SEC Form 10-Q filed by Vail Resorts Inc.

$MTN

Services-Misc. Amusement & Recreation

Consumer Discretionary

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended January 31, 2024

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-09614

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

| (Registrant’s telephone number, including area code) | |||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As of March 7, 2024, 37,968,155 shares of the registrant’s common stock were outstanding.

Table of Contents

| PART I | FINANCIAL INFORMATION | Page | ||||||

| Item 1. | Financial Statements (unaudited). | |||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | OTHER INFORMATION | |||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

1

Vail Resorts, Inc.

Consolidated Condensed Balance Sheets

(In thousands, except per share amounts)

(Unaudited)

| January 31, 2024 | July 31, 2023 | January 31, 2023 | ||||||||||||||||||

| Assets | ||||||||||||||||||||

| Current assets: | ||||||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | |||||||||||||||||

| Restricted cash | ||||||||||||||||||||

| Trade receivables, net | ||||||||||||||||||||

| Inventories, net | ||||||||||||||||||||

| Other current assets | ||||||||||||||||||||

| Total current assets | ||||||||||||||||||||

Property, plant and equipment, net (Note 7) | ||||||||||||||||||||

| Real estate held for sale or investment | ||||||||||||||||||||

Goodwill, net (Note 7) | ||||||||||||||||||||

| Intangible assets, net | ||||||||||||||||||||

| Operating right-of-use assets | ||||||||||||||||||||

| Other assets | ||||||||||||||||||||

| Total assets | $ | $ | $ | |||||||||||||||||

| Liabilities and Stockholders’ Equity | ||||||||||||||||||||

| Current liabilities: | ||||||||||||||||||||

Accounts payable and accrued liabilities (Note 7) | $ | $ | $ | |||||||||||||||||

| Income taxes payable | ||||||||||||||||||||

Long-term debt due within one year (Note 5) | ||||||||||||||||||||

| Total current liabilities | ||||||||||||||||||||

Long-term debt, net (Note 5) | ||||||||||||||||||||

| Operating lease liabilities | ||||||||||||||||||||

| Other long-term liabilities | ||||||||||||||||||||

| Deferred income taxes, net | ||||||||||||||||||||

| Total liabilities | ||||||||||||||||||||

Commitments and contingencies (Note 9) | ||||||||||||||||||||

| Stockholders’ equity: | ||||||||||||||||||||

Preferred stock, $ | ||||||||||||||||||||

Common stock, $ | ||||||||||||||||||||

| Additional paid-in capital | ||||||||||||||||||||

| Accumulated other comprehensive loss | ( | ( | ( | |||||||||||||||||

| Retained earnings | ||||||||||||||||||||

Treasury stock, at cost, | ( | ( | ( | |||||||||||||||||

| Total Vail Resorts, Inc. stockholders’ equity | ||||||||||||||||||||

| Noncontrolling interests | ||||||||||||||||||||

| Total stockholders’ equity | ||||||||||||||||||||

| Total liabilities and stockholders’ equity | $ | $ | $ | |||||||||||||||||

The accompanying Notes are an integral part of these unaudited consolidated condensed financial statements.

2

Vail Resorts, Inc.

Consolidated Condensed Statements of Operations

(In thousands, except per share amounts)

(Unaudited)

| Three Months Ended January 31, | Six Months Ended January 31, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net revenue: | |||||||||||||||||||||||

| Mountain and Lodging services and other | $ | $ | $ | $ | |||||||||||||||||||

| Mountain and Lodging retail and dining | |||||||||||||||||||||||

| Resort net revenue | |||||||||||||||||||||||

| Real Estate | |||||||||||||||||||||||

| Total net revenue | |||||||||||||||||||||||

| Operating expense (exclusive of depreciation and amortization shown separately below): | |||||||||||||||||||||||

| Mountain and Lodging operating expense | |||||||||||||||||||||||

| Mountain and Lodging retail and dining cost of products sold | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Resort operating expense | |||||||||||||||||||||||

| Real Estate operating expense | |||||||||||||||||||||||

| Total segment operating expense | |||||||||||||||||||||||

| Other operating (expense) income: | |||||||||||||||||||||||

| Depreciation and amortization | ( | ( | ( | ( | |||||||||||||||||||

| Gain on sale of real property | |||||||||||||||||||||||

Change in estimated fair value of contingent consideration (Note 8) | ( | ( | ( | ( | |||||||||||||||||||

| Loss on disposal of fixed assets and other, net | ( | ( | ( | ( | |||||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Mountain equity investment (loss) income, net | ( | ||||||||||||||||||||||

| Investment income and other, net | |||||||||||||||||||||||

Foreign currency gain (loss) on intercompany loans (Note 5) | ( | ( | |||||||||||||||||||||

| Interest expense, net | ( | ( | ( | ( | |||||||||||||||||||

| Income before provision for income taxes | |||||||||||||||||||||||

| Provision for income taxes | ( | ( | ( | ( | |||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Net income attributable to noncontrolling interests | ( | ( | ( | ( | |||||||||||||||||||

| Net income attributable to Vail Resorts, Inc. | $ | $ | $ | $ | |||||||||||||||||||

Per share amounts (Note 4): | |||||||||||||||||||||||

| Basic net income per share attributable to Vail Resorts, Inc. | $ | $ | $ | $ | |||||||||||||||||||

| Diluted net income per share attributable to Vail Resorts, Inc. | $ | $ | $ | $ | |||||||||||||||||||

| Cash dividends declared per share | $ | $ | $ | $ | |||||||||||||||||||

The accompanying Notes are an integral part of these unaudited consolidated condensed financial statements.

3

Vail Resorts, Inc.

Consolidated Condensed Statements of Comprehensive Income

(In thousands)

(Unaudited)

| Three Months Ended January 31, | Six Months Ended January 31, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Foreign currency translation adjustments, net of tax | ( | ( | |||||||||||||||||||||

| Change in estimated fair value of hedging instruments, net of tax | ( | ( | ( | ||||||||||||||||||||

| Comprehensive income | |||||||||||||||||||||||

| Comprehensive (income) loss attributable to noncontrolling interests | ( | ( | |||||||||||||||||||||

| Comprehensive income attributable to Vail Resorts, Inc. | $ | $ | $ | $ | |||||||||||||||||||

The accompanying Notes are an integral part of these unaudited consolidated condensed financial statements.

4

Vail Resorts, Inc.

Consolidated Condensed Statements of Stockholders’ Equity

(In thousands)

(Unaudited)

| Common Stock | Additional Paid in Capital | Accumulated Other Comprehensive Loss | Retained Earnings | Treasury Stock | Total Vail Resorts, Inc. Stockholders’ Equity | Noncontrolling Interests | Total Stockholders’ Equity | |||||||||||||||||||

| Vail Resorts | ||||||||||||||||||||||||||

| Balance, October 31, 2022 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Comprehensive income: | ||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||

| Foreign currency translation adjustments, net of tax | — | — | — | — | ||||||||||||||||||||||

| Change in estimated fair value of hedging instruments, net of tax | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Total comprehensive income | ||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | |||||||||||||||||||||

| Issuance of shares under share award plans, net of shares withheld for employee taxes | ( | — | — | — | ( | — | ( | |||||||||||||||||||

| Dividends (Note 4) | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Distributions to noncontrolling interests, net | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

| Balance, January 31, 2023 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Balance, October 31, 2023 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Comprehensive income: | ||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||

| Foreign currency translation adjustments, net of tax | — | — | — | — | ||||||||||||||||||||||

| Change in estimated fair value of hedging instruments, net of tax | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Total comprehensive income | ||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | |||||||||||||||||||||

| Issuance of shares under share award plans, net of shares withheld for employee taxes | ( | — | — | — | ( | — | ( | |||||||||||||||||||

| Dividends (Note 4) | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Distributions to noncontrolling interests, net | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

| Balance, January 31, 2024 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

