STROUDSBURG, PA / ACCESSWIRE / January 27, 2021 / ESSA Bancorp, Inc. (the "Company") (NASDAQ:ESSA), the holding company for ESSA Bank & Trust (the "Bank"), a $1.9 billion asset financial institution providing full service commercial and retail banking, financial, and investment services in eastern Pennsylvania, today announced financial results for the three months ended December 31, 2020.

Net income was $4.1 million, or $0.41 per diluted share, for the three months ended December 31, 2020, up 21% compared with $3.4 million, or $0.33 per diluted share, for the three months ended December 31, 2019.

Gary S. Olson, President and CEO, commented: "The Company's financial performance in the fiscal first quarter of 2021 reflected the ongoing commitment of ESSA to provide responsive service and personalized financial solutions with increased use of digital capabilities, ensure the health and safety of customers and employees, and maintain a strong balance sheet, asset quality and liquidity.

"Fiscal first quarter earnings results reflected the positive impact of reduced interest expense and increased noninterest income. We continued to maintain increased cash reserves to ensure liquidity and expanded loan loss reserves to address economic and pandemic-related uncertainties.

"Although economic uncertainty and pandemic-related conditions have understandably dampened commercial banking activity, we continued to see relative stability in commercial lending and only a modest year-over-year decline in interest income from loans. Managing interest expense contributed to higher year-over-year net interest income. Strong growth of noninterest income, fueled in part by brisk residential mortgage originations that generated fee income and resulting gains on the sale of mortgages, was an important factor in generating double-digit net income growth. The Company's financial performance continued to build shareholder value.

"Our bankers continued to efficiently serve customers through a variety of channels from digital delivery to safe personal interactions. We believe fiscal 2021 first quarter results affirmed our commitment to reimagining the future of banking that will incorporate increased digital capabilities, new ways of collaborating with customers, less reliance on physical facilities, and new ways to educate and communicate with customers.

"Although the pandemic continues to impact our served markets, we have been encouraged by the economic health and resilience demonstrated throughout the region. Most customers who requested loan payment deferrals in 2020 are now current, and there have been few requests for relief in recent months. Loans still in forbearance at December 31, 2020 included $28.1 million in commercial real estate, $108,000 in commercial, $3.2 million in mortgage and $160,000 in auto. In total, these loans represent 2.3% of our total outstanding loans at December 31, 2020 compared to 4.5% at September 30, 2020 and 12.4% at June 30, 2020.

"While businesses continue to take a conservative and cautious stance, they are generally holding their own. ESSA has provided the support and services to help clients, including our active participation in the Paycheck Protection Program ("PPP") last year. We assisted many existing and new customers, and we are participating in the current round of government-guaranteed financing.

"The pandemic and resulting economic uncertainty continue to present challenges. We believe ESSA has demonstrated the ability to effectively address the challenges. We remained focused on maintaining liquidity, an appropriate loan loss reserve, credit quality management, managing interest and noninterest expense, and delivering superior service."

FIRST QUARTER 2021 HIGHLIGHTS

- Net interest income after provision for loan losses increased to $12.0 million for the three months of fiscal 2021 compared to $11.5 million for the three months of fiscal 2020 as the Company more than offset lower year-over-year total interest income and increased loan loss provision with lower interest expense.

- Quarterly interest expense declined sharply year-over-year. The interest expense reduction primarily reflected balance sheet management and repricing of interest bearing liabilities to reflect the current low-interest environment. The Company's cost of funds declined to 0.55% in the fiscal first quarter of 2021 from 1.33% a year earlier.

- Noninterest income growth contributed to the Company's net income in the fiscal first quarter of 2021, rising 29% to $3.1 million compared with $2.4 million a year earlier. The year-over-year increase primarily reflected additional income from loan swap fees, gains on the sale of long-term residential mortgages to the secondary market of $818,000, and increased earnings from bank owned life insurance.

