UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

Form 20-F

OR

For the fiscal year ended December 31 , 2023

OR

OR

Commission file number: 001-37959

(Exact name of Registrant as specified in its charter)

trivago Corporation

(Translation of Registrant’s name into English)

The Netherlands

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||||||||

Class A shares, nominal value €0.06 per share* | The NASDAQ Stock Market LLC* | |||||||||||||

| * | Not for trading, but only in connection with the registration of the American Depositary Shares. | ||||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

(as of December 31, 2023)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a "large accelerated filer," an "accelerated filer," a "non-accelerated filer" or an "emerging growth company."

Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐ Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒ Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued by the International Accounting Standards Board o | Other o | |||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

Table of contents

| Page | ||||||||

| 1 | ||||||||

| PART I | ||||||||

Item 1 | ||||||||

Item 2 | ||||||||

Item 3 | ||||||||

Item 4 | ||||||||

Item 4A | ||||||||

Item 5 | ||||||||

Item 6 | ||||||||

Item 7 | ||||||||

Item 8 | ||||||||

Item 9 | ||||||||

Item 10 | ||||||||

Item 11 | ||||||||

Item 12 | ||||||||

| PART II | ||||||||

Item 13 | ||||||||

Item 14 | ||||||||

Item 15 | ||||||||

Item 16A | ||||||||

Item 16B | ||||||||

Item 16C | ||||||||

Item 16D | ||||||||

Item 16E | ||||||||

Item 16F | ||||||||

Item 16G | ||||||||

Item 16H | ||||||||

Item 16I | ||||||||

| Item 16J | ||||||||

Item 16K | ||||||||

| PART III | ||||||||

Item 17 | ||||||||

Item 18 | ||||||||

Item 19 | ||||||||

General

As used herein, references to “we,” “us,” the “company,” or “trivago,” or similar terms in this Annual Report on Form 20-F mean trivago N.V. and, as the context requires, its subsidiaries. References to "Expedia Group" mean our majority shareholder, Expedia Group, Inc., together with its subsidiaries. References to our "Founders" mean Rolf Schrömgens, Peter Vinnemeier and Malte Siewert, collectively.

Our financial statements are prepared in accordance with U.S. Generally Accepted Accounting Principles, or U.S. GAAP. Unless otherwise specified, all monetary amounts are in euros. All references in this annual report to “$,” “US$,” “U.S.$,” “U.S. dollars,” “dollars” and “USD” mean U.S. dollars, and all references to “€” and “euros,” mean euros, unless otherwise noted.

Special note regarding forward-looking statements

This annual report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, that are based on our management’s beliefs and assumptions and on information currently available to our management. All statements other than present and historical facts and conditions contained in this annual report, including statements regarding our future results of operations and financial positions, business strategy, plans and our objectives for future operations, are forward-looking statements. When used in this annual report, the words “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “due,” “estimate,” “expect,” “goal,” “intend,” “may,” “objective,” “plan,” “predict,” “potential,” “positioned,” “seek,” “should,” “target,” “will,” “would,” and other similar expressions that are predictions of or indicate future events and future trends, or the negative of these terms or other comparable terminology identify forward-looking statements. Forward-looking statements include, but are not limited to, statements about:

•the extent to which our strategy of increasing brand marketing investments positively impacts the volume of direct traffic to our platform and grows our revenue in future periods without reducing our profits or incurring losses;

•the continuing negative impact of having ceased almost all television advertising in 2020 and only having resumed such advertising at reduced levels in recent years on our ability to grow our revenue;

•our reliance on search engines, particularly Google, whose search results can be affected by a number of factors, many of which are not in our control;

•the promotion by Google of its own products and services that compete directly with our accommodation search;

•our continued dependence on a small number of advertisers for our revenue and adverse impacts that could result from their reduced spending or changes in their cost-per-click, or CPC, bidding strategy;

•our ability to generate referrals, customers, bookings or revenue and profit for our advertisers on a basis they deem to be cost-effective;

•factors that contribute to our period-over-period volatility in our financial condition and result of operations;

•the potential negative impact of a worsening of the economic outlook and inflation on consumer discretionary spending;

•any further impairment of intangible assets;

1

•geopolitical and diplomatic tensions, instabilities and conflicts, including war, civil unrest, terrorist activity, sanctions or other geopolitical events or escalations of hostilities, such as the war in Ukraine and the ongoing conflict affecting the Middle Eastern region;

•increasing competition in our industry;

•our ability to innovate and provide tools and services that are useful to our users and advertisers;

•our business model's dependence on consumer preferences for traditional hotel-based accommodation;

•our dependence on relationships with third parties to provide us with content;

•changes to and our compliance with applicable laws, rules and regulations;

•the impact of any legal and regulatory proceedings to which we are or may become subject; and

•potential disruptions in the operation of our systems, security breaches and data protection.

You should refer to the section of this annual report titled “Item 3: Key information - D. Risk factors” for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this annual report will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this annual report and the documents that we reference in this annual report and have filed as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

2

Summary of our risk factors

Our business is subject to numerous risks that you should be aware of before making an investment decision. These risks are described more fully in "Item 3: Key information - D. Risk factors". These risks include, among others:

Risks related to the general economic and geopolitical environment, the travel industry and our business

•We recently announced a strategy to increase brand marketing investments, with the aim of increasing the volume of direct traffic to our platform in the long-term. This strategy may not enable us to grow our revenue in future periods, or at rates deemed sufficient by the market without reducing our profits or incurring losses.

•We rely on search engines, particularly Google, to drive a substantial amount of traffic to our platform. Google continues to promote its own products and services that compete directly with our accommodation search at the expense of traditional keyword auctions and organic search. If we are unable to drive traffic cost-effectively, direct traffic to our platform could continue to decline and our business would be negatively affected.

•If TV or other brand marketing advertising becomes less effective or if we experience diminishing returns from investments in such advertising, overall or in key markets, our planned brand marketing campaigns may not be as successful in terms of Return on Advertising Spend (ROAS) as our broad-reaching TV marketing campaigns had been prior to the COVID-19 pandemic.

•The number of users we attract from search engines to our platform is due in large part to how and where information from, and links to, our websites are displayed on search engine pages. The display, including rankings, of search results can be affected by a number of factors, many of which are not in our control. Google and other search engines frequently update and change the logic that determines the placement and display of results of a user’s search.

•We derive a very large portion of our revenue from a small number of advertisers. Any reduction in spending or any change in the bidding strategies by any of these advertisers could harm our business and negatively affect our financial condition and results of operations.

•We cannot reliably predict our advertisers' future advertising spend or CPC levels or other strategic goals they hope to achieve through changes in bidding on our marketplace and, as a result, it is difficult for us to forecast advertiser demand, especially since our advertisers can and often do change their CPC bidding levels with little or no notice to us.