5

| Common Stock | Additional Paid in Capital | Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Treasury Stock | Total Vail Resorts, Inc. Stockholders’ Equity | Noncontrolling Interests | Total Stockholders’ Equity | |||||||||||||||||||

| Vail Resorts | ||||||||||||||||||||||||||

| Balance, July 31, 2022 | $ | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||

| Comprehensive income (loss): | ||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||

| Foreign currency translation adjustments, net of tax | — | — | ( | — | — | ( | ( | ( | ||||||||||||||||||

| Change in estimated fair value of hedging instruments, net of tax | — | — | — | — | — | |||||||||||||||||||||

| Total comprehensive income (loss) | ( | |||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | |||||||||||||||||||||

| Issuance of shares under share award plans, net of shares withheld for employee taxes | ( | — | — | — | ( | — | ( | |||||||||||||||||||

| Dividends (Note 4) | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Cumulative effect of adoption of ASU 2020-06 | — | ( | — | — | ( | — | ( | |||||||||||||||||||

| Estimated acquisition date fair value of noncontrolling interests (Note 6) | — | — | — | — | — | — | ||||||||||||||||||||

| Distributions to noncontrolling interests, net | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

| Balance, January 31, 2023 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Balance, July 31, 2023 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Comprehensive income (loss): | ||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||

| Foreign currency translation adjustments, net of tax | — | — | ( | — | — | ( | ( | ( | ||||||||||||||||||

| Change in estimated fair value of hedging instruments, net of tax | — | — | ( | — | — | ( | — | ( | ||||||||||||||||||

| Total comprehensive income (loss) | ( | |||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | |||||||||||||||||||||

| Issuance of shares under share award plans, net of shares withheld for employee taxes | ( | — | — | — | ( | — | ( | |||||||||||||||||||

Repurchases of common stock (Note 11) | — | — | — | — | ( | ( | — | ( | ||||||||||||||||||

Dividends (Note 4) | — | — | — | ( | — | ( | — | ( | ||||||||||||||||||

| Distributions to noncontrolling interests, net | — | — | — | — | — | — | ( | ( | ||||||||||||||||||

| Balance, January 31, 2024 | $ | $ | $ | ( | $ | $ | ( | $ | $ | $ | ||||||||||||||||

The accompanying Notes are an integral part of these unaudited consolidated condensed financial statements.

6

Vail Resorts, Inc.

Consolidated Condensed Statements of Cash Flows

(In thousands)

(Unaudited)

| Six Months Ended January 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| Cash flows from operating activities: | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Stock-based compensation expense | ||||||||||||||

| Provision for income taxes | ||||||||||||||

| Other non-cash income, net | ||||||||||||||

| Changes in assets and liabilities: | ||||||||||||||

| Trade receivables, net | ||||||||||||||

| Inventories, net | ( | ( | ||||||||||||

| Accounts payable and accrued liabilities | ||||||||||||||

| Deferred revenue | ||||||||||||||

| Income taxes payable | ( | ( | ||||||||||||

| Other assets and liabilities, net | ( | ( | ||||||||||||

| Net cash provided by operating activities | ||||||||||||||

| Cash flows from investing activities: | ||||||||||||||

| Capital expenditures | ( | ( | ||||||||||||

| Return of deposit for acquisition of business | ||||||||||||||

| Acquisition of business, net of cash acquired | ( | |||||||||||||

| Investments in short-term deposits | ( | |||||||||||||

| Maturity of short-term deposits | ||||||||||||||

| Other investing activities, net | ||||||||||||||

| Net cash used in investing activities | ( | ( | ||||||||||||

| Cash flows from financing activities: | ||||||||||||||

| Repayments of borrowings under Vail Holdings Credit Agreement | ( | ( | ||||||||||||

| Employee taxes paid for share award exercises | ( | ( | ||||||||||||

| Dividends paid | ( | ( | ||||||||||||

| Repurchases of common stock | ( | |||||||||||||

| Other financing activities, net | ( | ( | ||||||||||||

| Net cash used in financing activities | ( | ( | ||||||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | ( | ( | ||||||||||||

| Net increase in cash, cash equivalents and restricted cash | ||||||||||||||

| Cash, cash equivalents and restricted cash: | ||||||||||||||

| Beginning of period | ||||||||||||||

| End of period | $ | $ | ||||||||||||

| Non-cash investing activities: | ||||||||||||||

| Accrued capital expenditures | $ | $ | ||||||||||||

The accompanying Notes are an integral part of these unaudited consolidated condensed financial statements.

7

Vail Resorts, Inc.

Notes to Consolidated Condensed Financial Statements

(Unaudited)

1.Organization and Business

Vail Resorts, Inc. (“Vail Resorts”) is organized as a holding company and operates through various subsidiaries. Vail Resorts and its subsidiaries (collectively, the “Company”) operate in three reportable segments: Mountain, Lodging and Real Estate. The Company refers to “Resort” as the combination of the Mountain and Lodging segments.

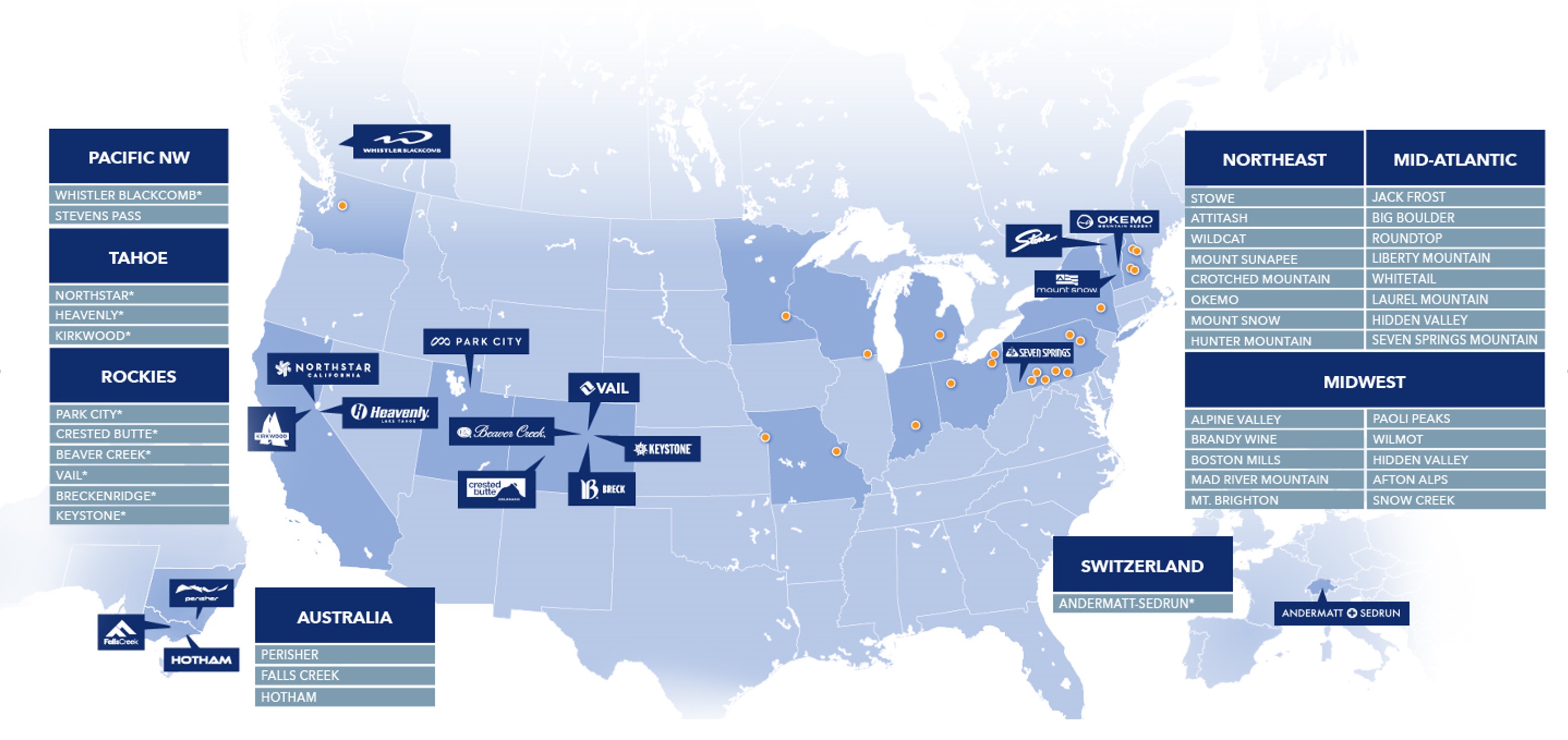

In the Mountain segment, the Company operates the following 41 destination mountain resorts and regional ski areas:

*Denotes a destination mountain resort, which generally receives a meaningful portion of skier visits from long-distance travelers, as opposed to the Company’s regional ski areas, which tend to generate skier visits predominantly from their respective local markets.

