be unsuccessful.

Mineral resource exploration and, if warranted, development, is a speculative business, characterized by a number of significant risks, including, among other things, unprofitable efforts resulting not only from the failure to discover mineral deposits but also from finding mineral deposits, which, though present, are insufficient in volume and/or grade to return a profit from production. There is no certainty that the expenditures that have been made and may be made in the future by the Corporation related to the exploration of its properties will result in discoveries of mineralized material in commercially viable quantities.

Most exploration projects do not result in the discovery of commercially viable mineral deposits and no assurance can be given that any particular level of recovery or Mineral Reserves will in fact be realized or that any identified mineral deposit will ever qualify as a commercially viable deposit which can be legally and economically exploited.

Perpetua Resources’ mineral resource and mineral reserve estimates may not be indicative of the actual gold that can be mined.

Assay results from core drilling or reverse circulation drilling can be subject to errors at the laboratory analyzing the drill samples. In addition, reverse circulation or core drilling may lead to samples which may not be representative of the gold or other metals in the entire deposit. Mineral resource and mineral reserve estimates are based on interpretation of available facts and extrapolation or interpolation of data and may not be representative of the actual deposit. In the context of mineral exploration and future development, there is inherent variability between duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. There may also be unknown geologic details that have not been identified or correctly appreciated at the current level of delineation in these types of investigations. This results in uncertainties that cannot be reasonably eliminated from the estimation process. Some of the resulting variances can have a positive effect and others can have a negative effect on mining and processing operations. The calculations of amounts of mineralized material within Mineral Resources and Mineral Reserves are estimates only. Actual recoveries of gold and other potential by-products from Mineral Resources and Mineral Reserves may be lower than those indicated by test work. Any material change in the quantity of mineralization, grade, tonnage or stripping ratio, or the price of gold and other potential by-products, may affect the economic viability of a mineral property. In addition, there can be no assurance that the recoveries of gold and other potential by-products in small-scale laboratory tests will be duplicated in larger scale pilot plant tests under on-site conditions or during production. Notwithstanding the results of any metallurgical testing or pilot plant tests for metallurgy and other factors, there remains the possibility that the ore may not react in commercial production in the same manner as it did in testing.

Mining and metallurgy are an inexact science and, accordingly, there always remains an element of risk that a mine may not prove to be commercially viable. Until a deposit is actually mined and processed, the quantity of Mineral Reserves, Mineral Resources and grades must be considered as estimates only. In addition, the determination and valuation of Mineral Reserves and Mineral Resources is based on, among other things, assumed metal prices. Market fluctuations and metal prices may render Mineral Resources and Mineral Reserves uneconomic. Any material change in quantity of Mineral Reserves, Mineral Resources, grade, tonnage, percent extraction of those mineral reserves recoverable by underground mining techniques or stripping ratio for those Mineral Reserves recoverable by open pit mining techniques may affect the economic viability of a mining project, including the Project and any future operations in which the Corporation has a direct or indirect interest. Any or all of these factors may lead to mineral resource and/or

13

mineral reserve estimates being overstated, the mineable gold that can be received from the Project being less than the mineral resource and mineral reserve estimates, and the Project not being a viable project.

If the Corporation’s mineral resource and mineral reserve estimates for the Project are not indicative of actual grades of gold and other potential by-products, Perpetua Resources will have to continue to explore for a viable deposit or cease operations.

Perpetua Resources faces numerous uncertainties in estimating economically recoverable mineral reserves and mineral resources, and inaccuracies in estimates could result in lower than expected revenues, higher than expected costs and decreased profitability.

Information concerning our mining properties in Item 2, Properties has been prepared in accordance with the requirements of S-K 1300. A mineral is economically recoverable when the price at which it can be sold exceeds the costs and expenses of mining, processing and selling the mineral. Mineral reserve and mineral resource estimates of the gold, silver and antimony in our mining properties are based on many factors, including engineering, economic and geological data assembled and analyzed by internal staff and third parties, which includes various engineers and geologists, the area and volume covered by mining rights, assumptions regarding extraction rates and duration of mining operations, and the quality of in-place mineral reserves and mineral resources. The mineral reserve and mineral resource estimates as to both quantity and quality are updated from time to time to reflect, among other matters, new data received. According to the TRS, as of December 31, 2020, the total initial capital cost estimate for the Project was approximately $1,263 million. The Corporation has not updated its capital cost estimates as of December 31, 2023, however, based on significant inflation and increased financing costs since 2020, the Corporation expects the actual cost estimates to be higher than the 2020 estimate. These cost estimates may change materially due to inflation, competition or other unforeseen challenges at the Project site.