•We are subject to a number of factors that contribute to significant period-to-period volatility in our financial condition and results of operations.

•We are dependent on general economic conditions, and declines in travel or discretionary spending could reduce the demand for our services.

•As a result of the change in the macroeconomic outlook, we have experienced and may in the future record impairments of intangible assets.

•Increasing competition in our industry could result in a loss of market share and higher traffic acquisition costs or reduce the value of our services to users and a loss of users, which would adversely affect our business, results of operations, financial condition and prospects.

•Any change in the global geopolitical environment, including any escalation or unexpected change in circumstances in the ongoing military conflict between Russia and Ukraine or the ongoing conflict affecting the Middle Eastern region, may have a negative impact on our business.

3

•If we do not innovate and provide tools and services that are sufficiently useful to users and advertisers, we may not remain competitive, and our revenue and results of operations could suffer.

•Several of our product features depend, in part, on our relationship with third parties to provide us with content and services.

Legal and regulatory risks

•We are involved in various legal proceedings and may experience unfavorable outcomes, which could adversely affect our reputation, business and financial condition.

•Regulators' continued focus on the consumer-facing business practices of online travel companies may adversely affect our business, financial performance, results of operations or business growth.

•We process, store and use user and employee personal data, which entails reputational, litigation and liability risks associated to any actual or perceived potential failure to comply with relevant legal obligations and regulatory guidance, which are constantly evolving.

Operational risks

•The competition for highly skilled personnel, including senior management and technology professionals is intense. If we are unable to retain or motivate key personnel or hire, retain, and motivate qualified personnel, especially as the broader job market undergoes structural changes that increase our costs, our business would be harmed.

•We are dependent upon the quality of traffic in our network to provide value to our advertisers, and any failure in our ability to deliver quality traffic and/or the metrics to demonstrate the value of the traffic could have a material and adverse impact on the value of our websites to our advertisers and adversely affect our revenue.

•We rely on assumptions, estimates and data to make decisions about our business, and any inaccuracies in, or misinterpretation of, such information could negatively impact our business.

•We may experience difficulties in implementing new business and financial systems.

•Increased computer circumvention capabilities could result in security breaches in our information systems, which may significantly harm our business.

•Any significant disruption in service on our websites and apps or in our computer systems, most of which are currently hosted by third-party providers, could damage our reputation and result in a loss of users, which would harm our business and results of operations.

•We rely on information technology to operate our business and maintain our competitiveness, and any failure to invest in and adapt to technological developments and industry trends could harm our business.

•Any use of artificial intelligence/machine learning (AI/ML) technologies in our operations may present additional legal, regulatory, and social risks, which could lead to additional costs and impact our competitive position.

•Our brand is subject to reputational risks and impairment.

Risks related to our ongoing relationship with our shareholders

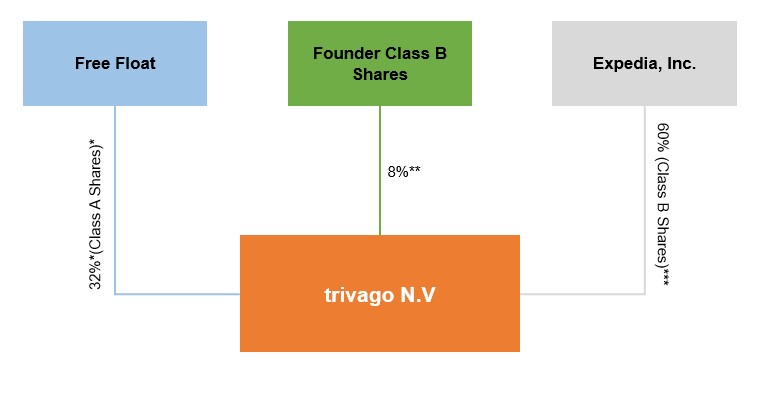

•Expedia Group controls our company and has the ability to control the direction of our business.

•Expedia Group’s interests may conflict with our interests, the interests of the Founders and the interests of our shareholders, and conflicts of interest among Expedia Group and us could be resolved in a manner unfavorable to us and our shareholders.

4

PART I

Item 1: Identity of directors, senior management and advisers

Not applicable.

Item 2: Offer statistics and expected timetable

Not applicable.

Item 3: Key information

A. [Reserved]

Not required.

B. Capitalization and indebtedness

Not applicable.

C. Reasons for the offer and use of proceeds

Not applicable.

D. Risk factors

Our business faces significant risks. You should carefully consider all of the information set forth in this annual report and in our other filings with the United States Securities and Exchange Commission, or the SEC, including the following risks that we face and that are faced by our industry. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. This annual report also contains forward-looking statements that involve risks and uncertainties. Our results could materially differ from those anticipated in these forward-looking statements as a result of certain factors including the risks described below and elsewhere in this annual report and our other SEC filings. See “Special note regarding forward-looking statements” above. For a summary of these risk factors, see "Summary of our risk factors" above.

Risks related to the general economic and geopolitical environment, the travel industry and our business

We recently announced a strategy to increase brand marketing investments, with the aim of increasing the volume of direct traffic to our platform in the long-term. This strategy may not enable us to grow our revenue in future periods, or at rates deemed sufficient by the market without reducing our profits or incurring losses.

We almost completely ceased advertising on television in 2020 and resumed such advertising at reduced levels in recent years. We believe our prior television advertising campaigns continued to have a significant positive effect, albeit one that diminishes over time, on direct traffic volumes to our platform in periods after the advertising was aired. As we continue to see diminishing returns from prior brand marketing campaigns, our financial performance has been negatively impacted. We have experienced declines in direct traffic volumes to our platform and a reduction in revenue of 9.3% in 2023, compared to

5

2022. We have decided to increase our brand marketing investments to increase the volume of direct traffic to our platform. Our planned increases in brand marketing investments are expected to negatively impact our profitability in the short-to-medium term and there can be no assurances that this revised strategy will succeed.

The success of our brand marketing investments depends on consumers’ awareness of the trivago brand, perceived quality and perceived differentiated attributes of our brand, and to what extent those efforts help us attract and expand the number of users of our websites and apps. If TV or other brand marketing advertising becomes less effective or if we experience diminishing returns from investments in such advertising, overall or in key markets, our planned brand marketing campaigns may not be as successful in terms of Return on Advertising Spend (ROAS) as our broad-reaching TV marketing campaigns had been prior to the COVID-19 pandemic. As we make our planned investments, we may observe increasing prices in light of increased spending from competitors or may see reduced benefits from our advertising due to, among other things, increasing traffic share growth of search engines as destination sites for users and the declining viewership in certain age groups and changes in viewing patterns that reduce viewer exposure to advertising. As we develop new creative concepts in our advertisements, our new advertisements may not be as effective in terms of ROAS as those we have used in the past. Our competitors may also invest in innovative advertisement campaigns to improve their brand awareness, which could make it difficult for us to increase or maintain our own marginal returns on our advertisements, despite our planned investments in brand marketing.

