UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________

FORM 20-F

_____________________

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Date of event requiring this shell company report

Commission file number 001-40692

_____________________

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

State of Israel

(Jurisdiction of incorporation or organization)

Riskified Ltd.

(Address of principal executive offices)

Chief Executive Officer

Riskified Ltd.

Email: [email protected]

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

_____________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act.: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of December 31, 2023, the registrant had 128,738,857 Class A ordinary shares, no par value, and 49,814,864 Class B ordinary shares, no par value, outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, "accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |||||||||

| Non-accelerated filer | ☐ | Emerging growth company | ☒ | ||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ | Other | ☐ | |||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

TABLE OF CONTENTS

| Page | |||||

ABOUT THIS ANNUAL REPORT

Except where the context requires or where otherwise indicated in this Annual Report on Form 20-F for the fiscal year ended December 31, 2023 (this “Annual Report”), the terms “Riskified,” the “Company,” “we,” “us,” “our,” “our company,” and “our business” refers to Riskified Ltd. and its consolidated subsidiaries as a consolidated entity.

All references in this Annual Report to “Israeli currency” and “NIS” refer to New Israeli Shekels, the terms “dollar,” “USD” or “$” refer to U.S. dollars and the terms “€” or “euro” refer to the currency introduced at the start of the third stage of the European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

BASIS OF PRESENTATION

Presentation of Financial Information

Our consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States, or U.S. GAAP (“GAAP”). We present our consolidated financial statements in U.S. dollars.

Our fiscal year ends on December 31 of each year. Our most recent fiscal year ended on December 31, 2023.

Certain monetary amounts, percentages and other figures included elsewhere in this Annual Report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables or charts may not be the arithmetic aggregation of the figures that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them. Certain amounts in prior periods have been reclassified to conform to the current period presentation.

Certain Definitions

As used in this Annual Report, except where the context otherwise requires or where otherwise indicated:

•“Approval rate” is defined as GMV that has been approved divided by GMV that has been reviewed.

•“Billings” or “amounts billed” is defined as (1) gross amounts invoiced to our merchants and estimates for cancellations and service level agreements for transactions approved during the period plus (2) changes in estimates for cancellations and service level agreements for orders approved in prior periods. Billings excludes credits issued for chargebacks.

•“Chargebacks” refers to forced transaction reversals typically associated with credit and debit card transactions. Chargebacks occur when a cardholder disputes a transaction with its bank and the cardholder’s bank rules in favor of the cardholder. In such instances, funds associated with the payment are withdrawn from the merchant’s bank account resulting in a loss equal to the amount of the item that was received by the consumer. Chargebacks are meant as a consumer protection mechanism from fraudulent transactions, however, they may also incite abuse and friendly fraud. For example, friendly fraud may occur when a consumer, rather than returning an order they are dissatisfied with, instead initiates the chargeback process to avoid the complicated returns process. Friendly fraud may violate the merchant’s cancellation policies and, depending on the jurisdiction, may also be unlawful.

•“Consumers” refers to end-consumers who purchase goods or services from our merchants.

•“Merchants” refers to the businesses that purchase our products.

1

Key Performance Indicators

Throughout this Annual Report, we provide a number of key performance indicators used by our management and often by competitors in our industry. These are discussed in more detail in the section entitled “Operating and Financial Review and Prospects—Key Performance Indicators and Non-GAAP Financial Measures” which also includes non-GAAP financial measures and a reconciliation of our non-GAAP financial measures to the most directly comparable GAAP measure. We define these key performance indicators as follows:

•“Chargebacks-to-billings ratio” or “CTB Ratio” is defined as the total amount of chargeback expenses incurred during the period indicated divided by the total amount of Billings to all of our merchants over the same period.

•“Gross Merchandise Volume” or “GMV” is defined as the gross total dollar value of orders reviewed through our ecommerce risk intelligence platform during the period indicated, including the value of orders that we did not approve.

•“Net Dollar Retention Rate” is defined as amounts billed in the current period to the same cohort of accounts that were active in the prior comparative period. The amounts billed include any upsell and are net of contraction and attrition. We define an active account as an account that generally has (a) submitted at least one order to us for review in every month of the prior comparative period and (b) has not churned during the prior comparative period.

Along with the GAAP metrics and non-GAAP financial measures described in Item 5. “Operating and Financial Review and Prospects”, the aforementioned key performance indicators are used by management and our board of directors to assess our performance, for financial and operational decision-making, and as a means to evaluate period-to-period comparisons. These measures are frequently used by analysts, investors and other interested parties to evaluate companies in our industry. These key performance indicators may not necessarily be comparable to similarly titled captions of other companies due to different methods of calculation.

Reverse Share Split

On July 28, 2021, we effectuated a two-for-one reverse share split of our Class A ordinary shares (the “Reverse Share Split”). No fractional shares were issued in connection with the Reverse Share Split. The historical financial statements included elsewhere in this Annual Report have been adjusted retroactively for the Reverse Share Split. Unless otherwise indicated, all other share and per share data in this Annual Report has been retroactively adjusted, where applicable, to reflect the Reverse Share Split as if it had occurred at the beginning of the earliest period presented.

Additional Class B Issuance

Immediately after the effectiveness of the Reverse Share Split, we issued and distributed Class B ordinary shares to holders of the Class A ordinary shares on a two-for-one ratio, such that each holder of Class A ordinary shares received two Class B ordinary shares for each Class A ordinary share held (the “Additional Class B Issuance”). The historical financial statements presented prior to the Reverse Share Split included elsewhere in this Annual Report have not been retroactively adjusted for the Additional Class B Issuance.

Market and Industry Data

Unless otherwise indicated, information in this Annual Report concerning economic conditions, our industry, our markets and our competitive position is based on a variety of sources, including information from independent industry analysts and publications, as well as our own estimates and research.

Our estimates are derived from publicly available information released by independent third-party sources, as well as data from our internal research, and are based on assumptions made by us upon

2

reviewing such data and our knowledge of our industry, which we believe to be reasonable. Certain statistical data, estimates and forecasts contained elsewhere in this Annual Report have been derived from:

•an independent industry report published by eMarketer, titled “Global Retail eCommerce Forecast 2024” (January 2024); and

•an independent industry data set published by eCommerceDB.com as of December 31, 2022.

None of the independent industry publications or data sets relied upon by us or otherwise referred to in this Annual Report were prepared on our behalf. Although we believe the data from these third-party sources is reliable, we have not independently verified any such information, and these sources generally state that the information they contain has been obtained from sources believed to be reliable but that the accuracy and completeness of such information is not guaranteed.

Projections, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Cautionary Note Regarding Forward-Looking Statements” and Item 3.D. “Risk Factors.” These and other factors could cause results to differ materially from those expressed in the estimates made by independent third parties and by us.