There are numerous uncertainties inherent in estimating quantities and qualities of minerals and costs to mine recoverable mineral reserves and mineral resources, including many factors beyond the Corporation’s control. Estimates of mineral reserves and mineral resources necessarily depend upon a number of variable factors and assumptions, any one of which may, if incorrect, result in an estimate that varies considerably from actual results. These factors and assumptions include, among others:

| ● | Geologic and mining conditions, including the Corporation’s ability to access certain mineral deposits as a result of the nature of the geologic formations of the deposits or other factors, which may not be fully identified by available exploration data; |

| ● | Demand for the Corporation’s minerals; |

| ● | Contractual arrangements, operating costs and capital expenditures; |

| ● | Development and reclamation costs; |

| ● | Mining technology and processing improvements; |

| ● | The effects of regulation by governmental agencies and adverse judicial decisions; |

| ● | The ability to obtain, maintain and renew all required permits; |

| ● | Employee health and safety; and |

| ● | The Corporation’s ability to convert all or any part of mineral resources to economically extractable mineral reserves. |

As a result, actual tonnage recovered from identified mining properties and estimated revenues, expenditures and cash flows with respect to mineral reserves and mineral resources may vary materially from estimates. Thus, these estimates may not accurately reflect the Corporation’s actual mineral reserves and mineral resources. Any material inaccuracy in estimates related to the Corporation’s mineral reserves or mineral resources could result in lower than expected revenues, higher than expected costs or decreased profitability and changes in future cash flow, which could materially and adversely affect the Corporation’s business, results of operations, financial position and cash flows. Additionally, reserve and resource estimates may be adversely affected in the future by interpretations of, or changes to, the SEC’s property disclosure requirements for mining companies.

Perpetua Resources has a history of net losses and expects losses to continue for the foreseeable future.

We have a history of net losses and we expect to incur net losses for the foreseeable future. The Project has not advanced to the commercial production stage and we have no history of earnings or cash flow from operations. We expect to continue to incur net losses unless and until such time the Project commences commercial production and generates sufficient revenues to fund continuing operations. The development of our mineral properties to achieve production will require the commitment of substantial financial resources. The amount and timing of expenditures will depend on a number of factors, including the progress of ongoing exploration and development, the results of consultants’ analyses and recommendations, the rate at which operating losses are incurred, the process

14

of obtaining required government permits and approvals, responding to opposition to the Project, including potential litigation, the availability and cost of financing, the participation of our partners, and the execution of any sale or joint venture agreements with strategic partners. These factors, and others, are beyond our control. There is no assurance that we will be profitable in the future.

We have a limited property portfolio.

At present, our only material mineral property is the interest that we hold through our subsidiary in the Project. Unless we acquire or develop additional mineral properties, we will be solely dependent upon this property. If no additional mineral properties are acquired by us, any adverse development affecting our operations and further development at the Project may have a material adverse effect on our financial condition and results of operations.

We are subject to NEPA review and may be unable to obtain or retain necessary permits which could adversely affect our operations.

Our mining and exploration development activities are subject to extensive permitting requirements which can be costly to comply with and involve extended timelines. Specifically, we are subject to NEPA review, a federal process which is presently ongoing. Formal review under NEPA is extensive and involves several actions, including public scoping, coordination with cooperating agencies, the release of environmental impact statements followed by public comment, potential administrative objections, and the issuance of a final record of decision. Delays in the NEPA process, such as we are unable to timely obtain a record of decision from the United States Forest Service or fail to obtain requisite ancillary permits, may adversely impact our operations. Additionally, to the extent that we are granted necessary permits, we may be subject to a number of Project requirements or conditions including the installation or undertaking of programs to safeguard protected species and their habitat, sites, or otherwise limit the impacts of our operations. Previously obtained permits may be suspended or revoked for a variety of reasons. While we strive to comply with and conclude the NEPA review process, and obtain and comply with all necessary permits and approvals, any failure to do so may have negative impacts upon our business or financial condition, such as increased delays, curtailment of our operations, increased costs, implementation of mitigation or remediation requirements, the potential for litigation or regulatory action, and damage to our reputation.

We are subject to extensive environmental laws and regulations, where compliance failure may impact our operations.

Our mining, exploration, and development operations are subject to extensive environmental, health, and safety laws and regulations in the jurisdictions in which we operate and include those relating to the discharge and remediation of materials in the environment, waste management, and natural resource protection and preservation. Numerous governmental authorities, such as the U.S. EPA, and analogous state agencies, have the authority to enforce compliance with these laws and regulations and the permits issued thereunder, oftentimes requiring difficult and costly response actions. Certain environmental laws, such as CERCLA, impose strict, joint and several liability for costs required to remediate and restore sites where hazardous substances have been stored or released, including sites subject to legacy contamination. We may be required to remediate contaminated properties currently owned and operated by us regardless of whether such contamination resulted from our actions or from the conduct of others. Additionally, claims for damages to persons or property, including damages to natural resources, may result from the environmental, health, and safety impacts of our operations.

We may incur substantial costs to maintain compliance with environmental, health, and safety laws and regulations and such costs could increase if existing laws and regulations are revised or reinterpreted or if new laws or regulations become applicable to our operations. Failure to comply with these environmental, health, and safety laws and regulations may result in the imposition of restrictions on our operations, administrative civil or criminal liabilities, injunctions, third-party property damage or personal injury claims, investigatory cleanup or other remedial obligations, or other adverse effects on our business, financial condition, or operations. Current and future legislative, regulatory, and judicial action could result in changes to operating permits, material changes in operations, and increased capital and operating expenditures, among others.