We anticipate the decline in viewership on traditional linear television to persist as consumers shift to other digital formats, such as streaming platforms and online video. As a result, we have begun investing in other channels with which we have less experience, including non-linear TV advertising formats and social media which may prove less effective than TV advertising in the long run and potentially lead to a lower marginal ROAS. If we are unable to maintain or enhance consumer awareness of our brand or to generate additional revenue in a cost-effective manner, it may have a material adverse effect on our business, results of operations, financial condition and prospects.

We rely on search engines, particularly Google, to drive a substantial amount of traffic to our platform. Google continues to promote its own products and services that compete directly with our accommodation search at the expense of traditional keyword auctions and organic search. If we are unable to drive traffic cost-effectively, direct traffic to our platform could continue to decline and our business would be negatively affected.

We rely on Bing, Google, Yahoo! and other Internet search engines to generate a substantial amount of traffic to our websites, principally through the purchase of hotel-related keywords. We obtain a significant amount of traffic via search engines and therefore utilize techniques such as search engine optimization and search engine marketing to improve our placement in relevant search queries. The number of users we attract from search engines to our platform is due in large part to how and where information from, and links to, our websites are displayed on search engine pages. The display, including rankings, of search results can be affected by a number of factors, many of which are not in our control. Google and other search engines frequently update and change the logic that determines the placement and display of results of a user’s search. If a major search engine changes its algorithms in a manner that negatively affects the search engine ranking, paid or unpaid, of our websites or that of our third-party distribution partners, it may have a material adverse effect on our business, results of operations, financial condition and prospects. For example, we observed ad format tests on Google that negatively impacted traffic volumes to our platform in 2023. In addition, increased competition in keyword auctions can also negatively impact our business, results of operations, financial condition and prospects, For example, we observed higher levels of competition in keyword auctions that resulted in declines in traffic volumes in 2023, particularly in our Americas and Developed Europe segments.

In addition, certain search and metasearch companies may change their displays or rankings in order to promote their own competing products or services, or the products or services of one or more of our competitors. For example, Google, a significant source of traffic to our website, frequently promotes its own hotel search platform (which it refers to as “Google Hotel Ads”) at the expense of traditional keyword

6

auctions and organic search results. This presents a challenge since we have significantly less flexibility to acquire traffic for our website using that platform compared to traditional hotel-related keyword advertising. In addition, our major advertisers might not be amenable in some cases to our using their inventory to compete with them on Google Hotel Ads, which may present a further difficulty if Google continues to direct traffic in this manner. Google’s promotion of its own competing products, or similar actions by Google in the future that have the effect of reducing our prominence or ranking on its search results, could have a substantial negative effect on our business, results of operations, financial condition and prospects.

We derive a very large portion of our revenue from a small number of advertisers. Any reduction in spending or any change in the bidding strategies by any of these advertisers could harm our business and negatively affect our financial condition and results of operations.

Our "cost-per-click," or CPC, pricing for click-based advertising depends, in part, on competition among advertisers on our marketplace, with advertisers that pay higher CPCs generally receiving better advertising placement and more referrals from us. We continue to generate the great majority of our revenue from our largest OTA advertisers, including brands affiliated with Booking Holdings, such as Booking.com, Agoda and priceline.com, and those affiliated with our majority shareholder, Expedia Group, such as Brand Expedia and Hotels.com. The loss of any of our major advertisers, on some or all of our platforms, or a further reduction in the amount they spend, or a further concentration in Advertising Spend by one advertiser could result in significant decreases in our revenue and profit or negative impacts on our liquidity position.

Our ability to grow and maintain revenue from our advertisers is dependent to a significant extent on our ability to generate referrals, customers, bookings or revenue and profit for our advertisers on a basis they deem to be cost-effective. Any reduction in the value that we deliver to our advertisers or our ability to match the value delivered by our competitors may negatively affect CPC bids on our marketplace. Our advertisers’ spend on our platforms may also be adversely affected by other factors such as a weakening of their own financial or business conditions or external economic effects.

Even if we improve our product and deliver value to our advertisers, the fact that a very significant portion of our revenue is generated from brands affiliated with Booking Holdings and Expedia Group can permit these advertisers, depending on marketplace dynamics, to adjust their CPC bids and obtain the same or increased levels of referrals, customers, bookings or revenue and profit at a lower cost. This can occur if one or more advertisers with sufficient market share to influence our aggregate CPC levels change their return-on-investment targets for their spend on our marketplace. Our advertisers may curtail their spend on our platform in response to changes we may make to our product offering or strategy, which may also, in turn, negatively impact our revenue levels and profitability or increase the volatility on our marketplace.

We are subject to a number of factors that contribute to significant period-to-period volatility in our financial condition and results of operations.

Our financial condition and results of operations have varied and may continue to vary considerably from period-to-period. This was reflected in the quarter-to-quarter changes in our profitability and revenue in 2023 and earlier years. We cannot reliably predict our advertisers' future advertising spend or CPC levels or other strategic goals they hope to achieve through changes in bidding on our marketplace and, as a result, it is difficult for us to forecast advertiser demand, especially since our advertisers can and often do change their CPC bidding levels with little or no notice to us. Our advertisers often pursue different marketing strategies and have varying levels of competitiveness based on their own competitive position. We believe that our advertisers continuously review their advertising spend on our platform and on other marketing channels, and continuously seek to optimize the allocation of their spend among us and our competitors.

We regularly compete with our advertisers in auctions for search engine keywords on Google and other search engines and adjust our spend on search engine marketing based on trends we see in our results. Large advertisers' strategies regularly test how changes in their spend on our platform may affect the efficiency of their spend on these other marketing channels. If these tests indicate that there are financial

7

benefits from spending less on our platform, we would generate fewer referrals to our advertisers' websites, and as a result, our revenues and results of operations would be adversely affected.

Furthermore, any resulting changes in Referral Revenue, especially as a result of changes in CPC bidding levels by our largest advertisers, could result in our inability to reduce our Advertising Spend, particularly on television, quickly enough to respond to the change in revenue since we have historically placed orders for television advertising in advance of the campaign season. As we spend the great majority of our revenue on advertising, such a failure to reduce Advertising Spend quickly enough can have, and has in the past had, a sudden and significant adverse effect on our profitability and results of operations. This risk may be exacerbated by our strategy to increase our brand marketing investments. Any resulting inability to meet financial guidance that we may communicate to the market in the future may have a material adverse effect on our business, results of operations, financial condition and prospects.