Certain estimates of market opportunity and forecasts of market growth included in this Annual Report may prove to be inaccurate. The market for our products is relatively new and will experience changes over time. The estimates and forecasts in this Annual Report relating to the size of our target market, market demand and adoption, capacity to address this demand and pricing may prove to be inaccurate. The addressable market we estimate may not materialize for many years, if ever, and even if the markets in which we compete meet the size estimates in this Annual Report, our business could fail to grow at similar rates, if at all.

Trademarks

We have proprietary rights to trademarks, service marks and trade names used in this Annual Report that are important to our business, including, among others, Riskified and the Riskified design logo. Solely for convenience, trademarks, service marks and trade names referred to in this Annual Report may appear without the “®” or “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies’ trademarks, trade names or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this Annual Report is the property of its respective holder.

3

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements contained in this Annual Report other than statements of historical fact, including, without limitation, statements regarding our future results of operations and financial position, growth strategy, plans and objectives of management for future operations, including, among others, expansion in new and existing markets, development and introductions of new products, capital expenditures and debt service obligations and the implementation of our share repurchase program, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “potential,” “continue,” “anticipate,” “intend,” “expect,” “could,” “would,” “project,” “predict,” “forecasts,” “aims,” “plan,” “target,” and similar expressions are intended to identify forward-looking statements, though not all forward-looking statements use these words or expressions. These forward-looking statements are principally contained in the sections entitled Item 3.D. “Risk Factors,” Item 4. “Information on the Company,” and Item 5. “Operating and Financial Review and Prospects.” These statements are neither promises nor guarantees, but involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, the following:

•our ability to manage our growth effectively;

•continued use of credit and debit cards and other payment methods that expose merchants to the risk of payment fraud, and changes or proposed changes in laws and regulations, including card scheme rules, or differing interpretations or enforcement of laws or regulations related to use of these payment methods, and the emergence of new alternative payment products;

•our history of net losses and ability to achieve and maintain profitability;

•our ability to attract new merchants and retain existing merchants;

•the impact of macroeconomic conditions on us and on the performance of our merchants;

•our ability to continue to improve our machine learning models;

•fluctuations in our CTB Ratio and gross profit margin;

•our ability to protect the information of our merchants and consumers;

•our ability to predict future revenue due to lengthy sales cycles;

•seasonal fluctuations in revenue;

•competition;

•our merchant concentration;

•the financial condition of our merchants, particularly in challenging macroeconomic environments;

•our ability to increase the adoption of our products and to develop and introduce new products;

•our ability to mitigate the risks involved with selling our products to large enterprises;

•our ability to retain the services of our executive officers, and other key personnel, including our co-founders;

4

•our ability to attract and retain highly qualified personnel, including software engineers and data scientists, particularly in Israel;

•changes to our prices and pricing structures;

•our exposure to potential future litigation claims;

•our exposure to fluctuations in currency exchange rates;

•our ability to obtain additional capital;

•our third-party providers of cloud-based infrastructure;

•our ability to protect our intellectual property rights;

•technology and infrastructure interruptions or performance problems;

•the efficiency and accuracy of our machine learning models and access to third-party and merchant data;

•our ability to comply with evolving data protection, privacy and security laws;

•any actual or perceived failure to comply with evolving regulatory frameworks around the development and use of artificial intelligence;

•our ability to successfully implement and use machine learning technology and artificial intelligence;

•our use of open-source software;

•our ability to enhance and maintain our brand;

•our ability to execute potential acquisitions, strategic investments, partnerships, or alliances;

•potential claims related to the violation of the intellectual property rights of third parties;

•our failure to comply with anti-corruption, trade compliance, and economic sanctions laws and regulations;

•our ability to enforce non-compete agreements entered into with employees in certain locations;

•our ability to maintain effective systems of disclosure controls and financial reporting;

•our ability to accurately estimate or judgements relating to our critical accounting policies;

•our business in China;

•changes in tax laws or regulations;

•increasing scrutiny of, and expectations for, environmental, social and governance initiatives;

•potential future requirements to collect sales or other taxes;

•potential future changes in the taxation of international business and corporate tax reform;

•changes in and application of insurance laws or regulations;

•conditions in Israel that may affect our operations, including the ongoing war between Israel and Hamas, as well as tension between Israel and Hezbollah on the Israel-Lebanon border;

5

•the impact of the dual class structure of our ordinary shares;

•the timing and amount of our share repurchases (if any);

•our status as a foreign private issuer; and

•the other matters described in the section entitled Item 3.D. “Risk Factors.”]

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition and operating results. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in Item 3.D. “Risk Factors” and elsewhere in this Annual Report. Moreover, we operate in an evolving environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any estimates or forward-looking statements. We qualify all of our estimates and forward-looking statements by these cautionary statements.

Additionally, we may provide information herein or on our website, or documents accessible thereby, that is not necessarily “material” under the federal securities laws for Securities and Exchange Commission (“SEC”) reporting purposes, but that is informed by various environmental, social, and governance (“ESG”) standards and frameworks (including standards for the measurement of underlying data), and the interests of various stakeholders, among other things. Much of this information is subject to assumptions, estimates or third-party information that is still evolving and subject to change. For example, our disclosures based on any standards may change due to revisions in framework requirements, availability or quality of information, changes in our business or applicable government policies, or other factors, some of which may be beyond our control.

The estimates and forward-looking statements contained in this Annual Report speak only as of the date of this Annual Report. Except as required by applicable law, we undertake no obligation to publicly update or revise any estimates or forward-looking statements contained in this Annual Report, whether as a result of any new information, future events, or otherwise, or to reflect the occurrence of unanticipated events or otherwise.

6

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

You should carefully consider the risks and uncertainties described below and the other information in this Annual Report before making an investment decision. Our business, financial condition, results of operations or strategic objectives could be materially and adversely affected by any of these risks and uncertainties. The trading price and value of our Class A ordinary shares could decline due to any of these risks and uncertainties, and you may lose all or part of your investment. This Annual Report also contains forward-looking statements that involve risks and uncertainties. See “Cautionary Note Regarding Forward-Looking Statements.” Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks and uncertainties faced by us described below and elsewhere in this Annual Report.

Risks Relating to Our Business and Industry

We have experienced substantial growth since our inception. If we fail to manage our growth effectively, then our revenues, results of operations, and financial condition may be adversely affected.