Additionally, the Mountain segment includes ancillary services, primarily including ski school, dining and retail/rental operations, and for the Company’s Australian ski areas, including lodging and transportation operations.

In the Lodging segment, the Company owns and/or manages a collection of luxury hotels and condominiums under its RockResorts brand; other strategic lodging properties and a large number of condominiums located in proximity to the Company’s North American mountain resorts; National Park Service (“NPS”) concessioner properties including the Grand Teton Lodge Company, which operates destination resorts in Grand Teton National Park; a Colorado resort ground transportation company and mountain resort golf courses.

The Company’s Real Estate segment primarily owns, develops and sells real estate in and around the Company’s resort communities.

The Company’s mountain business and its lodging properties at or around the Company’s mountain resorts are seasonal in nature, and typically experience their peak operating seasons primarily from mid-December through mid-April in North America and Europe. The peak operating season at the Company’s Australian resorts, NPS concessioner properties and golf courses generally occurs from June to early October.

8

Pending Acquisition of Crans-Montana Mountain Resort

On November 30, 2023, the Company announced that it had entered into an agreement to acquire Crans-Montana Mountain Resort (“Crans-Montana”) in Switzerland from CPI Property Group. Pursuant to the terms of the agreement, the Company will acquire (i) an 84% ownership stake in Remontées Mécaniques Crans Montana Aminona SA, which controls and operates all of the lifts and supporting mountain operations, including four retail and rental locations; (ii) an 80% ownership stake in SportLife AG, which operates one of the ski schools located at the resort; and (iii) 100% ownership of 11 restaurants located on and around the mountain. Subject to closing adjustments, the enterprise value of the resort operations is expected to be CHF 118.5 million. The Company expects to fund the purchase price for the acquired ownership interest of the resort operations through cash on hand when the transaction closes.

2. Summary of Significant Accounting Policies

Basis of Presentation

Use of Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the balance sheet date and the reported amounts of revenue and expenses during the reporting periods. Actual results could differ from those estimates.

Fair Value of Financial Instruments — The estimated fair values of the 6.25% Notes and the 0.0% Convertible Notes (each as defined in Note 5, Long-Term Debt) are based on quoted market prices (a Level 2 input). The estimated fair value of the EPR Secured Notes and the NRP Loan (both as defined in Note 5, Long-Term Debt) have been estimated using analyses based on current borrowing rates for comparable debt instruments with similar maturity dates (a Level 2 input). The carrying values, including any unamortized premium or discount, and estimated fair values of the 6.25% Notes, 0.0% Convertible Notes, EPR Secured Notes and NRP Loan as of January 31, 2024 are presented below (in thousands):

| January 31, 2024 | |||||||||||

| Carrying Value | Estimated Fair Value | ||||||||||

| 6.25% Notes | $ | $ | |||||||||

| 0.0% Convertible Notes | $ | $ | |||||||||

| EPR Secured Notes | $ | $ | |||||||||

| NRP Loan | $ | $ | |||||||||

The carrying values for all other financial instruments not included in the above table approximate their respective fair value due to their short-term nature or the variable nature of their associated interest rates.

Recently Issued Accounting Standards

Standards Being Evaluated

In November 2023, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update (“ASU”) 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures,” which is intended to improve reportable segment disclosures, primarily through incorporating enhanced segment disclosure requirements set forth by the Securities and Exchange Commission into U.S. GAAP. The enhanced disclosures will primarily require public entities to include specific disclosures regarding “significant expenses” that are regularly provided to or easily computed from information provided to the chief operating decision maker (“CODM”) and included within segment profit and loss. This ASU also requires that a public entity disclose the title and position of the CODM and an explanation of how the CODM uses the reported

9

measure(s) of segment profit or loss. ASU 2023-07 is effective for fiscal years beginning after December 15, 2023 (the Company’s fiscal year ending July 31, 2025), and interim periods within fiscal years beginning after December 15, 2024 (the Company’s fiscal quarter ending October 31, 2025), with early adoption permitted. The Company is in the process of evaluating the effect that the adoption of this standard will have on its Consolidated Condensed Financial Statements, including determining the timing of adoption.

In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures,” which includes amendments that further enhance the transparency and decision usefulness of income tax disclosures, primarily through standardization and disaggregation of rate reconciliation categories and income taxes paid by jurisdiction. This update is effective for annual periods beginning after December 15, 2024 (the Company’s fiscal year ending July 31, 2026), though early adoption is permitted. The Company is in the process of evaluating the effect that the adoption of this standard will have on its Consolidated Condensed Financial Statements, including determining the timing of adoption.

3. Revenues

Disaggregation of Revenues

The following table presents net revenues disaggregated by segment and major revenue type for the three and six months ended January 31, 2024 and 2023 (in thousands):

| Three Months Ended January 31, | Six Months Ended January 31, | |||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||

| Mountain net revenue: | ||||||||||||||||||||||||||

| Lift | $ | $ | $ | $ | ||||||||||||||||||||||

| Ski School | ||||||||||||||||||||||||||

| Dining | ||||||||||||||||||||||||||

| Retail/Rental | ||||||||||||||||||||||||||

| Other | ||||||||||||||||||||||||||

| Total Mountain net revenue | $ | $ | $ | $ | ||||||||||||||||||||||

| Lodging net revenue: | ||||||||||||||||||||||||||

| Owned hotel rooms | $ | $ | $ | $ | ||||||||||||||||||||||

| Managed condominium rooms | ||||||||||||||||||||||||||

| Dining | ||||||||||||||||||||||||||

| Transportation | ||||||||||||||||||||||||||

| Golf | ||||||||||||||||||||||||||

| Other | ||||||||||||||||||||||||||

| Payroll cost reimbursements | ||||||||||||||||||||||||||

| Total Lodging net revenue | $ | $ | $ | $ | ||||||||||||||||||||||

| Total Resort net revenue | $ | $ | $ | $ | ||||||||||||||||||||||

| Total Real Estate net revenue | ||||||||||||||||||||||||||

| Total net revenue | $ | $ | $ | $ | ||||||||||||||||||||||

Contract Balances

Deferred revenue balances of a short-term nature were $660.3 million and $572.6 million as of January 31, 2024 and July 31, 2023, respectively. For the three and six months ended January 31, 2024, the Company recognized approximately $238.0 million and $294.5 million, respectively, of revenue that was included in the deferred revenue balance as of July 31, 2023. Deferred revenue balances of a long-term nature, comprised primarily of long-term private club initiation fee revenue, were $108.3 million, $109.7 million and $113.3 million as of January 31, 2024, July 31, 2023 and January 31, 2023, respectively. As of January 31, 2024, the weighted average remaining period over which revenue for unsatisfied performance obligations on long-term private club contracts will be recognized was approximately 15 years.

10

Costs to Obtain Contracts with Customers

Costs to obtain contracts with customers are recorded within other current assets on the Company’s Consolidated Condensed Balance Sheets, and were $14.4 million, $5.1 million and $13.0 million as of January 31, 2024, July 31, 2023 and January 31, 2023, respectively. The amounts capitalized are subject to amortization generally beginning in the second quarter of each fiscal year, commensurate with the recognition of revenue for related pass products. The Company recorded amortization of $13.9

4. Net Income per Share

Earnings per Share

Basic EPS excludes dilution and is computed by dividing net income attributable to Vail Resorts stockholders by the weighted-average shares outstanding during the period. Diluted EPS reflects the potential dilution that could occur if securities or other contracts to issue common stock were exercised, resulting in the issuance of shares of common stock that would then share in the earnings of Vail Resorts.

In connection with the Company’s acquisition of Whistler Blackcomb in October 2016, the Company issued consideration in the form of shares of Vail Resorts common stock (the “Vail Shares”), redeemable preferred shares of the Company’s wholly-owned Canadian subsidiary Whistler Blackcomb Holdings Inc. (“Exchangeco Shares”) or cash (or a combination thereof). Effective September 26, 2022, all Exchangeco Shares had been exchanged for Vail Shares. Both Vail Shares and Exchangeco Shares have a par value of $0.01 per share, and Exchangeco Shares, while they were outstanding, were substantially the economic equivalent of the Vail Shares. The Company’s calculation of weighted-average shares outstanding as of January 31, 2023 included the Exchangeco Shares, but there were no Exchangeco Shares that remained outstanding as of January 31, 2023.