We are dependent on general economic conditions, and declines in travel or discretionary spending could reduce the demand for our services.

Our results of operations and financial prospects are significantly dependent upon users of our services and the prosperity and solvency of the OTAs, hotel chains and independent hotels that have relationships with us. The global economic outlook continues to be highly uncertain, with an economic recession in some or all of our key markets still possible. Travel, including the booking of accommodation, is dependent on personal and business discretionary spending levels, which are directly affected by perceived or actual adverse economic conditions. Our results of operations and financial prospects continue to be significantly dependent upon the economic health of our users and the prosperity and solvency of the OTAs, hotel chains and independent hotels that have relationships with us.

As a result of the change in the macroeconomic outlook, we have experienced and may in the future record impairments of intangible assets.

We recorded a cumulative impairment charge of €196.1 million in 2023 in connection with our annual indefinite-lived intangible asset and goodwill impairment analysis, resulting in the elimination of the goodwill balance and a remaining intangible asset balance of €75.6 million on the consolidated balance sheet as of December 31, 2023. The impairment was driven by adjustments made to our profitability outlook arising from the announced strategy shift to long-term growth, share price decline during the third quarter of 2023, uncertainty in our operating environment, and the continued uncertainty in respect of the overall economic environment. We may record further impairment charges in the future due to further changes in the macroeconomic outlook.

Increasing competition in our industry could result in a loss of market share and higher traffic acquisition costs or reduce the value of our services to users and a loss of users, which would adversely affect our business, results of operations, financial condition and prospects.

We operate in an increasingly competitive travel industry. Many of our current and potential competitors, including hotels themselves (both hotel chains and independent hotels), and metasearch engines, such as Kayak, TripAdvisor, Skyscanner and Google Hotel Ads, locally focused metasearch engines, such as Check24, OTAs, such as Booking.com, Ctrip, TUI, trip.com and Brand Expedia, alternative accommodation websites, such as Airbnb and Vrbo, and other hotel websites, may have been in existence longer, may have larger user bases, may have wider ranges of products and services and may have greater brand recognition and customer loyalty in certain markets and/or significantly greater financial, marketing, personnel, technical and other resources than we do. Some of these competitors may be able to offer products and services on more favorable terms than we can. Google Hotel Ads and other metasearch websites, continue to expand globally, are increasingly competitive, have access to large numbers of users, and, in some cases, continue to adopt strategies and develop technologies and websites that are very similar to ours. In particular, Google has entered various aspects of the online travel market and has grown rapidly in this area, including by offering a flight meta-search product ("Google Flights"), a hotel meta-search product ("Google Hotel Ads"), a vacation rental meta-search product, a tours and activities product, an inspirational travel product, Google Travel (which is a planning

8

tool that aggregates its flight, tours and activities and hotel and packages products in one website), and by integrating its hotel meta-search products and restaurant information and reservation products into its Google Maps app. In addition, artificial intelligence (AI) has the potential to disrupt the online travel industry, possibly changing how travelers look for and book travel. AI's advancement could enable our competitors to enhance user experiences and operational efficiencies, potentially threatening our position in the market if we do not adopt and deploy artificial intelligence/machine learning (AI/ML) as quickly or as efficiently as our competitors. Further, the rapid pace of AI/ML’s development may require the investment of significant resources for us to remain competitive, and we may not receive commensurate returns if we are not successful in achieving the outcomes we expect (either on the timelines we expect or at all). The realization of any of these risks could result in higher traffic acquisition costs, lower CPC levels and reduced margins on our advertising services, loss of market share, reduced user traffic to our websites and reduced advertising by hotel companies and other accommodation advertisers on our websites.

Our business model and value proposition is focused primarily on providing users with search services for hotels. If user preferences shift from traditional hotel-based accommodation or if users expect our websites and apps to offer search for non-accommodation services, we may be unable to source and monetize that inventory to a sufficient degree.

Our success depends on continued innovation to provide features and services that make our websites and apps useful for users. While we have offered users the opportunity to search for alternative accommodation, such as vacation rentals, on our websites and apps, our primary historical focus has been on helping users search for accommodation at hotels. If user preferences shift away from traditional hotel-based accommodation, we may face challenges in integrating and monetizing new types of accommodation into our platform since those properties may have attributes substantially different from hotel rooms, our traditional area of focus. In addition, the online travel industry is rapidly evolving, and if we fail to predict the manner in which that market develops or if our competitors are able to acquire a larger share of the aggregate online accommodation searches at our expense, our financial performance may be harmed. In addition, we do not currently offer users the ability to search for air travel, rental cars, tours, cruises and other services with our advertisers, while they can book or otherwise obtain information about at least some of these services on the websites of nearly all of our major competitors. If we are unable to provide users with information they deem useful, or our competitors are able to provide more attractive offers for accommodation coupled with attractive offers for other services, or if our users demand to see more comprehensive offers akin to those of our competitors, this may have a substantial negative effect on our competitiveness, business, results of operations, financial condition and prospects.

If we do not innovate and provide tools and services that are sufficiently useful to users and advertisers, we may not remain competitive, and our revenue and results of operations could suffer.

Our competitors are constantly innovating in online accommodation-related services and features. As a result, we must continue to invest significant resources in research and development to continuously improve the speed, accuracy and comprehensiveness of our services. The emergence of alternative platforms and niche competitors who may be able to optimize services or strategies have required, and will continue to require, new and costly investments in technology. We have invested, and in the future may invest, in new business strategies and services to attain competitiveness. Some of the changes we are implementing may require us to make investments into what we perceive as longer-term profitable returns at the expense of short-term profitability, and as a result, we may continue to prioritize the quality of user experience over short-term monetization.

In the future, we may need to provide alternative hotel listing products, potentially including paid and non-paid placements, to ensure we have a competitive coverage of rates globally. These strategies and services may not succeed, and, even if successful, our revenue may not increase or we may not achieve the longer-term profitable returns that we expect. In addition, we may fail to adopt and adapt to new technology, especially as text-based Internet search, including through Google and Amazon, potentially moves to video and voice interfaces over the coming years, or we may not be successful in developing technologies that operate effectively across multiple devices and platforms. New developments in other

9

areas could also make it easier for competitors to enter our markets due to lower up-front technology costs. If we are unable to continue offering innovative services or do not provide sufficiently comprehensive results for our users, we may be unable to attract additional users and advertisers or retain our current users and advertisers, which may have a material adverse effect on our business, results of operations, financial condition and prospects.