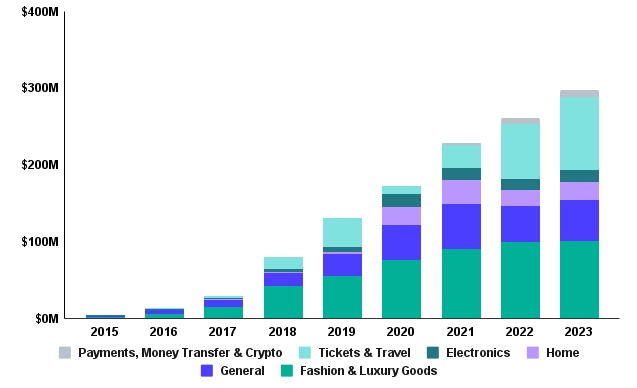

We have experienced substantial growth in our business since inception in 2012. Our revenue was $297.6 million and $261.2 million for the years ended December 31, 2023 and 2022, respectively, representing an increase of 14%. Our historical revenue growth may not be sustainable and should not be considered indicative of our future performance. Since launching our business, we have frequently expanded and enhanced our products, extended our geographic presence, and changed our pricing methodologies. This evolution and associated growth makes it difficult to evaluate our future prospects and the risks and challenges we may encounter. These risks include our ability to:

•accurately forecast our revenue and plan our operating expenses;

•increase the number of new merchants and retain existing merchants using our products;

•successfully compete with current and future competitors;

•successfully expand our business in existing markets, and enter new markets and geographies;

•anticipate and respond to macroeconomic changes and changes in the markets in which we operate;

7

•successfully execute on our growth initiatives while also focusing on enhanced expense discipline and path to profitability;

•accurately adjust our pricing structures for our products;

•maintain and enhance the value of our reputation and brand;

•adapt to rapidly evolving trends in the ways merchants and consumers interact with, and shop using, technology;

•accurately predict projected chargeback expenses, especially in new industry verticals, new geographies and with respect to new payment methods, or if new fraud patterns develop more quickly than our ability to detect and block those new fraud patterns;

•avoid interruptions or disruptions to our service;

•develop a scalable, high-performance technology infrastructure that can efficiently and reliably handle increased usage, as well as the deployment of new features and products; and

•hire, integrate, and retain talented technology, sales, and other personnel.

In addition, any material decline in global ecommerce transaction volumes in the future, for whatever reason, may adversely impact our future revenues and financial condition.

If we fail to address the risks and difficulties we face, including those associated with the challenges listed above as well as those described elsewhere in this “Risk Factors” section, our business, financial condition, and results of operations could be adversely affected.

We are dependent upon the continued use of credit and debit cards and other payment methods that expose our merchants to the risk of payment fraud as a primary means of payment for ecommerce transactions. Changes in laws and regulations, including card scheme rules, related to use of these types of payment methods, the emergence of alternative payment products, or the general public’s use of such alternative payment methods has, and may in the future reduce or change the use-cases for our products, and has and could continue to adversely affect our revenues, our results of operations and financial condition.

The future success of our business depends upon the continued use of credit and debit cards and other payment methods as a primary means to pay for online purchases and conduct commercial transactions that expose our merchants to the risk of payment fraud. Federal, state or foreign government bodies or agencies have in the past adopted, and may in the future adopt, laws or regulations affecting the use of such payment methods, including with respect to card-not-present transactions. In addition, card schemes such as Visa, Mastercard and American Express, impose rules and other requirements on participants in the payment chain. Changes in these laws, regulations or card scheme rules and terms and conditions of other payment providers could require us to modify our products in order to comply with these changes.

In addition, the adoption, implementation and evolution of laws, regulations or card scheme rules that operate to reduce fraudulent transactions, shift liability for certain transactions away from merchants and on to other participants in the payments chain, or route transactions through networks or payments rails with different chargeback rules may adversely affect the use-cases and demand for our products, our business, financial condition, and results of operations or require us to make changes to our business and strategies. In addition, to the extent the performance of strong factor authentication protocols, such as 3D Secure, improves over time, or merchant risk profiles or consumer preferences shift over time, we may begin to see merchants electing to voluntarily adopt similar protocols with respect to online transaction volume. The adoption of 3D Secure or other strong factor authentication protocols that reduce online payment fraud, or shift the liability for online payment fraud away from the merchant, may reduce the

8

demand or use-cases for our products, reduce the GMV available for us to review, and could adversely affect our revenues, our results of operations and financial condition.

Further, we depend upon the general public’s continued willingness to use credit cards and other payment methods that expose our merchants to the risk of payment fraud as a primary means to pay for online purchases and conduct commercial transactions. While we are able to review and guarantee transactions completed using alternative ecommerce payment methods, such as Apple Pay, Google Pay and Paypal, the increased availability of, and adoption by our merchants and by the general public of these and other alternative payment methods (such as “buy now pay later” services, cryptocurrencies or “digital wallet” style products or real time payments, including those offered by large “traditional” financial institutions with large customer bases), which may be less susceptible to fraud, include native fraud management features, sit outside of the broader chargebacks regime or allow liability for online transactions to be shifted away from merchants, may reduce the attractiveness or use-cases of our products, reduce demand for our products and the GMV available for us to review, and may adversely affect our business, financial condition, and results of operations.

We have a history of net losses and there are no assurances that we will achieve profitability in the future.

We have not been profitable since our inception in 2012 and have incurred significant net losses in prior years, including net losses of $59.0 million and $104.7 million for the years ended December 31, 2023 and 2022, respectively. While we have implemented certain cost reduction measures, we anticipate that our non-GAAP operating expenses may increase modestly over the next several years as we continue to strategically hire, expand our partnerships, operations, and infrastructure, continue to expand and enhance our products, and increase our spending on sales and marketing. In addition, our ability to achieve and maintain profitability will depend, in part, on our ability to effectively manage and decrease our chargeback expenses, which is dependent on our ability to improve the accuracy of our products. The accuracy of our products is, in part, driven by the amount of information we are able to obtain from processing transactions. In addition, higher rates of inflation in the U.S. and globally, and demand for high-tech personnel in Israel, have impacted, and may continue to impact our costs of labor and the prices at which we are able to acquire goods and services from third-party vendors on which we rely. In many instances, we are not able to increase the prices at which we sell our products and services to offset these higher costs, either partially or at all. We intend to continue enhancing our existing products and may develop and introduce new products through internal research and development, and we may also selectively pursue acquisitions. These efforts may prove more expensive than we currently anticipate. If our revenue declines, or fails to grow at a rate sufficient to offset increases in our operating expenses, we may continue to generate losses and not be able to achieve and maintain profitability in future periods. In addition, our increased focus on expense discipline, dilution management, capital allocation initiatives, and path to profitability may require us to reduce the resources we can allocate to growth initiatives, which may in turn result in slower than anticipated revenue growth. We cannot assure you that we will become profitable, or that if we do become profitable, we will be able to sustain profitability.

If we are unable to attract new merchants, retain existing merchants or increase sales of our products to existing merchants, our business, financial condition and results of operations may be adversely affected.