Presented below is basic and diluted EPS for the three months ended January 31, 2024 and 2023 (in thousands, except per share amounts):

| Three Months Ended January 31, | ||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||

| Basic | Diluted | Basic | Diluted | |||||||||||||||||||||||

| Net income per share: | ||||||||||||||||||||||||||

| Net income attributable to Vail Resorts | $ | $ | $ | $ | ||||||||||||||||||||||

| Weighted-average Vail Shares outstanding | ||||||||||||||||||||||||||

| Effect of dilutive securities | — | — | ||||||||||||||||||||||||

| Total shares | ||||||||||||||||||||||||||

| Net income per share attributable to Vail Resorts | $ | $ | $ | $ | ||||||||||||||||||||||

The Company computes the effect of dilutive securities using the treasury stock method and average market prices during the period. The number of shares issuable upon the exercise of share-based awards excluded from the calculation of diluted EPS because the effect of their inclusion would have been anti-dilutive totaled approximately 15,000 and 25,000 for the three months ended January 31, 2024 and 2023, respectively.

11

Presented below is basic and diluted EPS for the six months ended January 31, 2024 and 2023 (in thousands, except per share amounts):

| Six Months Ended January 31, | ||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||

| Basic | Diluted | Basic | Diluted | |||||||||||||||||||||||

| Net income per share: | ||||||||||||||||||||||||||

| Net income attributable to Vail Resorts | $ | $ | $ | $ | ||||||||||||||||||||||

| Weighted-average Vail Shares outstanding | ||||||||||||||||||||||||||

| Weighted-average Exchangeco Shares outstanding | ||||||||||||||||||||||||||

| Total Weighted-average shares outstanding | ||||||||||||||||||||||||||

| Effect of dilutive securities | — | — | ||||||||||||||||||||||||

| Total shares | ||||||||||||||||||||||||||

| Net income per share attributable to Vail Resorts | $ | $ | $ | $ | ||||||||||||||||||||||

The number of shares issuable upon the exercise of share-based awards excluded from the calculation of diluted EPS because the effect of their inclusion would have been anti-dilutive totaled approximately 18,000 and 26,000 for the six months ended January 31, 2024 and 2023 respectively.

In December 2020, the Company completed an offering of $575.0 million in aggregate principal amount of 0.0% Convertible Notes (as defined in Note 5, Long-Term Debt). The Company is required to settle the principal amount of the 0.0% Convertible Notes in cash and has the option to settle the conversion spread in cash or shares. The Company uses the if-converted method to calculate the impact of convertible instruments on diluted EPS when the instruments may be settled in cash or shares. If the conversion value of the 0.0% Convertible Notes exceeds their conversion price, then the Company will calculate its diluted EPS as if all the notes were converted into common stock at the beginning of the period. However, if reflecting the 0.0% Convertible Notes in diluted EPS in this manner is anti-dilutive, or if the conversion value of the notes does not exceed their conversion price for a reporting period, then the shares underlying the notes will not be reflected in the Company’s calculation of diluted EPS. For the three and six months ended January 31, 2024 and 2023, the price of Vail Shares did not exceed the conversion price and therefore there was no impact to diluted EPS during those periods.

Dividends

During the three and six months ended January 31, 2024, the Company paid cash dividends of $2.06 and $4.12 per share, respectively ($78.2 million and $156.7 million, respectively). During the three and six months ended January 31, 2023, the Company paid cash dividends of $1.91 and $3.82 per share, respectively ($77.0 million and $154.0 million), respectively. On March 7, 2024 , the Company’s Board of Directors approved a cash dividend of $2.22 per share payable on April 11, 2024 to stockholders of record as of March 28, 2024 .

12

5. Long-Term Debt

Long-term debt, net as of January 31, 2024, July 31, 2023 and January 31, 2023 is summarized as follows (in thousands):

| Maturity | January 31, 2024 | July 31, 2023 | January 31, 2023 | |||||||||||||||||||||||

Vail Holdings Credit Agreement term loan (a) | $ | $ | $ | |||||||||||||||||||||||

Vail Holdings Credit Agreement revolver (a) | ||||||||||||||||||||||||||

| 6.25% Notes | ||||||||||||||||||||||||||

0.0% Convertible Notes (b) | ||||||||||||||||||||||||||

Whistler Credit Agreement revolver (c) | ||||||||||||||||||||||||||

EPR Secured Notes (d) | ||||||||||||||||||||||||||

| NRP Loan | ||||||||||||||||||||||||||

| Employee housing bonds | ||||||||||||||||||||||||||

| Canyons obligation | ||||||||||||||||||||||||||

| Whistler Blackcomb employee housing leases | ||||||||||||||||||||||||||

| Other | ||||||||||||||||||||||||||

| Total debt | ||||||||||||||||||||||||||

| Less: Unamortized premiums, discounts and debt issuance costs | ||||||||||||||||||||||||||

Less: Current maturities (e) | ||||||||||||||||||||||||||

| Long-term debt, net | $ | $ | $ | |||||||||||||||||||||||

(a)As of January 31, 2024, the Vail Holdings Credit Agreement consists of a $500.0 million revolving credit facility and a $1.0 billion outstanding term loan. The term loan is subject to quarterly amortization of principal of approximately $15.6 million, in equal installments, for a total of 5% of principal payable in each year and the final payment of all amounts outstanding, plus accrued and unpaid interest is due upon maturity in September 2026. The proceeds of the loans made under the Vail Holdings Credit Agreement may be used to fund the Company’s working capital needs, capital expenditures, acquisitions, investments and other general corporate purposes, including the issuance of letters of credit. Borrowings under the Vail Holdings Credit Agreement, including the term loan, bear interest annually at the Secured Overnight Financing Rate (“SOFR”) plus a spread of 1.60 % as of January 31, 2024 (6.93 % as of January 31, 2024). Interest rate margins may fluctuate based upon the ratio of the Company’s Net Funded Debt to Adjusted EBITDA on a trailing four-quarter basis. The Vail Holdings Credit Agreement also includes a quarterly unused commitment fee, which is equal to a percentage determined by the Net Funded Debt to Adjusted EBITDA ratio, as each such term is defined in the Vail Holdings Credit Agreement, multiplied by the daily amount by which the Vail Holdings Credit Agreement commitment exceeds the total of outstanding loans and outstanding letters of credit (0.30 % as of January 31, 2024). The Company is party to various interest rate swap agreements which hedge the cash flows associated with the SOFR-based variable interest rate component of $400.0 million in principal amount of its Vail Holdings Credit Agreement until September 23, 2024, at an effective rate of 1.38 %.

(b)The Company issued $575.0 million in aggregate principal amount of 0.0% Convertible Notes due 2026 (the “0.0% Convertible Notes) under an indenture dated December 18, 2020. As of January 31, 2024, the conversion price of the 0.0% Convertible Notes, adjusted for cash dividends paid since the issuance date, was $377.76 .

(c)Whistler Mountain Resort Limited Partnership (“Whistler LP”) and Blackcomb Skiing Enterprises Limited Partnership (“Blackcomb LP” and together with Whistler LP, the “WB Partnerships”) are party to a credit agreement consisting of a C$300.0 million credit facility which was most recently amended on April 14, 2023, by and among Whistler LP, Blackcomb LP, certain subsidiaries of Whistler LP and Blackcomb LP party thereto as guarantors, the financial institutions party thereto as lenders and The Toronto-Dominion Bank, as administrative agent. The Whistler Credit Agreement has a maturity date of April 14, 2028 and uses rates based on SOFR with regard to borrowings under the facility made in U.S. dollars. As of January 31, 2024, there were no borrowings under the Whistler Credit Agreement. The Whistler Credit Agreement also includes a quarterly unused commitment fee based on the Consolidated Total Leverage Ratio, which as of January 31, 2024 is equal to 0.39 % per annum.