If we do not provide a broad set of offers to our users, we may not remain competitive, and our revenue and results of operations could suffer.

Our ability to attract users to our services depends in large part on providing a comprehensive set of accommodation search results and a broad range of offers across price ranges. To do so, we maintain relationships with OTAs, hotel chains, independent hotels and alternative accommodation providers to include their data in our search results. Although we maintain a very large searchable database of properties from around the world, we do not have relationships with some significant potential advertisers, including some major hotel chains, many independent hotels, smaller chains and certain large providers of alternative accommodations. The risk associated with incomplete coverage in our search results may increase if we see lower user interest in accommodation at hotels, for example as a result of any travel restrictions or because user preferences shift away from hotels to alternative accommodation. In addition, consolidation among advertisers, which may occur at increasing levels because of the general global economic situation, or a change to more coordinated or centralized marketing activities within OTA groups and hotel chains, could reduce the number of offers we have available in our marketplace for each hotel. The realization of any of these risks could make us less popular to our users and reduce the revenue we generate from referrals.

Several of our product features depend, in part, on our relationship with third parties to provide us with content and services.

We currently license, and incorporate into our websites, content and technology services from third parties. As we continue to improve the overall quality of our products, we may introduce new features that require us to incorporate new content or services, and this may require us to license additional rights. We cannot be sure that such technology will be available on commercially reasonable terms, if at all. In particular, certain third parties provide us with map products, content such as consumer reviews that we provide to our users along with our proprietary rating scores and hotel related data and information. If any of our third-party data providers terminate their relationships with us, the information that we provide to users may be limited or the quality of the information may suffer, which may negatively affect the implementation of our strategic initiatives, users’ perception of the value of our product and our reputation.

Many events beyond our control, including geopolitical events, may adversely affect the travel industry.

Many events beyond our control can adversely affect the travel industry, with a corresponding negative impact on our business and results of operations. Natural disasters, including hurricanes, tsunamis, earthquakes or volcanic eruptions, and other natural phenomena, public health threats, such as outbreaks of the Zika virus, the Ebola virus, avian flu and, most recently, COVID-19, as well as other pandemics and epidemics, have disrupted normal travel patterns and levels in the past. The COVID-19 pandemic has had a significant negative impact on our global business volumes, particularly in 2020 and 2021 and a severe outbreak of new (vaccine-resistant) variants of these viruses, other airborne contagious diseases or another pandemic, may result in governmental authorities imposing or re-imposing restrictions and recommending precautions to mitigate the health crisis. The travel industry is also sensitive to other events that may discourage travel, such as work stoppages or labor unrest, political instability, regional hostilities. Any change in the global geopolitical environment, including any escalation or unexpected change in circumstances in the ongoing military conflict between Russia and Ukraine or the ongoing conflict affecting the Middle Eastern region, may have a negative impact on our business. We do not have insurance coverage against loss or business interruption resulting from war and terrorism, and we may be unable to fully recover any losses we sustain due to other factors beyond our control under our existing insurance coverage. The occurrence of any of the foregoing events may have a material adverse effect on our business, results of operations, financial condition and prospects.

10

Our global operations expose us to risks associated with currency fluctuations, which may adversely affect our business.

Our platform is available in a large number of jurisdictions outside the Eurozone. As a result, we face exposure to movements in currency exchange rates around the world. Changes in foreign exchange rates can amplify or reduce changes in the underlying trends in our Advertising Spend and revenue. A large portion of our advertising expenses are incurred in the local currency of the particular geographic market in which we advertise, with a significant amount incurred in U.S. dollar. Although we largely denominate our CPCs in euro and have relatively little direct foreign currency translation with respect to our revenue, we believe that our advertisers’ decisions on the share of their booking revenue they are willing to pay to us are based on the currency in which the hotels being booked are priced. Accordingly, we have observed that advertisers tend to adjust their CPC bidding based on the relative strengthening or weakening of the euro as compared to the local functional currency in which the booking with our advertisers is denominated. Currency exchange-related exposures also include but are not limited to re-measurement gains and losses from changes in the value of foreign denominated monetary assets and liabilities; translation gains and losses on foreign subsidiary financial results that are translated into euro upon consolidation; fluctuations in hotel revenue and planning risk related to changes in exchange rates between the time we prepare our annual and quarterly forecasts and when actual results occur.

We do not currently hedge our foreign exchange exposure. Depending on the size of the exposures and the relative movements of exchange rates, if we choose not to hedge or fail to hedge effectively our exposure, we could experience a material adverse effect on our financial statements and financial condition. As we have seen in some recent periods, in the event of severe volatility in foreign exchange rates, these exposures can increase, and the impact on our results of operations can be more pronounced. In addition, the current environment and the global nature of our business have made hedging these exposures more complex.

We are subject to counterparty default risks.

We are subject to the risk that a counterparty to one or more of our customer arrangements will default on its performance obligations. A counterparty may fail to comply with its commercial commitments, which could then lead it to default on its obligations with little or no notice to us. This could limit our ability to take action to mitigate our exposure. Additionally, our ability to mitigate our exposures may be constrained by the terms of our commercial arrangements or because market conditions prevent us from taking effective action. In addition, our ability to recover any funds from financially distressed or insolvent counterparties is limited, and our recovery rates in such instances have historically been very low. Because a majority of our accounts receivable are owed by Booking Holdings and Expedia Group, delays or a failure to pay by any of these advertisers could result in a significant increase in our credit losses, and we may be unable to fund our operations. Counterparties may also be located in countries where enforcement of our creditors’ rights is more difficult than in the countries where our major OTA advertisers are located. If one of our counterparties becomes insolvent or files for bankruptcy, our ability to recover any losses suffered as a result of that counterparty’s default may be limited by the liquidity of the counterparty or the applicable laws governing the bankruptcy proceedings, and in any event, the customers of that counterparty may seek redress from us, even though the booking with that counterparty was not conducted on our platform. In addition, almost all of our agreements with OTAs, hotel chains and independent hotels may be terminated at will or upon prior notice of thirty days or less by either party. In the event of such default or termination, we could incur significant losses or reduced revenue, which could adversely impact our business, results of operations, financial condition and prospects.

Legal and regulatory risks

We are involved in various legal proceedings and may experience unfavorable outcomes, which could adversely affect our reputation, business and financial condition.

We are involved in various legal proceedings and disputes involving alleged infringement of third-party intellectual property rights, competition and consumer protection laws, including, but not limited to, the legal proceedings described in the following risk factor and in "Item 8: Financial information - A.