Our growth is dependent on our ability to continue attracting new merchants while retaining existing merchants and expanding and enhancing the products we sell to them. In particular, if we are not able to attract new merchants and increase the amount of transactions we process within our existing merchant network, we may not be able to continue to improve our products. Growth in the demand for our products may also be inhibited, and we may be unable to grow our merchant base for a number of reasons, including, but not limited to:

9

•our failure to develop or offer new or enhanced products in a timely manner that are comparable with, or superior to, new technologies or competitor offerings, and that meet the evolving needs of our merchants and changes in the regulatory environment in which we operate;

•difficulties providing high quality support or maintaining a high level of merchant satisfaction, which could reduce demand for our products if existing merchants terminate their relationship with us or stop referring prospective merchants to us;

•increases in our merchant churn rates, including churn of significant merchants from whom we derive a significant percent of our revenue, which may occur for various reasons including, but not limited to, corporate reorganizations, mergers and acquisitions or bankruptcies affecting our merchant base;

•perceived or actual security, availability, integrity, privacy, reliability, quality, or compatibility problems with our products, including related to unscheduled downtime, outages, or network security breaches; and

•continued or increased competition in our industry, including greater marketing efforts or investments by our competitors in advertising and promoting their brands or in product development.

Our future success depends, in part, on our ability to sell additional products to our existing merchants. If our merchants do not purchase additional products from us, or do not renew their agreements upon expiration, our business, financial condition, and results of operations may be adversely affected.

Our merchant expansions and renewals may decline or fluctuate as a result of a number of factors, including merchant usage, merchant satisfaction with our products and ecommerce risk intelligence platform capabilities and merchant support, our prices, the prices of competing products, corporate reorganizations, mergers and acquisitions or bankruptcies affecting our merchant base, consolidation of affiliates’ multiple paid business accounts into a single paid business account, the effects of global economic conditions, including recession and inflation, or reductions in our merchants’ spending levels generally. These factors may be exacerbated if, consistent with our growth strategy, our merchant base continues to grow to encompass large online enterprises.

Our revenue is impacted, to a significant extent, by macroeconomic conditions and the financial performance of our merchants.

Our business, the ecommerce retail sector, and our merchants’ businesses are sensitive to macroeconomic conditions. Economic factors, such as interest rates, inflation, currency exchange rates, changes in monetary and related policies, market volatility, consumer confidence, recession or recessionary indicators, supply chain issues, unemployment rates, shifts in consumer spending patterns (for example, between goods and services), and real wages, are among the most significant factors that impact consumer spending behavior. Weak economic conditions or a significant deterioration in economic conditions, including prolonged recession with sustained high interest rates and unemployment rates, may reduce the amount of disposable income available to consumers, which, in turn, reduces consumer spending and merchant transaction volumes. This has had, and may continue to have an adverse effect on our business, financial condition, and results of operations.

In particular, there are certain industries, including the luxury goods industry, that are particularly susceptible to recession and other macroeconomic conditions, such as inflation, that may reduce consumer discretionary spending. Similarly, external macroeconomic factors and business conditions including global supply chain disruptions, such as those experienced in many industries in recent years, have resulted in and may in the future result in shortages of raw products and prolonged shipping and delivery times for consumer goods. This may in turn lead to decreased ecommerce transaction volumes as consumers instead opt to purchase stock-on-hand from bricks-and-mortar retailers, rather than

10

transact through digital channels. Any reduction in our merchants’ transaction volume directly impacts the revenue we derive from them and, if such reduction continues for a prolonged period, would have a material adverse effect on our business, financial condition and results of operations.

Our ability to review transactions for fraud, and the fees due to us associated with providing such products, depends upon sales of products and services by our merchants. Certain of our merchants’ sales have and may in the future decrease or fail to increase at rates consistent with prior performance, current expectations, or at all, as a result of factors outside of their control, such as the macroeconomic conditions referenced above, or business conditions affecting a particular industry vertical or region. For example, we continued to see softness in certain industry verticals, including “Fashion & Luxury”, “Home” and “General Retail” throughout 2023, which we believe is partially attributable to a slowdown in consumer discretionary spending as a result of macroeconomic pressures. In our experience, weak economic conditions can also extend the length of our merchants’ sales cycles, and cause consumers to delay making (or not make) purchases of our merchants’ products and services. Even in the absence of macroeconomic factors, the performance of our merchants directly impacts our business, and, as a result, if the sales volume and financial performance of a merchant is negatively impacted for reasons specific to such merchant, our revenues will be negatively impacted. In addition, a reduction in online engagement generally or for any of our individual merchants, including due to a general decrease in online spending or a decreased demand for any of our merchants’ products or services for any reason could lead to a decrease in our merchants’ ecommerce revenues, which, in turn, would harm our revenues or reduce the attractiveness of our products.

If we are unable to continue to improve our machine learning models or if our machine learning models contain errors or are otherwise ineffective, our growth prospects, business, financial condition, and results of operations may be adversely affected.

Our products are based on our machine learning models and our ability to attract new merchants, retain existing merchants, or increase sales of our products to existing merchants will depend in large part on our ability to maintain a high degree of accuracy and automation in our automated decisioning process. Maintaining or improving the level of accuracy in our automated decisioning process in turn allows us to maintain or improve approval rates for our merchants over time. If our machine learning models fail to accurately detect fraud, detect fraud quickly enough or correctly categorize new risks relating to fraud, or if any of the other components of our automated decisioning process fail, we will typically experience higher than forecasted chargebacks, which in turn puts downward pressure on our gross margins, and may impact our ability to attract new merchants, retain existing merchants or increase sales of our products to existing merchants and our business, financial condition, and results of operations may be adversely affected.

Our machine learning models are designed to analyze data attributes to identify complex transaction and behavior patterns, which enables us to detect fraud and illegitimate consumers quickly and accurately. Our ability to accurately detect fraud even as methods of committing fraud evolve and become more sophisticated is dependent on our ability to continuously improve and train these models. However, it is possible that our machine learning models may prove to be less accurate than we expect, or than they have been in the past, for a variety of reasons, including inaccurate assumptions or other errors made in building or training such models, incorrect interpretations of the results of such models, increased fraud sophistication beyond the capabilities of our machine learning models, and failure to timely update model assumptions and parameters. For example, in the third quarter of 2023, one of our merchants experienced a significant fraud event. In this instance, our machine learning models were not able to effectively block the relevant fraudulent transactions. In addition, because we had not correctly predicted the scope of the fraud event, the overall risk level in the merchant’s account was underrepresented at the time the event occurred. The combination of these factors meant that we were unable to mitigate the effects of the fraud event quickly enough, which impacted our quarterly gross profit. In addition, our machine learning models may initially be less accurate following expansion into new industry verticals, geographic regions and use-cases, such as review of automated clearing house (“ACH”) payments or covering non-fraud related chargebacks. Further, the successful performance of our machine learning