13

(d)In September 2019, in conjunction with the acquisition of Peak Resorts, Inc. (“Peak Resorts”), the Company assumed various secured borrowings (the “EPR Secured Notes”) under the master credit and security agreements and other related agreements, as amended, (collectively, the “EPR Agreements”) with EPT Ski Properties, Inc. and its affiliates (“EPR”). The EPR Secured Notes include the following:

i.The Alpine Valley Secured Note. The $4.6 million Alpine Valley Secured Note provides for interest payments through its maturity on December 1, 2034. As of January 31, 2024, interest on this note accrued at a rate of 11.90 %.

ii.The Boston Mills/Brandywine Secured Note. The $23.3 million Boston Mills/Brandywine Secured Note provides for interest payments through its maturity on December 1, 2034. As of January 31, 2024, interest on this note accrued at a rate of 11.41 %.

iii.The Jack Frost/Big Boulder Secured Note. The $14.3 million Jack Frost/Big Boulder Secured Note provides for interest payments through its maturity on December 1, 2034. As of January 31, 2024, interest on this note accrued at a rate of 11.41 %.

iv.The Mount Snow Secured Note. The $51.1 million Mount Snow Secured Note provides for interest payments through its maturity on December 1, 2034. As of January 31, 2024, interest on this note accrued at a rate of 12.32 %.

v.The Hunter Mountain Secured Note. The $21.0 million Hunter Mountain Secured Note provides for interest payments through its maturity on January 5, 2036. As of January 31, 2024, interest on this note accrued at a rate of 9.03 %.

In addition, Peak Resorts is required to maintain a debt service reserve account which amounts are applied to fund interest payments and other amounts due and payable to EPR.

(e)Current maturities represent principal payments due in the next 12 months.

Aggregate maturities of debt outstanding as of January 31, 2024 reflected by fiscal year (August 1 through July 31) are as follows (in thousands):

| Total | |||||

| 2024 (February 2024 through July 2024) | $ | ||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028 | |||||

| Thereafter | |||||

Total debt | $ | ||||

The Company recorded interest expense of $40.6 million and $38.4 million for the three months ended January 31, 2024 and 2023, respectively, of which $1.7 million and $1.6 million, respectively, was amortization of deferred financing costs. The Company recorded interest expense of $81.3 million and $73.7 million for the six months ended January 31, 2024 and 2023, respectively, of which $3.2

In connection with the acquisition of Whistler Blackcomb, VHI funded a portion of the purchase price through an intercompany loan to Whistler Blackcomb, which was effective as of November 1, 2016, and requires foreign currency remeasurement to Canadian dollars, the functional currency for Whistler Blackcomb. As a result, foreign currency fluctuations associated with the loan are recorded within the Company’s results of operations. The Company recognized approximately $3.0 million and $(1.9 ) million of non-cash foreign currency gains (losses) on the intercompany loan to Whistler Blackcomb for the three and six months ended January 31, 2024, respectively, on the Company’s Consolidated Condensed Statements of Operations. The Company recognized approximately $2.3 million and $(3.8 ) million of non-cash foreign currency gains (losses) on the intercompany loan to Whistler Blackcomb for the three and six months ended January 31, 2023, respectively, on the Company’s Consolidated Condensed Statements of Operations.

14

6. Acquisitions

Andermatt-Sedrun

On August 3, 2022, through a wholly-owned subsidiary, the Company acquired a 55 % controlling interest in Andermatt-Sedrun Sport AG (“Andermatt-Sedrun”) from Andermatt Swiss Alps AG (“ASA”). The consideration paid consisted of an investment of $114.4 million (CHF 110.0 million) into Andermatt-Sedrun for use in capital investments to enhance the guest experience on mountain (which was prepaid to fund the acquisition and was recorded in other current assets on the Company’s Consolidated Condensed Balance Sheet as of July 31, 2022) and $41.3 million (CHF 39.3 million) paid to ASA (which was paid on August 3, 2022, commensurate with closing). As of August 3, 2022 the total fair value of the consideration paid was $155.4 million (CHF 149.3 million).

Andermatt-Sedrun operates mountain and ski-related assets, including lifts, most of the restaurants and a ski school operation at the ski area. Ski operations are conducted on land owned by ASA as freehold or leasehold properties, land owned by Usern Corporation, land owned by the municipality of Tujetsch and land owned by private property owners. ASA retained a 40% ownership stake, with a group of existing shareholders comprising the remaining 5% ownership stake. ASA and the other noncontrolling economic interests contain certain protective rights pursuant to a shareholder agreement (the “Andermatt Agreement”) and no ability to participate in the day-to-day operations of Andermatt-Sedrun. The Andermatt Agreement provides that no dividend distributions be made by Andermatt-Sedrun until the end of the fiscal year ending July 31, 2026, after which time there shall be annual distributions of 50% of the available cash (as defined in the Andermatt Agreement) for the most recently completed fiscal year. In addition, the distribution rights are non-transferable and transfer of the noncontrolling interests are limited.

The following summarizes the purchase consideration and the purchase price allocation to estimated fair values of the identifiable assets acquired and liabilities assumed at the date the transaction was effective (in thousands):

| Acquisition Date Estimated Fair Value | |||||

| Total cash consideration paid by Vail Resorts, Inc. | $ | ||||

| Estimated fair value of noncontrolling interests | |||||

| Total estimated purchase consideration | $ | ||||

| Allocation of total estimated purchase consideration: | |||||

| Current assets | $ | ||||

| Property, plant and equipment | |||||

| Goodwill | |||||

| Identifiable intangible assets and other assets | |||||

| Assumed long-term debt | ( | ||||

| Other liabilities | ( | ||||

| Net assets acquired | $ | ||||

Identifiable intangible assets acquired in the transaction were primarily related to a trade name. The process of estimating the fair value of the property, plant, and equipment includes the use of certain estimates and assumptions related to replacement cost and physical condition at the time of acquisition. The excess of the purchase price over the aggregate estimated fair values of the assets acquired and liabilities assumed was recorded as goodwill. The goodwill recognized is attributable primarily to expected synergies, the assembled workforce of the resort and other factors, and is not expected to be deductible for income tax purposes. The operating results of Andermatt-Sedrun are reported within the Mountain segment prospectively from the date of acquisition.

15

7. Supplementary Balance Sheet Information

The composition of property, plant and equipment follows (in thousands):

| January 31, 2024 | July 31, 2023 | January 31, 2023 | ||||||||||||||||||

| Land and land improvements | $ | $ | $ | |||||||||||||||||

| Buildings and building improvements | ||||||||||||||||||||

| Machinery and equipment | ||||||||||||||||||||

| Furniture and fixtures | ||||||||||||||||||||

| Software | ||||||||||||||||||||

| Vehicles | ||||||||||||||||||||

| Construction in progress | ||||||||||||||||||||

| Gross property, plant and equipment | ||||||||||||||||||||

| Accumulated depreciation | ( | ( | ( | |||||||||||||||||

| Property, plant and equipment, net | $ | $ | $ | |||||||||||||||||

The composition of accounts payable and accrued liabilities follows (in thousands):

| January 31, 2024 | July 31, 2023 | January 31, 2023 | ||||||||||||||||||

| Trade payables | $ | $ | $ | |||||||||||||||||

| Deferred revenue | ||||||||||||||||||||

| Accrued salaries, wages and deferred compensation | ||||||||||||||||||||

| Accrued benefits | ||||||||||||||||||||

| Deposits | ||||||||||||||||||||

| Operating lease liabilities | ||||||||||||||||||||

| Other liabilities | ||||||||||||||||||||

| Total accounts payable and accrued liabilities | $ | $ | $ | |||||||||||||||||

The changes in the net carrying amount of goodwill by segment for the six months ended January 31, 2024 are as follows (in thousands):

| Mountain | Lodging | Goodwill, net | |||||||||||||||

| Balance at July 31, 2023 | $ | $ | $ | ||||||||||||||

| Effects of changes in foreign currency exchange rates | ( | ( | |||||||||||||||

| Balance at January 31, 2024 | $ | $ | $ | ||||||||||||||

8. Fair Value Measurements

The Company utilizes FASB-issued fair value guidance that establishes how reporting entities should measure fair value for measurement and disclosure purposes. The guidance establishes a common definition of fair value applicable to all assets and liabilities measured at fair value and prioritizes the inputs into valuation techniques used to measure fair value. Accordingly, the Company uses valuation techniques which maximize the use of observable inputs and minimize the use of unobservable inputs when determining fair value. The three levels of the hierarchy are as follows:

Level 1: Inputs that reflect unadjusted quoted prices in active markets that are accessible to the Company for identical assets or liabilities;

Level 2: Inputs include quoted prices for similar assets and liabilities in active and inactive markets or that are observable for the asset or liability either directly or indirectly; and

Level 3: Unobservable inputs which are supported by little or no market activity.