11

Consolidated statements and other financial information - Legal Proceedings". These matters may involve claims for substantial amounts of money or for other relief that might necessitate changes to our business or operations. The defense of these actions has been, and will likely continue to be, both time consuming and expensive and the outcomes of these actions cannot be predicted with certainty. Determining provisions for pending litigation is a complex, fact-intensive process that requires significant legal judgment. It is possible that unfavorable outcomes in one or more such proceedings could result in substantial payments that would adversely affect our business, consolidated financial position, results of operations, reputation or cash flows in a particular period.

Regulators' continued focus on the consumer-facing business practices of online travel companies may adversely affect our business, financial performance, results of operations or business growth.

A number of regulatory authorities in Europe, Australia and elsewhere have initiated litigation and/or market studies, inquiries or investigations relating to online marketplaces and how information is presented to consumers using those marketplaces, including practices such as search results rankings and algorithms, discount claims, disclosure of charges, and availability and similar messaging. For example, on January 20, 2020, the Australian Federal Court issued a judgment in the Australian Competition and Consumer Commission's (ACCC) case against us regarding our advertising and website display practices in Australia. On April 22, 2022, the Australian Federal Court issued a judgment ordering us to pay a penalty of AUD 44.7 million. We paid the penalty balance of €29.6 million (AUD 44.7 million) in the second quarter of 2022 and costs arising from the proceedings. Parts of the court’s opinions included views that differed significantly from those of other national regulators and raised concerns about the function of our marketplace and the adequacy of disclosures to consumers regarding how advertisers that pay higher CPCs generally receive better advertising placement on our website. Since then, two purported class actions have been filed in Israel and Ontario, Canada, making allegations about our advertising and/or display practices broadly similar to aspects of the case brought by the ACCC. Plaintiffs’ motion for class certification in the Ontario action was denied on November 28, 2022. Plaintiffs have since filed a notice of appeal asking that the motion for class certification be granted. A hearing regarding that appeal took place on November 17, 2023, with a decision still pending. A case management hearing in the class action filed in Israel recently took place. The matter remains at a relatively early stage.

Should other national courts or regulators take a similar view of our business model to that of the Australian Federal Court and the ACCC, or should changes in our business practices or those prevalent in our sector following the attention brought on by this litigation or other regulatory matters reduce the attractiveness, competitiveness or functionality of our platform and the services we offer, or should our reputation or that of our sector continue to suffer, or should we have to pay substantial amounts due to any such regulatory action or proceeding, our business, results of operations, financial condition and prospects could be adversely affected.

In addition, many governmental authorities in the markets in which we operate are also considering additional and potentially diverging legislative and regulatory proposals that would increase the level and complexity of regulation of Internet display, disclosure and advertising activities. There also are, and will likely continue to be, an increasing number of laws and regulations pertaining to the Internet and online commerce that may relate to liability for information retrieved from, transmitted over or displayed on the Internet, display of certain taxes, charges and fees, online editorial, user-generated or other third-party content, user or other third-party privacy, data security, behavioral targeting and online advertising, taxation, liability for third-party activities and the quality of services.

We process, store and use user and employee personal data, which entails reputational, litigation and liability risks associated to any actual or perceived potential failure to comply with relevant legal obligations and regulatory guidance, which are constantly evolving.

Personal data information is increasingly subject to legislation and regulations, and the enforcement thereof, in numerous jurisdictions around the world. We are in particular subject to the EU (European Union) General Data Protection Regulation 2016/679 or “GDPR”, in effect since May 25, 2018, as well as the ePrivacy Directive (and local laws implementing the ePrivacy Directive) regarding the use of cookies

12

and similar technologies. Both of these pieces of legislation have recently led to the imposition of significant fines on various companies by EU data protection authorities and/or similar enforcement actions. Due to the global nature of our operations, we are subject to an ever changing and growing patchwork of privacy laws, including the UK GDPR and the UK Data Protection Act 2018, the Brazilian General Data Protection Law, the Canadian Personal Information Protection and Electronic Documents Act, India’s Digital Personal Data Protection Act, U.S. state privacy laws and others.

A number of these data protection laws (including the GDPR and the UK GDPR) contain restrictions on processing of personal data, including lawful processing ground, cross-border transfers of personal data, mandatory breach reporting to regulators and, under certain circumstances, to the individuals whose personal data was compromised in the breach.

Many other jurisdictions have adopted or are in the process of adopting data protection regulations, which are sometimes inconsistent or conflicting. While we strive to monitor and comply with this complex and ever-changing patchwork of laws, a failure or perceived or alleged failure by us or our third party providers to comply with data privacy requirements in one of the jurisdictions where we operate or target users may significantly harm our businesses, including by subjecting us to regulatory investigations or enforcement, lawsuits (including class actions), fines, sanctions or other penalties that could negatively affect our reputation, business, financial condition and results of operations. In general, negative publicity we might receive regarding any actual or perceived violations of consumer privacy rights, including fines and enforcement actions against us or other similarly placed businesses, may also impair consumers’ trust in our privacy practices and make them reluctant to give their consent to share their data with us. In addition, we could be adversely affected if data privacy regulations are expanded (through new regulation or through legal rulings) to require major changes in our business practices and we may incur substantial compliance-related costs and expenses that are likely to increase over time. Implementation of and compliance with these laws and regulations may be more costly or take longer than we anticipate, or could otherwise adversely affect our business operations, including by causing us to divert resources from other initiatives and projects to address these evolving compliance and operational requirements, all of which could negatively impact our financial position or cash flows.

Changes in, and continued implementation and enforcement of, international trade and anti-corruption laws and regulations could affect our ability to remain in compliance with such laws and regulations and could have a materially adverse effect on our business, results of operations, financial condition and prospects.

The United States (acting through, among other government agencies, the SEC, the U.S. Department of Justice and the U.S. Department of the Treasury, Office of Foreign Assets Control (OFAC)), as well as foreign authorities of other jurisdictions, such as the United Kingdom and the European Union, continue to be focused on the implementation and enforcement of economic and trade and anti-corruption laws and regulations, across industries. For example, U.S. sanctions broadly prohibit transactions conducted within U.S. jurisdiction in, with, involving or relating to certain countries and territories subject to comprehensive sanctions, including, currently, the Crimea, Donetsk, and Luhansk regions of Ukraine, Cuba, Iran, North Korea and Syria, and certain specifically designated individuals and entities (including the Government of Venezuela and those individuals and entities listed on OFAC's Specially Designated Nationals and Blocked Persons List), as well as parties owned (and with respect to the Government of Venezuela, owned or controlled) by such sanctioned individuals and entities. In addition, as a result of Russia’s invasion of Ukraine, governmental authorities in the United States, the European Union, and the United Kingdom, among others, launched an expansion of coordinated sanctions and export control measures, including targeted sanctions against certain individuals and entities and prohibitions or restrictions on new investments and other financial, commercial, or trade-based activities. We believe that our activities comply with applicable trade and anti-corruption laws and regulations, including the laws and regulations administered and enforced by OFAC, the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act. As applicable laws and regulations are enacted or amended, often with little or no advance notice, and the interpretations of those laws and regulations may evolve or come into conflict with other jurisdictions, we cannot guarantee that our programs and policies will be deemed compliant by all applicable regulatory authorities or at all times. In the event that our controls should fail or are found not to be in compliance for

13

any reasons, including as a result of changes to our products and services or the behavior of our advertisers, we could be subject to monetary damages, civil and criminal penalties or other regulatory action, litigation and damage to our reputation and the value of our brand.