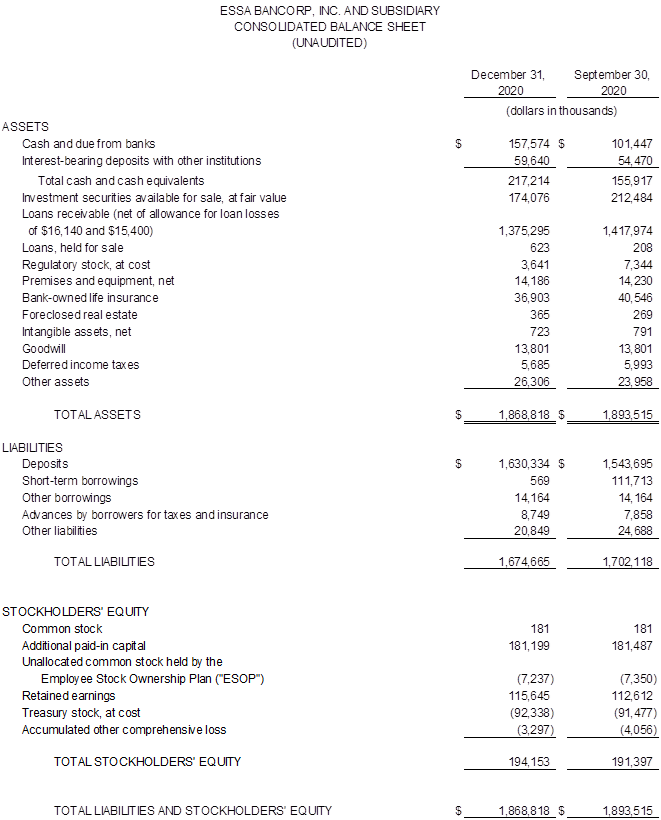

- Total assets were $1.87 billion at December 31, 2020 compared with $1.89 billion at September 30, 2020, primarily reflecting a slight decrease in net loans receivable and lower amounts of investment securities available for sale, offset in part, by increased cash.

- Focusing on maintaining strong liquidity, the Company held $217.2 million in cash and cash equivalents at December 31, 2020, a $61.3 million increase from September 30, 2020 as a result of balance sheet adjustments made to mitigate potential risks early in the pandemic along with continued deposit growth.

- Total net loans at December 31, 2020 were $1.38 billion compared with $1.42 billion at September 30, 2020, primarily reflecting sales of $18.7 million of residential mortgage loans and paydowns of Paycheck Protection Program (PPP) loans of $9.7 million and Indirect Auto Loans of $7.8 million during the quarter. Commercial real estate and construction loans declined by $8.1 million. Home equity loans and lines of credit remained stable.

- The Company maintained its focus on credit quality and increased its loan loss provision based on economic conditions. Nonperforming assets were 1.12% of total assets at December 31, 2020 compared to 1.09% of total assets at September 30, 2020.The allowance for loan losses was 1.16% of loans outstanding at December 31, 2020 compared to 1.07% at September 30, 2020.

- Core deposits (demand accounts, savings and money market) increased year-over-year, comprising 69% of total deposits at December 31, 2020 compared to 64% at December 31, 2019. The increase reflected increased commercial customer deposits, including PPP and stimulus funds not deployed, and demand retail deposits. Total deposits grew by $86.6 million from September 30, 2020 through December 31, 2020.

- The Bank continued to demonstrate financial strength with a Tier 1 leverage ratio of 9.28% at December 31, 2020, exceeding regulatory standards for a well-capitalized institution.

- Total stockholders' equity increased to $194.2 million at December 31, 2020 compared with $191.4 million at September 30, 2020.

- Tangible book value per share at December 31, 2020 increased to $16.60, compared with $16.26 at September 30, 2020.

- The Company paid a cash dividend of $0.11 per share on December 31, 2020, continuing its trend of quarterly cash dividends to shareholders.

- Broadening the size and scope of its Board of Directors, the Company in December, 2020 announced the appointment of Carolyn P. Stennett, Vice President, Human Resources at Victaulic Company, and Dr. Tina Q. Richardson, Chancellor of Penn State University's Lehigh Valley campus, to the Boards of Directors of ESSA Bancorp, Inc. and ESSA Bank & Trust.