16

The table below summarizes the Company’s cash equivalents, restricted cash, other current assets, interest rate swaps and Contingent Consideration (defined below) measured at estimated fair value (all other assets and liabilities measured at fair value are immaterial) (in thousands).

| Estimated Fair Value Measurement as of January 31, 2024 | ||||||||||||||||||||||||||

| Description | Total | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||

| Money Market | $ | $ | $ | — | $ | — | ||||||||||||||||||||

| Commercial Paper | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Certificates of Deposit | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Interest Rate Swaps | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||

| Contingent Consideration | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| Estimated Fair Value Measurement as of July 31, 2023 | ||||||||||||||||||||||||||

| Description | Total | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||

| Money Market | $ | $ | $ | — | $ | — | ||||||||||||||||||||

| Commercial Paper | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Certificates of Deposit | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Interest Rate Swaps | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||

| Contingent Consideration | $ | $ | — | $ | — | $ | ||||||||||||||||||||

| Estimated Fair Value Measurement as of January 31, 2023 | ||||||||||||||||||||||||||

| Description | Total | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||

| Money Market | $ | $ | $ | — | $ | — | ||||||||||||||||||||

| Commercial Paper | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Certificates of Deposit | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Interest Rate Swaps | $ | $ | — | $ | $ | — | ||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||

| Contingent Consideration | $ | $ | — | $ | — | $ | ||||||||||||||||||||

The Company’s cash equivalents, restricted cash, other current assets and interest rate swaps are measured utilizing quoted market prices or pricing models whereby all significant inputs are either observable or corroborated by observable market data. The estimated fair value of the interest rate swaps are included within other current assets on the Company’s Consolidated Condensed Balance Sheet as of January 31, 2024 and included within other assets as of July 31, 2023 and January 31, 2023.

The changes in Contingent Consideration during the six months ended January 31, 2024 and 2023 were as follows (in thousands):

| Balance as of July 31, 2023 and 2022, respectively | $ | $ | ||||||||||||

| Payments | ( | ( | ||||||||||||

| Change in estimated fair value | ||||||||||||||

| Balance as of January 31, 2024 and 2023, respectively | $ | $ | ||||||||||||

17

During the six months ended January 31, 2024, the Company made a payment to the landlord for Contingent Consideration of approximately $17.1 million and recorded an increase of approximately $6.5 million, primarily related to the estimated Contingent Consideration payment for the fiscal year ending July 31, 2024. These changes resulted in an estimated fair value of the Contingent Consideration of approximately $62.7 million, which is reflected in other long-term liabilities in the Company’s Consolidated Condensed Balance Sheet.

9. Commitments and Contingencies

Guarantees/Indemnifications

As of January 31, 2024, the Company had various letters of credit outstanding totaling $95.0 million, consisting of $53.4 million to support the Employee Housing Bonds; $6.4 million to support bonds issued by Holland Creek Metropolitan District; and $35.2 million primarily for workers’ compensation, a wind energy purchase agreement and insurance-related deductibles. The Company also had surety bonds of $9.5 million as of January 31, 2024, primarily to provide collateral for its U.S. workers compensation self-insurance programs.

In addition to the guarantees noted above, the Company has entered into contracts in the normal course of business that include certain indemnifications under which it could be required to make payments to third parties upon the occurrence or non-occurrence of certain future events. These indemnities include indemnities related to licensees in connection with third-parties’ use of the Company’s trademarks and logos, liabilities associated with the infringement of other parties’ technology and software products, liabilities associated with the use of easements, liabilities associated with employment of contract workers and the Company’s use of trustees and liabilities associated with the Company’s use of public lands and environmental matters. The duration of these indemnities generally is indefinite and generally do not limit the future payments the Company could be obligated to make.

As permitted under applicable law, the Company and certain of its subsidiaries have agreed to indemnify their directors and officers over their lifetimes for certain events or occurrences while the officer or director is, or was, serving the Company or its subsidiaries in such a capacity. The maximum potential amount of future payments the Company could be required to make under these indemnification agreements is unlimited; however, the Company has a director and officer insurance policy that should enable the Company to recover a portion of any amounts paid.

Unless otherwise noted, the Company has not recorded any significant liabilities for the letters of credit, indemnities and other guarantees noted above in the accompanying Consolidated Condensed Financial Statements, either because the Company has recorded on its Consolidated Condensed Balance Sheets the underlying liability associated with the guarantee, the guarantee is with respect to the Company’s own performance and is therefore not subject to the measurement requirements as prescribed by GAAP, or because the Company has calculated the estimated fair value of the indemnification or guarantee to be immaterial based on the current facts and circumstances that would trigger a payment under the indemnification clause. In addition, with respect to certain indemnifications, it is not possible to determine the maximum potential amount of liability under these potential obligations due to the unique set of facts and circumstances likely to be involved in each particular claim and indemnification provision. Historically, payments made by the Company under these obligations have not been material.

As noted above, the Company makes certain indemnifications to licensees for their use of the Company’s trademarks and logos. The Company does not record any liabilities with respect to these indemnifications.

Additionally, the Company has entered into strategic long-term season pass alliance agreements with third-party mountain resorts in which the Company has committed to pay minimum revenue guarantees over the remaining terms of these agreements.

Self-Insurance

The Company is self-insured for claims under its U.S. health benefit plans and for the majority of workers’ compensation claims in the U.S. Workers compensation claims in the U.S. are subject to stop loss policies. The self-insurance liability related to workers’ compensation is determined actuarially based on claims filed. The self-insurance liability related to claims under

18

the Company’s U.S. health benefit plans is determined based on analysis of actual claims. The amounts related to these claims are included as a component of accrued benefits in accounts payable and accrued liabilities (see Note 7, Supplementary Balance Sheet Information).

Legal

The Company is a party to various lawsuits arising in the ordinary course of business. Management believes the Company has adequate insurance coverage and/or has accrued for all loss contingencies for asserted and unasserted matters deemed to be probable and estimable losses. As of January 31, 2024, July 31, 2023 and January 31, 2023, the accruals for the above loss contingencies were not material individually or in the aggregate.

10. Segment Information

The Company has three reportable segments: Mountain, Lodging and Real Estate. The Company refers to “Resort” as the combination of the Mountain and Lodging segments. The Mountain segment includes the operations of the Company’s mountain resorts/ski areas and related ancillary activities. The Lodging segment includes the operations of the Company’s owned hotels, RockResorts, NPS concessioner properties, condominium management, Colorado resort ground transportation operations and mountain resort golf operations. The Real Estate segment owns, develops and sells real estate in and around the Company’s resort communities. The Company’s reportable segments, although integral to the success of the others, offer distinctly different products and services and require different types of management focus. As such, these segments are managed separately.

The Company reports its segment results using Reported EBITDA (defined as segment net revenue less segment operating expenses, plus segment equity investment income or loss, and for the Real Estate segment, plus gain or loss on sale of real property). The Company reports segment results in a manner consistent with management’s internal reporting of operating results to the chief operating decision maker (Chief Executive Officer) for purposes of evaluating segment performance.

Items excluded from Reported EBITDA are significant components in understanding and assessing financial performance. Reported EBITDA should not be considered in isolation or as an alternative to, or substitute for, net income, net change in cash and cash equivalents or other financial statement data presented in the accompanying Consolidated Condensed Financial Statements as indicators of financial performance or liquidity.

The Company utilizes Reported EBITDA in evaluating the performance of the Company and in allocating resources to its segments. Mountain Reported EBITDA consists of Mountain net revenue less Mountain operating expense plus Mountain equity investment income or loss. Lodging Reported EBITDA consists of Lodging net revenue less Lodging operating expense. Real Estate Reported EBITDA consists of Real Estate net revenue less Real Estate operating expense plus gain or loss on sale of real property. All segment expenses include an allocation of corporate administrative expense. Assets are not used to evaluate performance, except as shown in the table below. The accounting policies specific to each segment are the same as those described in Note 2, Summary of Significant Accounting Policies.