11

models relies on the ability to constantly review and process large amounts of transactions and other data. If we are unable to attract new merchants, retain existing merchants or increase sales of our products to existing merchants, or if our merchants do not provide us with access to a significant volume of their transaction data or if the number of transactions processed by our existing merchants declines, the amount of data reviewed and processed by our machine learning models will be reduced or may fail to grow at a pace that will allow us to continue to improve the efficiency of our machine learning models, which may reduce the accuracy of such models. Additionally, such models may not be able to effectively account for matters that are inherently difficult to predict or are otherwise beyond our control, such as social engineering and other methods of perpetrating fraud that do not lend themselves well to risk-based analysis. Material errors or inaccuracies in such machine learning models could lead us to make inaccurate or sub-optimal operational or strategic decisions, which could adversely affect our business, financial condition and results of operations. Our inability to train our models or develop new technology that can detect new fraud schemes may also result in significant chargeback expenses, which would materially and adversely impact our business, financial condition, and results of operations.

The data gathering for, and development of, our machine learning models have predominantly occurred during a period of sustained economic growth, and our machine learning models have not been extensively tested during a down-cycle economy or recession. For example, consumer spending patterns, transaction volumes and fraud patterns experienced during a down-cycle economy or recession may differ from those experienced during periods of sustained economic growth. There is no assurance that our machine learning models can continue to accurately detect fraud under adverse economic conditions. If our machine learning models are unable to accurately detect fraud under such economic conditions, the performance of our product may be worse than anticipated and we may be required to issue a significant amount of credits as a result of valid chargebacks, which would adversely affect our business, financial condition and results of operations.

Our CTB Ratio and gross profit margin have historically fluctuated from quarter-to-quarter and we expect that to continue. These metrics are managed, and should be analyzed, on an annual basis.

Our CTB Ratio and gross profit margin are managed, and are best analyzed, on an annual basis. Historically, our CTB Ratio and gross profit margin have fluctuated between periods, and we expect that these financial metrics will continue to fluctuate between periods in the future, based on a number of factors, including changes in the mix of our merchant industry base, our entry into new geographies and industries, shifts from credit and debit cards towards alternate payment methods, the risk profile of orders approved in the period, technological improvements in the performance of our models, seasonality, large-scale merchant fraud events or security incidents, expansion into other use-cases and other factors. For example, our CTB Ratio and gross profit margins are sometimes negatively impacted in the first several quarters following the onboarding of merchants in new industry verticals or geographic regions, as our machine learning models adapt to the unique fraud patterns and other characteristics associated with transaction volume in those industries or regions. Model performance will generally normalize over time as our machine learning models gather more data and their accuracy improves. We believe that similar trends will continue to affect our future quarterly performance. In addition, order populations in certain industry verticals or geographic regions may be more or less risky. For example, historically “tickets and travel” has been a higher-risk, lower-margin industry, while other industry verticals, such as “electronics” and “fashion, cosmetics and luxury goods” have been lower-risk, higher-margin industries. Any change in our merchant industry mix between periods is likely to impact our CTB Ratio and gross profit margin between periods.

Our products enable the collection and storage of personal, confidential or proprietary information of our merchants and their consumers, and security concerns could result in liability to us or inhibit sales of our products.

In conducting our business, we rely heavily on computer systems, hardware, software, technology infrastructure and online websites and networks (collectively, “IT Systems”), including those of third-party service providers, for both internal and external operations. Our operations involve the storage,

12

transmission and processing of our merchants’ and their consumers’ confidential proprietary data, which can include personal information. Because we make extensive use of third-party suppliers and service providers, successful cyberattacks against such third parties’ IT Systems can also materially impact our operations and financial results. While we have developed systems and processes to protect our IT Systems and the integrity, confidentiality, availability and security of such data, our security measures or those of our third-party service providers, including, but not limited to, the third-party providers of cloud-based infrastructure, or Public Cloud Providers, have in the past and could in the future result in unauthorized access to or disclosure, modification, misuse, loss or destruction of such data. Any security breaches, computer malware, ransomware or extortion based attack, exploited hardware or software bugs, distributed denial-of-service (“DDoS”) attacks, misconfigurations or similar vulnerabilities experienced by us or by our third-party service providers, including from diverse threat actors, such as state-sponsored organizations, opportunistic hackers and hacktivists, could expose us to a risk of loss of personal, confidential or proprietary information, operational disruptions, loss of business, severe reputational damage adversely affecting merchant or investor confidence, regulatory investigations and orders, litigation (including class action lawsuits), indemnity obligations, damages for contract breach, fines and penalties for violation of applicable laws or regulations, and significant costs for remediation and incentives offered to merchants or other business partners in an effort to maintain business relationships after a breach, and other liabilities.

We regularly experience and expect to continue to experience actual and attempted cyber-attacks on our IT Systems, such as through phishing scams and ransomware. Additionally, in the aftermath of Hamas’ attack on Israel on October 7, 2023, many Israeli websites reported a significant increase in DDoS attacks. Although none of these actual or attempted cyber-attacks to date, individually or in the aggregate, has had a material adverse impact on our operations or financial condition, we cannot guarantee that such incidents will not have such an impact in the future. Cyberattacks and other malicious Internet-based activity continue to increase generally. If our products or security measures are perceived as weak or are actually compromised as a result of third-party action, employee or merchant error, malfeasance, stolen or fraudulently-obtained log-in credentials, or otherwise, our merchants may curtail or stop using our products, our reputation could be damaged, our business may be adversely affected, and we could incur significant liability. Further, because our products and services are integrated with our customers’ systems and processes, any circumvention, disruption or failure of our cybersecurity defenses or measures could compromise the confidentiality, integrity, and availability of our customers’ own IT Systems and/or our customers’ proprietary or other sensitive information which could result in legal claims or proceedings (such as class actions), regulatory investigations and enforcement actions, fines and penalties, negative reputational impacts that cause us to lose existing or future customers, and/or significant incident response, system restoration or remediation and future compliance costs. We may be unable to anticipate or prevent techniques used to obtain unauthorized access to or to sabotage systems because threat actors are becoming increasingly sophisticated in using techniques and tools – including artificial intelligence – that change frequently, may remove forensic evidence and generally are not detected until after an incident has occurred. As adoption of our products by merchants continues to increase and our brand becomes more widely known and recognized, we may become more of a target for third parties seeking to compromise our security systems or gain unauthorized access to our merchants’ data. Moreover, if a high-profile security breach occurs with respect to another cloud platform provider, our merchants and potential merchant customers may lose trust in the security of cloud platforms generally, which could adversely impact our ability to retain existing merchants or attract new ones. While we continue to implement controls and plans for preventative actions to further strengthen our IT Systems against future attacks, we cannot ensure that such measures will be fully implemented and complied with, provide adequate security, that we will be able to react in a timely manner, or that our remediation efforts following past or future attacks will be successful.