We may not be able to adequately protect our intellectual property, which could harm the value of our brand and adversely affect our business.

We regard our intellectual property, including our business processes and other proprietary information, as critical to our success, and we rely on trademark, copyright and trade secret laws, domain name registration, confidentiality and non-disclosure procedures and contractual provisions and license agreements, where applicable, to protect our proprietary rights. If we are not successful in protecting our intellectual property, it could have a material adverse effect on our business, results of operations, financial condition and prospects.

Effective trademark and service mark protection may not be available in every country in which our services are provided. The laws of certain countries do not protect proprietary rights, such as trade secrets, to the same extent as the laws of the United States or Europe and, therefore, in certain jurisdictions, we may be unable to protect our proprietary technology adequately against unauthorized third-party copying or use, which could adversely affect our competitive position. In case of the introduction of new trademarks or logos, there is a risk of third parties with older, allegedly similar trademarks challenging the new brand. In addition, certain characteristics of the Internet, in particular the anonymity, may make the protection and enforcement of our intellectual property difficult and in some cases, even impossible. We have licensed in the past, and expect to license in the future, certain of our proprietary rights, such as trademarks, to third parties. These licensees may take actions that might diminish the value of our proprietary rights or harm our reputation, even if we have agreements prohibiting such activity. Moreover, we utilize intellectual property and technology developed or licensed by third parties, and we may not be able to obtain or continue to obtain licenses and technologies from these third parties at all or on reasonable terms. Also, to the extent that third parties are obligated to indemnify us for breaches of our intellectual property rights, these third parties may be unable to meet these obligations. Any of these events may have a material adverse effect on our business, results of operations, financial condition and prospects.

We have registered domain names for websites that we use in our business, such as www.trivago.com, www.trivago.de and www.trivago.co.uk. Our competitors could attempt to capitalize on our brand recognition by using domain names similar to ours. Domain names similar to ours have been registered in the United States and elsewhere, and in some countries the domain name “trivago,” or spelling variations of it, may be owned by other parties. We may be unable to prevent third parties from acquiring and using domain names that infringe on, are similar to, or otherwise decrease the value of, our brand or our trademarks or service marks. Protecting and enforcing our rights to our domain names and determining the rights of others may require litigation, which, whether or not successful, could result in substantial costs and diversion of management attention, as well as a loss in customer trust in the brand.

We are, and may in the future be, subject to legal claims alleging that we infringe, misappropriate or otherwise violate the intellectual property rights of third parties.

Our commercial success depends on our ability to conduct our business without infringing, misappropriating or otherwise violating any intellectual property owned by third parties. We may be subject to liability if our products, services, software or other technology, or the operations of our business infringe, misappropriate or otherwise violate the patents, copyrights, trademarks or other intellectual property rights of third parties. Intellectual property challenges have been increasingly brought against members of the travel industry, and third parties may bring legal claims, or threaten to bring legal claims, that their intellectual property rights are being infringed, misappropriated or otherwise violated by us, including by means of counterclaims against us as a result of the assertion of our intellectual property rights. Further, the use of AI/ML technologies in our operations may result in claims by third parties of infringement, misappropriation or other violations of intellectual property, including based on the use of large datasets to train the AI/ML technologies, or the use of output generated by AI/ML technologies, in

14

either case which may contain or be substantially similar to third-party material protected by intellectual property, including patents, copyrights or trademarks.

We do currently, and could in the future, face claims that we have infringed the intellectual property rights of others. Legal proceedings involving intellectual property rights are highly uncertain and can involve complex legal and scientific questions, and any claims against us or such providers could require us to spend significant time and money in litigation or pay damages. Such claims could also delay or prohibit the use of existing, or the release of new, products, services or processes, and the development of new technology or intellectual property. We cannot assure you that we will achieve a favorable outcome for any such claims, and any such actual or threatened claims (whether or not valid) could adversely impact our reputation and result in direct and indirect costs, all of which may have an adverse impact on our operations and financial performance. Even if we believe such third party claims are without merit, a court may hold that we have infringed, misappropriated or otherwise violated such intellectual property rights or we may settle claims to avoid the cost and uncertainty of litigation. If we were to be found liable for any such infringement, misappropriation or other violation, we could be required to rebrand, redesign, reengineer or modify our products and services (including our platform), pay substantial monetary damages, including possible treble damages and attorneys’ fees, or royalties and enter into costly license agreements (if available at all) to obtain the rights to use necessary technology, and we could be subject to injunctions preventing us from using some or all of our products, services or technology. Any payments we are required to make and any injunctions with which we are required to comply as a result of infringement claims could be costly.

Even if intellectual property claims brought by or against us are settled or resolved in our favor, because of the substantial amount of discovery required in connection with intellectual property litigation, there is a risk that some of our confidential or proprietary information could be compromised by disclosure during this type of litigation. In addition, there could be public announcements of the results of hearings, motions or other interim proceedings or developments, and if securities analysts or investors perceive these results to be negative, it could have a substantial adverse effect on the price of our securities.

Any of the foregoing could divert management’s attention and materially and adversely affect our business, financial condition, results of operations and cash flows.

Operational risks

The competition for highly skilled personnel, including senior management and technology professionals is intense. If we are unable to retain or motivate key personnel or hire, retain, and motivate qualified personnel, especially as the broader job market undergoes structural changes that increase our costs, our business would be harmed.

We believe our success has depended, and continues to depend, on the efforts and talents of our senior management and our highly skilled team members, including our software engineers and other technology professionals who are key to designing code and algorithms necessary to our business. Our workforce has declined from 1,247 on December 31, 2019 to 651 as of December 31, 2023. This reduction in workforce has resulted in the loss of institutional knowledge, relationships or expertise for critical roles. This reduction may also have a negative impact on employee morale and productivity, and could make it more difficult to retain valuable key employees, divert attention from operating our business, create personnel capacity constraints and hamper our ability to grow, develop innovative products and compete, any of which could impede our ability to operate or meet strategic objectives.