19

The following table presents financial information by reportable segment, which is used by management in evaluating performance and allocating resources (in thousands):

| Three Months Ended January 31, | Six Months Ended January 31, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net revenue: | |||||||||||||||||||||||

| Mountain | $ | $ | $ | $ | |||||||||||||||||||

| Lodging | |||||||||||||||||||||||

| Total Resort net revenue | |||||||||||||||||||||||

| Real Estate | |||||||||||||||||||||||

| Total net revenue | $ | $ | $ | $ | |||||||||||||||||||

| Segment operating expense: | |||||||||||||||||||||||

| Mountain | $ | $ | $ | $ | |||||||||||||||||||

| Lodging | |||||||||||||||||||||||

| Total Resort operating expense | |||||||||||||||||||||||

| Real Estate | |||||||||||||||||||||||

| Total segment operating expense | $ | $ | $ | $ | |||||||||||||||||||

| Gain on sale of real property | $ | $ | $ | $ | |||||||||||||||||||

| Mountain equity investment (loss) income, net | $ | ( | $ | $ | $ | ||||||||||||||||||

| Reported EBITDA: | |||||||||||||||||||||||

| Mountain | $ | $ | $ | $ | |||||||||||||||||||

| Lodging | ( | ( | |||||||||||||||||||||

| Resort | |||||||||||||||||||||||

| Real Estate | ( | ||||||||||||||||||||||

| Total Reported EBITDA | $ | $ | $ | $ | |||||||||||||||||||

| Real estate held for sale or investment | $ | $ | $ | $ | |||||||||||||||||||

| Reconciliation from net income attributable to Vail Resorts, Inc. to Total Reported EBITDA: | |||||||||||||||||||||||

| Net income attributable to Vail Resorts, Inc. | $ | $ | $ | $ | |||||||||||||||||||

| Net income attributable to noncontrolling interests | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Provision for income taxes | |||||||||||||||||||||||

| Income before provision for income taxes | |||||||||||||||||||||||

| Depreciation and amortization | |||||||||||||||||||||||

| Change in estimated fair value of contingent consideration | |||||||||||||||||||||||

| Loss on disposal of fixed assets and other, net | |||||||||||||||||||||||

| Investment income and other, net | ( | ( | ( | ( | |||||||||||||||||||

| Foreign currency (gain) loss on intercompany loans | ( | ( | |||||||||||||||||||||

| Interest expense, net | |||||||||||||||||||||||

| Total Reported EBITDA | $ | $ | $ | $ | |||||||||||||||||||

20

11. Share Repurchase Program

On March 9, 2006, the Company’s Board of Directors approved a share repurchase program, authorizing the Company to repurchase up to 3,000,000 Vail Shares. On July 16, 2008, December 4, 2015 and March 7, 2023, the Company’s Board of Directors increased the authorization by an additional 3,000,000 , 1,500,000 and 2,500,000 Vail Shares, respectively, for a total authorization to repurchase up to 10,000,000 Vail Shares. The Company did not repurchase any Vail Shares during the three months ended January 31, 2024. The Company repurchased 237,056 Vail Shares during the six months ended January 31, 2024 (at a total cost of approximately $50.0 million, excluding accrued excise tax). The Company did not repurchase any Vail Shares during the three and six months ended January 31, 2023. Since inception of its share repurchase program through January 31, 2024, the Company has repurchased 8,885,358 Vail Shares for approximately $1,029.5 million. As of January 31, 2024, 1,114,642 Vail Shares remained available to repurchase under the existing share repurchase program, which has no expiration date. Vail Shares purchased pursuant to the repurchase program will be held as treasury shares and may be used for the issuance of Vail Shares under the Company’s employee share award plan.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Vail Resorts, Inc., together with its subsidiaries, is referred to throughout this Quarterly Report on Form 10-Q for the period ended January 31, 2024 (“Form 10-Q”) as “we,” “us,” “our” or the “Company.”

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with our Annual Report on Form 10-K for the fiscal year ended July 31, 2023 (“Form 10-K”) and the Consolidated Condensed Financial Statements as of January 31, 2024 and 2023 and for the three and six months then ended, included in Part I, Item 1 of this Form 10-Q, which provide additional information regarding our financial position, results of operations and cash flows. To the extent that the following MD&A contains statements which are not of a historical nature, such statements are forward-looking statements, which involve risks and uncertainties. See “Forward-Looking Statements” below. These risks include, but are not limited to, those discussed in our filings with the Securities and Exchange Commission (“SEC”), including the risks described in Item 1A. “Risk Factors” of Part I of our Form 10-K, which was filed on September 28, 2023.

The MD&A includes discussion of financial performance within each of our three segments. We have chosen to specifically include segment Reported EBITDA (defined as segment net revenue less segment operating expense, plus segment equity investment income or loss, and for the Real Estate segment, plus gain or loss on sale of real property) in the following discussion because we consider this measurement to be a significant indication of our financial performance. We utilize segment Reported EBITDA in evaluating our performance and in allocating resources to our segments. Net Debt (defined as long-term debt, net plus long-term debt due within one year less cash and cash equivalents) is included in the following discussion because we consider this measurement to be a significant indication of our available capital resources. We also believe that Net Debt is an important measurement as it is an indicator of our ability to obtain additional capital resources for our future cash needs. Resort Reported EBITDA (defined as the combination of segment Reported EBITDA of our Mountain and Lodging segments), Total Reported EBITDA (which is Resort Reported EBITDA plus segment Reported EBITDA from our Real Estate segment) and Net Debt are not measures of financial performance or liquidity defined under accounting principles generally accepted in the United States (“GAAP”). Refer to the end of the Results of Operations section for a reconciliation of net income attributable to Vail Resorts, Inc. to Total Reported EBITDA and Resort Reported EBITDA, and long-term debt, net to Net Debt.

Items excluded from Resort Reported EBITDA, Total Reported EBITDA and Net Debt are significant components in understanding and assessing financial performance or liquidity. Resort Reported EBITDA, Total Reported EBITDA and Net Debt should not be considered in isolation or as an alternative to, or substitute for, net income, net change in cash and cash equivalents or other financial statement data presented in the Consolidated Condensed Financial Statements as indicators of financial performance or liquidity. Because Resort Reported EBITDA, Total Reported EBITDA and Net Debt are not measurements determined in accordance with GAAP and are thus susceptible to varying calculations, Resort Reported EBITDA, Total Reported EBITDA and Net Debt, as presented herein, may not be comparable to other similarly titled measures of other companies. In addition, our segment Reported EBITDA (i.e., Mountain, Lodging and Real Estate), the measure of segment profit or loss required to be disclosed in accordance with GAAP, may not be comparable to other similarly titled measures of other companies.

Overview

Our operations are grouped into three integrated and interdependent segments: Mountain, Lodging and Real Estate. We refer to “Resort” as the combination of the Mountain and Lodging segments.

21

Mountain Segment

In the Mountain segment, the Company operates the following 41 destination mountain resorts and regional ski areas (collectively, “Resorts”):

*Denotes a destination mountain resort, which generally receives a meaningful portion of skier visits from long-distance travelers, as opposed to our regional ski areas, which tend to generate skier visits predominantly from their respective local markets.

Additionally, the Mountain segment includes ancillary services, primarily including ski school, dining and retail/rental operations, and for our Australian ski areas, including lodging and transportation operations. Mountain segment revenue is seasonal, with the majority of revenue earned from our North American and European ski operations occurring in our second and third fiscal quarters and the majority of revenue earned from our Australian ski operations occurring in our first and fourth fiscal quarters. Our North American and European Resorts typically experience their peak operating season for the Mountain segment from mid-December through mid-April, and our Australian ski areas typically experience their peak operating season from June to early October. Consequently, our first and fourth fiscal quarters are seasonally low periods as most of our North American and European ski operations are generally not open for business, and the activity of our Australian ski areas’ peak season and our North American and European summer operating results are not sufficient to offset the losses incurred during these seasonally low periods. Revenue of the Mountain segment during the first and fourth fiscal quarters is primarily generated from summer and group related visitation at our North American and European destination mountain resorts, retail/rental operations and peak season Australian ski operations. Our largest source of Mountain segment revenue is the sale of lift tickets (including pass products), which represented approximately 60% and 58% of Mountain segment net revenue for the three months ended January 31, 2024 and 2023, respectively.