If we are not able to detect activity on our ecommerce risk intelligence platform that might be nefarious in nature or if we are not able to design processes or systems to reduce the impact of similar activity on a platform of a third-party service provider, our merchants could suffer harm. In such cases, we could face exposure to legal claims, particularly if a merchant suffers actual harm.

13

There can be no assurance that our cybersecurity risk management program and processes, including our policies, controls or procedures, will be fully implemented, complied with or effective in protecting our systems and information. Any adverse impact to the availability, integrity or confidentiality of our IT Systems may result in significant incident response, system restoration or remediation and future compliance costs. We cannot assure you that any limitation of liability provisions in our contracts for a security lapse or breach would be enforceable, adequate or would otherwise protect us from any liabilities or damages with respect to any particular claim related to such lapse or breach. We also cannot be sure that our existing insurance coverage will continue to be available on acceptable terms or will be available in sufficient amounts to cover one or more large claims related to a security breach, or that the insurer will not deny coverage as to any future claim. Our existing general liability and cyber liability insurance policies may not cover, or may cover only a portion of, any potential claims related to security lapses or breaches to which we are exposed or may not be adequate to indemnify us for all or any portion of liabilities that may be imposed. We also cannot be certain that our existing insurance coverage will continue to be available on economically reasonable terms or in amounts sufficient to cover the potentially significant losses that may result from a security incident or breach, which could therefore have a material adverse effect on our business, financial condition and results of operations.

Lengthy sales cycles with large enterprises make it difficult to predict our future revenue and may cause variability in our operating results.

Our sales cycle can vary substantially from merchant to merchant, but with large enterprises it typically requires 25 to 55 weeks on average from the time we designate a merchant as a sales qualified lead to execution of an agreement with that merchant. Our ability to forecast revenue accurately is affected by our ability to forecast new merchant acquisitions. Lengthy sales cycles make it difficult to predict the quarter in which revenue from a new merchant may first be recognized. If we overestimate new merchant growth in a particular period or generally, our revenue will not grow as quickly as our forecasts, our costs and expenses may continue to exceed our revenue, and our results of operations will be adversely affected. In addition, we may not meet or may be required to revise guidance that we have provided to the public, if any.

In addition, we plan our operating budget, including sales and marketing expenses, and our hiring needs, in part, based on our forecasts of new merchant growth and future sales. If new merchant growth or sales for a particular period is lower than expected, we may not be able to proportionately reduce our operating expenses for that period, which could harm our operating results for that period. Delays in our sales cycles could cause significant variability in our revenue and operating results for any particular period.

We have experienced in the past, and expect to continue to experience, seasonal fluctuations in our revenues. If we fail to accommodate increased volumes during peak seasons and events, our business, financial condition, and results of operations may be adversely affected.

Our business is seasonal in nature and our GMV and revenues are typically highest in the calendar fourth quarter. Our revenue is directly correlated with the level of revenue that our merchants generate, and our merchants typically generate the most revenue in the calendar fourth quarter, which includes Black Friday, Cyber Monday, the holiday season, and other peak events included in the ecommerce calendar, such as Chinese Singles’ Day and Thanksgiving. Our gross profit margin typically follows a similar trend. For the years ended December 31, 2023 and 2022, calendar fourth quarter revenue represented approximately 28% and 30% of our total revenues, respectively. As a result, our revenue will typically decline in the calendar first quarter of each year relative to the calendar fourth quarter of the previous year.

Any service disruption affecting our products, especially during the calendar fourth quarter, could have a negative effect on our operating results. Surges in volumes during peak periods may strain our technological infrastructure and merchant support activities, which may reduce our revenue and the attractiveness of our products.

14

Any disruption to our operations or the operations of our merchants during the calendar fourth quarter could lead to a material decrease in revenues relative to our expectations for the calendar fourth quarter, which could in turn result in a significant shortfall in revenue, results of operations and operating cash flows for the full year.

We operate in a highly competitive industry. Competition presents an ongoing challenge to the success of our business.

We operate in a highly competitive industry, and we expect competition to continue to increase. With the introduction of new technologies and the entry of new competitors into the market, including risk scoring companies that provide non-guaranteed decisions, typically at a lower price point, we expect competition to persist and intensify in the future. This could harm our ability to attract new merchants, increase sales, maintain or increase renewals, and maintain or increase our prices. We believe that our ability to compete depends upon many factors both within and beyond our control, including the following:

•the size of our merchant base;

•the timing and market acceptance of products, including the developments and enhancements to those products, offered by us or our competitors;

•the quality of our products and our merchant service and support efforts;

•our selling and marketing efforts;

•our continued ability to develop technology to support our business model;

•our continued ability to develop and implement new products to meet evolving merchant needs, use-cases and regulatory requirements;

•our continued ability to expand into and localize our products in new geographies and new industry verticals in a timely manner;

•the pricing structures and pricing practices employed by our competitors; and

•our brand strength relative to our competitors.

Many of our existing and potential competitors could have substantial competitive advantages, such as greater name recognition, longer operating histories, larger sales and marketing budgets, greater merchant support resources, lower labor and development costs, larger and more mature intellectual property portfolios and significantly greater financial, technical, marketing and other resources. Further, in addition to fraud detection and prevention, certain of our competitors may offer a more comprehensive portfolio of products and services, which may make them more attractive to potential merchants.

Our competitors may engage in more extensive research and development efforts, undertake more far-reaching marketing campaigns and adopt more aggressive pricing policies which may allow them to attract merchants. Our competitors may develop products that are similar to our products or that achieve greater market acceptance than our products, which could attract merchants away from our products and reduce our market share.

In addition, if one or more of our competitors were to merge or partner with another of our competitors, our ability to compete effectively could be adversely affected. Our competitors may also establish or strengthen cooperative relationships with our current or future strategic distribution and technology partners or other parties with whom we have relationships (i.e. channel partners), thereby limiting our ability to promote and implement our ecommerce risk intelligence platform.

These competitive pressures in our market, or our failure to compete effectively, may result in price reductions, lower transaction volumes, reduced revenue and gross profit margins, increased net losses,

15

merchant-churn and loss of market share. Any failure to meet and address these factors may adversely affect our business, financial condition and results of operations.

We have a substantial merchant concentration, with a limited number of merchants accounting for a substantial portion of our revenues. The loss of a significant merchant would materially and negatively affect our business, financial condition and results of operations.