We continue to face intense competition for new talent as the broader job market appears to undergo structural changes that have further exacerbated the competitive environment. We compete with companies that have far greater financial resources than we do as well as companies that promise short-term growth opportunities and/or other benefits. These companies may be able to provide attractive offers to employees in critical roles who have gained valuable and marketable experience in our flat organizational structure. The competition for talent in our industry has in the past and may in the future increase our personnel expenses, which may adversely affect our results of operations. We have experienced changes to our senior management during 2023. We may be unable to hire or retain certain

15

high-performing employees, including senior management, when the price of our ADSs is low, as a significant portion of the compensation they receive consists of equity grants. If we do not succeed in attracting well-qualified employees, or retaining or motivating existing employees, including senior management, our business would be adversely affected. The loss of the services of any key individual could negatively affect our business.

We are dependent upon the quality of traffic in our network to provide value to our advertisers, and any failure in our ability to deliver quality traffic and/or the metrics to demonstrate the value of the traffic could have a material and adverse impact on the value of our websites to our advertisers and adversely affect our revenue.

We use technology and processes to monitor the quality of the internet traffic that we deliver to our advertisers and have identified metrics to demonstrate the quality of that traffic and identify low quality clicks such as non-human processes, including robots, spiders, the mechanical automation of clicking and other types of invalid clicks or click fraud. Even with such monitoring in place, there is a risk that a certain amount of low-quality traffic will be delivered to such online advertisers. Such low-quality or invalid traffic may be detrimental to our relationships with advertisers and could adversely affect our advertising pricing and revenue.

We rely on assumptions, estimates and data to make decisions about our business, and any inaccuracies in, or misinterpretation of, such information could negatively impact our business.

We take a data-driven, testing-based approach to managing our business, where we use our proprietary tools and processes to measure and optimize end-to-end performance of our platform. Our ability to analyze and rapidly respond to the internal data we track enables us to improve our platform and make decisions about allocating marketing spend and ultimately convert any improvements into increased revenue. While the internal data we use to judge the effectiveness of changes to our platform and to make improvements to how we make decisions about allocating Advertising Spend are based on what we believe to be reasonable assumptions and estimates, our internal tools are not independently verified by a third-party and have a number of limitations. We only have access to limited information about user behavior compared to many of our competitors that in many cases can record detailed information about users who log onto their websites or who complete a booking or other transaction with them.

In addition, our ability to track user behavior is also subject to considerable limitations, for example, relating to our ability to use cookies and browser extensions to analyze behavior over time, and to difficulties pertaining to users who use multiple devices to conduct their search for accommodation. In particular, users can block or delete cookies through their browsers or “ad-blocking” software or apps. The most common Internet browsers allow users to modify their browser settings to prevent cookies from being accepted by their browsers or are set to block third-party cookies by default. At least one major browser has introduced extensive privacy features, including the imposition of a strict time limit on tracking tools' lifespans. Another major browser provider has announced a phase-out of third-party cookies for all users by the end of the second half of 2024. Further, the mobile app ecosystem is constantly evolving, in particular with how the operating systems handle third party data tracking and usage. Changes in these technologies or developments further limiting data availability may inhibit our ability to use user and web analytics data to better understand and track our users’ preferences. We use this information to improve our platform, to optimize our marketing campaigns and our advertisers’ campaigns and to detect and prevent fraudulent activities, which all may be adversely affected. We believe that many of our competitors, in particular Google, have substantial advantages compared to us in their ability to understand and track users' behavior. In addition, we are to a significant extent dependent upon certain advertisers for specific types of user information, including, for example, as to whether a user ultimately completed a booking. Our or our advertisers’ methodologies for tracking this information may change over time. Some countries have already adopted digital services tax, or other taxes of a similar nature, while other countries may also adopt such taxes in the future. In addition to increasing our operational expenses, digital services tax or other taxes of a similar nature make it more difficult for us to measure the marginal efficiency of our Advertising Spend among marketing channels as such taxes affect not only how we allocate our spend but also how these marketing channels and our advertisers make

16

decisions about their businesses. Additionally, our use of such tracking tools may be subject to regulation by certain data protection laws.

Furthermore, we incorporate AI into certain of our offerings. The use of AI presents risks and challenges, including that algorithms may be flawed, datasets may be insufficient, erroneous, stale, or contain biased information, or content chosen for display to users by AI systems may be discriminatory, offensive, illegal, or otherwise harmful. These deficiencies and other failures of AI systems could subject us to competitive harm, regulatory action, legal liability, and brand or reputational harm. In addition, AI's sophistication in mimicking human behavior can also make it more difficult to detect fraudulent activities, such as click fraud and fake reviews, thereby potentially jeopardizing our reputation and relationships with advertisers. See also – “Any use of artificial intelligence/machine learning (AI/ML) technologies in our operations may present additional legal, regulatory, and social risks, which could lead to additional costs and impact our competitive position.”

If the internal tools we use to judge the effectiveness of changes to our platform produce or are based on information that is incomplete or inaccurate, or we do not have access to important information, or if we are not sufficiently rigorous in our analysis of that information, or if such information is the result of algorithm or other technical or methodological errors, the decisions we make relating to our website, marketplace and allocation of marketing spend may not result in the positive effects in terms of profitability, revenue and user experience that we expect, which may negatively impact our business, results of operations, financial condition and prospects.

In the past, we identified a material weakness in our internal control over financial reporting. If the measures we have implemented, including internal controls, fail to be effective in the future, any such failure could result in material misstatements of our financial statements, cause investors to lose confidence in our reported financial and other public information, harm our business and adversely impact the trading price of our ADSs.

Our management is responsible for establishing and maintaining internal controls over financial reporting, disclosure controls, and compliance with other requirements of the Sarbanes-Oxley Act and the rules promulgated by the SEC thereunder. Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements in accordance with U.S. GAAP. In addition, our independent registered public accounting firm is required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act. Satisfying these requirements requires us to dedicate a significant amount of time and resources, including for the development, implementation, evaluation and testing of our internal controls over financial reporting. Although no material weaknesses were identified in connection with the attestation of the effectiveness of our internal control over financial reporting as of December 31, 2023, 2022 or 2021, our management cannot guarantee that our internal controls and disclosure controls will prevent all possible errors or fraud. In addition, the internal controls that we have implemented could fail to be effective in the future. This failure could result in material misstatements in our financial statements, result in the loss of investor confidence in the reliability of our financial statements and subject us to regulatory scrutiny and sanctions. This could, in turn, harm our business and the market value of our ADSs. In addition, we may be required to incur costs in improving our internal controls system and the hiring of additional personnel.

We may experience difficulties in implementing new business and financial systems.