Lift revenue is driven by volume and pricing. Pricing is impacted by absolute pricing, as well as both the demographic and geographic mix of guests, which impacts the price points at which various products are purchased. The demographic mix of guests that visit our North American Resorts is divided into two primary categories: (i) out-of-state and international (“Destination”) guests and (ii) in-state and local (“Local”) guests. The geographic mix depends on levels of visitation to our destination mountain resorts versus our regional ski areas. For the three months ended January 31, 2024, Destination guests comprised approximately 55% of our North American destination mountain resort skier visits (excluding complimentary access), while Local guests comprised approximately 45% of our North American destination mountain resort skier visits (excluding complimentary access), which compares to 54% and 46%, respectively, for the three months ended January 31, 2023. Skier visitation at our regional ski areas is largely comprised of Local guests. Destination guests generally purchase our higher-priced lift tickets (including pass products) and utilize more ancillary services such as ski school, dining and retail/rental, as well as lodging at or around our mountain resorts. Additionally, Destination guest visitation is less likely to be impacted by changes in the weather during the current season, but may be more impacted by adverse economic conditions, the global geopolitical climate, travel disruptions or weather conditions in the immediately preceding ski season. Local guests tend to be more value-oriented and weather-sensitive.

22

We offer a variety of pass products for all of our Resorts, marketed toward both Destination and Local guests. Our pass product offerings range from providing access to one or a combination of our Resorts for a certain number of days to our Epic Pass, which allows pass holders unlimited and unrestricted access to all of our Resorts. The Epic Day Pass is a customizable one to seven day pass product purchased in advance of the season, for those skiers and riders who expect to ski a certain number of days during the season, and which is available in three tiers of resort access offerings. Our pass products provide a compelling value proposition to our guests, which in turn assists us in developing a loyal base of customers who commit to ski at our Resorts generally in advance of the ski season and typically ski more days each season at our Resorts than those guests who do not buy pass products. Additionally, we enter into strategic long-term pass alliance agreements with third-party mountain resorts, which further increase the value proposition of our pass products. For the 2024/2025 ski season, our pass alliances include Telluride Ski Resort in Colorado, Hakuba Valley and Rusutsu Resort in Japan, Resorts of the Canadian Rockies in Canada, Les 3 Vallées in France, Disentis Ski Area and Verbier 4 Vallées in Switzerland, Skirama Dolomiti in Italy and Ski Arlberg in Austria. Our pass program drives strong customer loyalty; mitigates exposure to more weather sensitive guests; generates additional ancillary spending; and provides cash flow in advance of winter season operations. In addition, our pass program attracts new guests to our Resorts. All of our pass products, including the Epic Pass and Epic Day Pass, are predominately sold prior to the start of the ski season. Pass product revenue, although primarily collected prior to the ski season, is recognized in the Consolidated Condensed Statements of Operations throughout the ski season on a straight-line basis using the number of skiable days of the season-to-date period relative to the total estimated number of skiable days of the season.

Lift revenue consists of pass product lift revenue (“pass revenue”) and non-pass product lift revenue (“non-pass revenue”). For the three months ended January 31, 2024 and 2023, approximately 74% and 70%, respectively, of our total lift revenue recognized was derived from pass revenue. Pass revenue recognized year to date, which is primarily recognized in our second fiscal quarter, represents approximately 50% and 51%, of our total North American pass product revenue for the 2023/2024 and 2022/2023 North American ski seasons, respectively, with the remaining North American pass revenue almost entirely recognized as lift revenue in our third fiscal quarter ending April 30. The decrease in the portion of pass product revenue recognized year to date compared to the prior year to date period is primarily the result of unfavorable early season conditions in the current year, which were impacted by limited natural snow and variable temperatures that resulted in delayed openings, compared with strong conditions in the prior year. This variability in Resort opening dates resulted in an approximately $14 million reduction of recognized pass revenue for the three months ended January 31, 2024 compared to what we would have recognized had our Resorts been able to open on the same schedule as they did in the prior year. This is a timing difference that will largely reverse during our third fiscal quarter.

The cost structure of our mountain resort operations has a significant fixed component with variable expenses including, but not limited to, land use permit or lease fees, credit card fees, retail/rental cost of sales and labor, ski school labor and dining operations; as such, profit margins can fluctuate greatly based on the level of revenues.

Lodging Segment

Operations within the Lodging segment include: (i) ownership/management of a group of luxury hotels through the RockResorts brand proximate to our Colorado and Utah mountain resorts; (ii) ownership/management of non-RockResorts branded hotels and condominiums proximate to our North American Resorts; (iii) National Park Service (“NPS”) concessioner properties, including the Grand Teton Lodge Company (“GTLC”); (iv) a Colorado resort ground transportation company; and (v) mountain resort golf courses.

The performance of our lodging properties (including managed condominium rooms) proximate to our Resorts, and our Colorado resort ground transportation company, are closely aligned with the performance of the Mountain segment and generally experience similar seasonal trends, particularly with respect to visitation by Destination guests. Revenues from such properties represented approximately 94% of Lodging segment net revenue (excluding Lodging segment revenue associated with the reimbursement of payroll costs) for both the three months ended January 31, 2024 and 2023. Management primarily focuses on Lodging net revenue excluding payroll cost reimbursements and Lodging operating expense excluding reimbursed payroll costs (which are not measures of financial performance under GAAP) as the reimbursements are made based upon the costs incurred with no added margin and as such, the revenue and corresponding expense do not affect our Lodging Reported EBITDA, which we use to evaluate Lodging segment performance. Revenue of the Lodging segment during our first and fourth fiscal quarters is generated primarily by the operations of our NPS concessioner properties (as their peak operating season generally occurs during the months of June to October), as well as golf operations and seasonally low operations from our other owned and managed properties and businesses.

23

Real Estate Segment

The principal activities of our Real Estate segment include the sale of land parcels to third-party developers and planning for future real estate development projects, including zoning and acquisition of applicable permits. We continue undertaking preliminary planning and design work on future projects and are pursuing opportunities with third-party developers rather than undertaking our own significant vertical development projects. Additionally, real estate development projects by third-party developers most often result in the creation of certain resort assets that provide additional benefit to the Mountain segment. We believe that, due to our low carrying cost of real estate land investments, we are well situated to promote future projects by third-party developers while limiting our financial risk. Our revenue from the Real Estate segment and associated expense can fluctuate significantly based upon the timing of closings and the type of real estate being sold, causing volatility in the Real Estate segment’s operating results from period to period.

Recent Trends, Risks and Uncertainties

Together with those risk factors we have identified in our Form 10-K, we have identified the following important factors (as well as risks and uncertainties associated with such factors) that could impact our future financial performance or condition:

•Our results for the three months ended January 31, 2024 were negatively impacted by challenging conditions at all of our North American resorts, with approximately 42% lower snowfall across our western North American resorts through January compared to the same period in the prior year and limited natural snow and variable temperatures at our Eastern U.S. resorts (comprising the Midwest, Mid-Atlantic, and Northeast). Despite the impacts of conditions, Resort Reported EBITDA increased approximately 8% for the three months ended January 31, 2024 as compared to the prior year period, primarily driven by the stability created by our season pass results. While visitation declined, our ancillary businesses performed well, in particular our ski and ride school, dining and rental businesses experienced strong growth in spending per visit compared to the prior year.

•The timing and amount of snowfall can have an impact on Mountain and Lodging revenue, particularly with regard to skier visits and the duration and frequency of guest visitation. To help mitigate this impact, we sell a variety of pass products prior to the beginning of the ski season, which results in a more stabilized stream of lift revenue. Additionally, our pass products provide a compelling value proposition to our guests, which in turn create a guest commitment predominately prior to the start of the ski season. Pass revenue increased approximately $34.3 million, or 8.3%, for the three months ended January 31, 2024 compared to the same period in the prior year, primarily due to increased pass product sales for the 2023/2024 North American ski season compared to the 2022/2023 North American ski season, partially offset by the impact of delayed Resort opening dates in the current year (as discussed above). Deferred revenue related to North American pass product sales was approximately $457.0 million as of January 31, 2024 (compared to approximately $398.0 million as of January 31, 2023).