We derive a significant portion of our revenues from a few significant merchants, each of which operates in the ecommerce retail sector. For the three years ended December 31, 2023, 2022 and 2021, our three largest merchants in the aggregate accounted for 28%, 25% and 30% of our revenues, respectively. In addition, our five largest merchants in aggregate accounted for approximately 38%, 34% and 39% of our revenues for the years ended December 31, 2023, 2022 and 2021, respectively. If any of these merchants experience declining or delayed sales or other business interruptions due to market, economic, or competitive conditions, the fees we receive from such merchant will decline proportionally. Further, because the retail sector, where most of our major merchants operate, is generally susceptible to macroeconomic factors, we too are susceptible to macroeconomic factors. See “Item 3.D. “Risk Factors-Risks Relating to our Business and Industry-Our revenue is impacted, to a significant extent, by macroeconomic conditions and the financial performance of our merchants.” In addition, we could be pressured to reduce our prices, make other contractual concessions or we could experience a decline in the demand for our products, any of which could negatively affect our business, financial condition, and results of operations. If any of our five largest merchants terminate their relationships with us, become subject to bankruptcy proceedings, or otherwise cease operating, such termination, bankruptcy or cessation of operations would materially negatively affect our business, financial condition, and results of operations. Furthermore, if any of our largest merchants terminate their relationships with us, or if these merchants experience declining or delayed ecommerce sales or other business interruptions, our estimates and forecasts relating to the size and expected growth of our market and our revenues may prove to be inaccurate.

The risk of losing merchants as a result of bankruptcies may be higher due to challenging macroeconomic conditions (including a recession), and could materially and negatively affect our business, financial condition and results of operations.

We have in the past had, and may in the future have, merchants, including significant merchants, whose financial condition deteriorates significantly, or who become subject to bankruptcy proceedings. In particular, merchants who are highly leveraged, operate on narrow margins, or are otherwise susceptible to changes in economic, competitive and market conditions, may be at an increased risk of bankruptcy in a recessionary environment. In addition to a reduction in these merchants’ ecommerce sales volumes, possibly to zero, we are not always able to recover amounts due to us from these merchants, which can have a material adverse impact on our business, financial condition, and results of operations.

If we are unable to develop enhancements to our products, increase adoption and usage of our products, and introduce new products and capabilities that achieve market acceptance, our business, financial condition and results of operations may be adversely affected.

Our ability to attract new merchants and increase revenue from existing merchants depends on numerous factors, including our ability to enhance and improve our existing products, increase adoption and usage of our products, and introduce new products and capabilities. In particular, if we are not able to develop technology that is able to keep pace with new and increasingly complex fraud schemes or that is able to solve new or different problems for our merchants, we may not be able to achieve a return on investment that satisfies our merchants. The success of any enhancements or new products depends on several factors, including timely completion, adequate quality testing, introduction to the market, and market acceptance. Any products we develop may not be introduced in a timely or cost-effective manner (or at all), may contain errors or defects, or may not achieve the broad market acceptance necessary to generate sufficient revenue. If we are unable to successfully enhance our existing products to meet

16

merchant requirements, increase adoption and usage of our products, or develop new products, our business, financial condition, and results of operations may be adversely affected.

If we are unable to continue to increase the sales of our products to large enterprises while mitigating the risks associated with serving such merchants, our business, financial condition and results of operations may be adversely affected.

Our growth strategy is dependent, in large part, upon the continued increase of sales to large enterprises. For the year ended December 31, 2023, we estimate that more than 90% of our Billings were derived from merchants generating over $75 million in online sales per year. Sales to large enterprises involve risks that may not be present or that are present to a lesser extent with sales to smaller entities, such as longer sales cycles, more complex merchant requirements, substantial upfront sales costs, and less predictability in completing some of our sales. For example, large enterprises may require considerable time to evaluate and test our applications and those of our competitors prior to making a purchase decision and placing an order. A number of factors influence the length and variability of our sales cycle, including the need to educate potential merchants about the uses and benefits of our products, the discretionary nature of purchasing and budget cycles, and the competitive nature of evaluation and purchasing approval processes. As a result, the length of our sales cycle may vary significantly from merchant to merchant, and sales to large enterprises typically take longer to complete. Moreover, large enterprises often request pilot periods or begin by deploying our products on a limited basis, but nevertheless require configuration, integration services, and pricing negotiations, which increase our upfront investment in the sales effort with no guarantee that these merchants will deploy our products widely enough across their organization to justify the substantial upfront investment. Our ability to improve our sales to such large enterprises is also partially dependent on our ability to continue to attract, train and retain sales personnel with experience selling to large enterprises, and competition for such personnel can be intense.

In addition, as security breaches with respect to larger, high-profile enterprises are likely to be heavily publicized, there is an increased reputational risk associated with serving such merchants. If we are unable to continue to increase sales of our products to large enterprises while mitigating the risks associated with serving such merchants, our business, financial condition, and results of operations may be adversely affected.

The loss of the services of any of our executive leadership team, including our co-founders, who are also our Chief Executive Officer and Chief Technology Officer, could materially and adversely affect our revenues, our results of operations and financial condition.

Our success and future growth depend largely upon the continued services of our executive officers and other key employees in the areas of research and development, marketing, business development, sales, products, and general administrative functions. In particular, the experiences of Eido Gal, our co-founder and Chief Executive Officer, and Assaf Feldman, our co-founder and Chief Technology Officer, are valuable assets to us. Mr. Gal and Mr. Feldman both have significant experience in developing automated risk and identity products and developing robust systems with machine learning algorithms and intelligent UIs for risk management applications and would be difficult to replace. Competition for senior executives in our industry is intense, and we may not be able to attract and retain qualified personnel to replace or succeed Mr. Gal, Mr. Feldman or other key executives. Failure to retain Mr. Gal, Mr. Feldman or other key executives would have a material adverse effect on our business, financial condition and results of operations.

In addition, executive leadership transition periods are often difficult as the new executives gain more detailed knowledge of our operations, and friction can result from changes in strategy and management style. Management turnover inherently causes some loss of institutional knowledge, which can negatively affect strategy and execution.

17

If we are unable to attract and retain executives and employees that we need to support our operations and growth, our revenues, our results of operations and financial condition may be adversely affected.

To execute our growth plan, we must attract and retain highly qualified personnel. Competition for these personnel is intense, especially for software engineers experienced in designing and developing software as a service (“SaaS”) applications and experienced sales professionals. Competition for talent in Israel has in the past been and remains intense. See Item 3.D. “Risk Factors ― Risks Relating to our Incorporation and Location in Israel — Due to competition for highly skilled personnel in Israel, we may fail to attract, recruit, retain and develop qualified employees, which could materially and adversely impact our business, financial condition and results of operations.” If we are unable to attract such personnel remotely or in cities or countries where we are located, we may need to hire in other locations which may add to the complexity and costs of our business operations. In particular, we recently established a research and development hub in Portugal in order to enhance and expand our talent pool and to help rationalize our labor costs. There can be no guarantee that we will be successful in continuing to hire in this region, that we will be successful in integrating our research and development teams across locations, or that such initiative will lead to meaningful and sustainable cost savings. From time to time, we have experienced, and we expect to continue to experience, difficulty in hiring and retaining employees with appropriate qualifications. Many of the companies with which we compete for experienced personnel have greater resources than we have. If we hire employees from competitors or other companies, their former employers may attempt to assert that these employees or we have breached their legal obligations, resulting in a diversion of our time and resources.