Our operations are also subject to extensive laws and regulations governing worker health and safety and require us to ensure our employees receive adequate training and guidance to follow applicable environmental, health, and safety policies, procedures, and programs. Failure to comply with applicable legal requirements may cause us to incur significant legal liability, penalties, or fines, result in reputational damage, and negatively impact our employee retention. Our mines will be inspected on a regular basis by government regulators who may issue orders and citations if they believe a violation of applicable mining health and safety laws has occurred. In such cases, we may be subject to fines, penalties, or sanctions, and our operations temporarily shut down. Additionally, future changes in applicable laws and regulations, including more rigorous enforcement, could have an adverse impact on operations and result in increased material expenditures to achieve compliance.

15

Our operations, including permitting, may be subject to legal challenges which could result in adverse impacts to our business and financial condition.

Our mining, exploration, and development operations, and the permits required for such activities, may be subject to legal challenges at the international, federal, state, and local level by various parties. Such legal challenges may allege non-compliance with laws and regulations. For example, in August 2019, the Nez Perce Tribe filed a complaint in the United States District Court for the District of Idaho seeking to hold the Corporation responsible for alleged violations of the CWA through declaratory and injunctive relief. Following the execution of the voluntary ASAOC with the U.S. EPA and the United States Department of Agriculture, the Corporation and the Nez Perce Tribe agreed to stay the litigation and explore alternative dispute resolution through court-ordered mediation. The mediation effort was successful, and the Corporation and the Nez Perce Tribe filed the Settlement Agreement and Stipulation for Dismissal with the United States District Court on August 8, 2023 and the case was dismissed without prejudice on October 2, 2023. Under the Settlement Agreement, a dismissal with full prejudice will follow after completion of our required payments. Once we have satisfied our payment obligations under the Settlement Agreement, the parties will submit a Stipulation of Dismissal with Prejudice to the court.

Legal challenges such as described may result in adverse impacts to our planned operations such as increased defense costs, the performance of additional mitigation and remedial activities, or significant delays to our Project. We may also be subject to more localized opposition, including efforts by environmental groups, which could attract negative publicity or have an adverse impact on our reputation.

Additionally, our Project is located in a district with significant impacts from legacy mining operations prior to our acquisition of and tenure at the sites. Pursuant to CERCLA, we may be subject to liability and remediation responsibilities as current owners of certain areas of the sites under applicable law, consent decrees or similar agreements.

Our operations are subject to climate change risks.

Climate change may result in various and presently unknown physical risks, such as the increased frequency or intensity of extreme weather events or changes in meteorological and hydrological patterns that could adversely impact our business. Such physical risks may result in damage to our facilities causing our operations to temporarily slow down or come to a stop. Moreover, the physical risks associated with climate change could have financial implications for our business, such as increased capital or operating costs, and additional expenditures to maintain or increase the resiliency of our facilities and implement contingency measures.

Increasing attention to ESG matters and conservation measures may adversely impact our business.

Increasing attention to, and societal expectations on companies to address, climate change and other environmental and social impacts, investor, regulatory and societal expectations regarding voluntary and mandatory ESG-related disclosures may result in increased costs, reduced profits, increased investigations and litigation, negative impacts on our stock price and reduced access to capital.

Moreover, while we may create and publish voluntary disclosures regarding ESG matters from time to time, certain statements in those voluntary disclosures may be based on hypothetical expectations and assumptions that may or may not be representative of current or actual risks or events or forecasts of expected risks or events, including the costs associated therewith. Mandatory ESG-related disclosure is also emerging as an area where we may be, or may become, subject to required disclosures in certain jurisdictions, and any such mandatory disclosures may similarly necessitate the use of hypothetical, projected or estimated data, some of which is not controlled by us and is inherently subject to imprecision. Disclosures reliant upon such expectations and assumptions are necessarily uncertain and may be prone to error or subject to misinterpretation given the long timelines involved and the lack of an established single approach to identifying, measuring and reporting on many ESG matters. Additionally, while we may announce various voluntary ESG targets in the future, due to our status as a development stage company, such targets are aspirational. Also, we may not be able to meet such targets in the manner or on such a timeline as initially contemplated and we cannot guarantee that such targets will improve our ESG profile, including, but not limited to, as a result of unforeseen costs or technical difficulties associated with achieving such results. Further, despite any voluntary actions, we may receive pressure from certain investors, lenders, employees or other groups to adopt more aggressive ESG-related targets or policies, but we cannot guarantee that we will be able to implement such targets because of potential costs or technical or operational obstacles. Furthermore, we could be criticized by various anti-ESG stakeholders for the scope of our ESG-related goals or policies, our strategic choices regarding ESG matters as they may impact our operations now or in the future, or for any revisions to the same, as well as initiatives we may pursue or any public statements we may make. We could be subjected to negative responses by governmental actors (such as anti-ESG legislation or retaliatory legislative or administrative treatment) or

16

consumers (such as boycotts or negative publicity campaigns), which could adversely affect our reputation, business, financial performance, market access and growth.