In addition, prospective and existing employees often consider the value of the equity awards they receive in connection with their employment, in addition to their cash compensation. The market price of our stock has experienced significant volatility. Significant declines in the value of our stock, has, and may in the future, impact our ability to compensate employees appropriately and to attract and retain talent. If the total compensation, including the amount or value of equity awards offered to employees is perceived to be less favorable than total compensation or equity awards offered by other companies with whom we compete for talent, or the perceived value of our equity awards declines, experiences significant volatility, or increases such that prospective employees believe that they are not being fairly compensated or that there is limited upside to the value of the Company’s equity awards, it may adversely affect our ability to recruit and retain key employees. If we fail to attract new personnel or fail to retain and motivate our current personnel, our business, financial condition and results of operations may be adversely affected.

In the event of continued stock price volatility in the future, we may determine that it is necessary to grant equity awards to our employees, outside of ordinary ranges, to recalibrate total compensation and help recruit and retain talent. Existing shareholders may experience significant dilution of their ownership interests as a result of such grants.

We may need to change our prices and pricing structure from time to time, which may negatively impact our business.

We typically charge our merchants a percentage of the value of the transactions that we approve. The fee we charge our merchants is a risk-adjusted price (based on a variety of factors including historical fraud levels, approval rate commitment, industry vertical and geographic region), which is expressed as a percentage of the GMV dollars that we approve. We expect we may need to change our pricing model from time to time, including as a response to updates or enhancements to our product suite, and in response to changes in global economic conditions or reductions in our merchants’ spending levels generally.

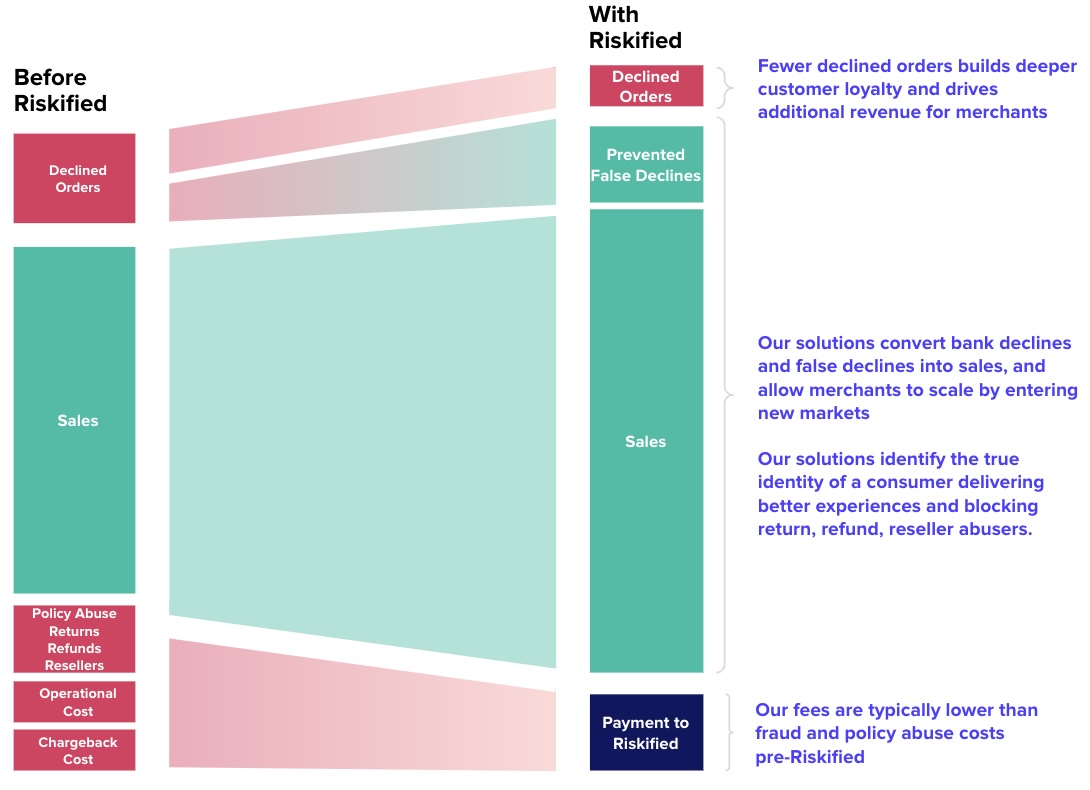

Through our Chargeback Guarantee product, we provide a Chargeback Guarantee to our merchants for transactions that our ecommerce risk intelligence platform approves that are subsequently determined to be fraudulent and for which a valid chargeback reimbursement request is received by our merchant. Pursuant to our Chargeback Guarantee, we may be required to issue a significant amount of credits to

18

merchants. The credit issued via the invoice we provide to our merchants generally equates to the approved transaction amount, which exceeds the fee we charge for the associated transaction. This business model requires us to accurately predict the amount of credits we expect to issue in order to determine the appropriate pricing structure for our products, and failure to do so may negatively affect our financial condition. While chargebacks are intended as a consumer protection mechanism from fraudulent transactions, they are also susceptible to abuse and “friendly fraud”. For example, friendly fraud may occur when a consumer, rather than returning an order they are dissatisfied with, instead initiates the chargeback process to avoid a complicated returns process. Friendly fraud may violate the merchant’s cancellation policies and, depending on the jurisdiction, may also be unlawful. Nevertheless, to the extent a chargeback reimbursement request is received by our merchants, even in instances of friendly fraud or other chargeback abuse, we may be required to issue significant credits to our merchants in respect of these transactions. While we employ a variety of strategies to minimize our exposure to friendly fraud and other chargeback abuses, it is often difficult to differentiate friendly fraud and other chargeback abuses from “true” fraud. Any increase in chargeback abuse, including friendly fraud, may impact the our ability to accurately predict the amount of credits we expect to issue in order to determine the appropriate pricing structure for our products, which could negatively impact our business operations and financial performance.

Similarly, as we introduce new products, or as a result of the evolution of our existing products, including reviewing ACH payments and covering non-fraud related chargebacks, and as the methods and techniques used to perpetrate fraud evolve, we may have difficulty determining the appropriate pricing structure for our products.