Fiscal First Quarter 2021 Income Statement Review

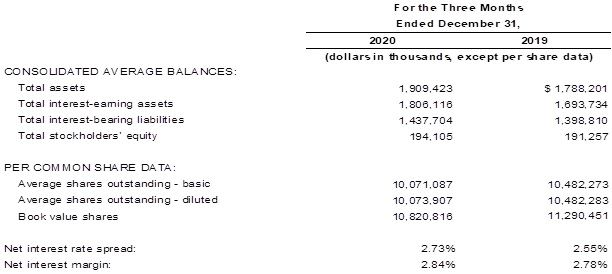

Total interest income was $14.9 million for the three months ended December 31, 2020 compared with $16.5 million for the three months ended December 31, 2019 reflecting a decline in interest rates and a decrease in the total yield on average interest earning assets from 3.88% for the quarter ended December 31, 2019 to 3.28% for the quarter ended December 31, 2020. The decline in rates was partially offset by growth of $112.4 million in average interest earning assets. The majority of the growth, however, was in the lower yielding cash category of interest earning assets.

Interest expense declined to $2.0 million for the quarter ended December 31, 2020 compared to $4.7 million for the same period in 2019. Cost of interest bearing liabilities declined from 1.33% for the 2019 period to 0.55% for the 2020 period, reflecting lower interest rates, timely repricing of deposits, roll-off of higher-cost borrowings and strong balance sheet management. Balance sheet management includes the effect of the deleverage transaction completed by the Company during the fourth quarter of 2020 that decreased the Company's borrowed funds by approximately $123.0 million. Average interest-bearing liabilities grew $38.9 million year-over-year.

For the three months ended December 31, 2020, net interest income was $12.9 million compared with $11.8 million for the three months ended December 31, 2019. The net interest margin for first three months of fiscal 2021 was 2.84% compared with 2.78% for the first three months of fiscal 2020 and 2.64% for the three months ended September 30, 2020. The net interest rate spread was 2.73% for the three months of fiscal 2021, 2.55% for the same three months of fiscal 2020 and 2.48% for the three months ended September 30, 2020.

Net interest income after provision for loan losses in the three months of fiscal 2021 reflected a higher provision for loan losses, primarily due to prudent reserving practices in light of economic conditions and uncertainties. The Company's provision for loan losses was $900,000 for the three months ended December 31, 2020, compared with $375,000 for the three months ended December 31, 2019.

Noninterest income increased 29% to $3.1 million for the three months ended December 31, 2020, compared with $2.4 million for the three months ended December 31, 2019. Noninterest income in the fiscal first quarter of 2021 included $818,000 in gains on sales of residential mortgages, primarily lower-interest 30-year fixed rate loans. The Company's strategy continues to focus on commercial banking and decreasing the amount of long-term, low interest, retained residential mortgages. Loan swap fees were $211,000 in fiscal first quarter 2021 compared to no similar fees in fiscal first quarter 2020. In addition, the Company recorded $120,000 in earnings on bank-owned life insurance during this fiscal first quarter due to the notice of death of a former executive included in the Company's bank-owned life insurance policies.

Noninterest expense was $10.2 million for the three months ended December 31, 2020 compared with $9.8 million for the comparable period a year earlier primarily reflecting increases in compensation and employee benefits expenses and Federal Deposit Insurance Corporation premiums.

Balance Sheet, Asset Quality and Capital Adequacy Review

Total assets decreased $24.7 million to $1.87 billion at December 31, 2020, from $1.89 billion at September 30, 2020, primarily due to declines in investment securities available for sale and loans receivable offset in part by increases in cash and cash equivalents.

Cash and cash equivalents increased $61.3 million during the first three months of fiscal 2021. At December 31, 2020, cash and cash equivalents were $217.2 million compared with $155.9 million at September 30, 2020.

Decreases in investment and loan balances outstanding, offset in part by a decrease in liabilities, account for the majority of the first quarter increase. The Company built the majority of its cash position in the fiscal second quarter of 2020 and has maintained that position through the first quarter of fiscal 2021 to remain prepared for ongoing economic uncertainties.

Total net loans were $1.38 billion at December 31, 2020 compared with $1.42 billion at September 30, 2020. Residential real estate loans were $601.5 million at December 31, 2020 compared to $610.4 million at September 30, 2020. The Company sold $18.7 million in residential mortgage loans to the Federal Home Loan Bank of Pittsburgh during the fiscal first quarter, recording gains on the sale of these loans in noninterest income. Indirect auto loans declined by $7.8 million during the first quarter of fiscal 2021 reflecting expected runoff of the portfolio following the Company's previously announced discontinuation of indirect auto lending in July 2018.

Commercial real estate loans were $508.0 million at December 31, 2020 compared with $509.6 million at September 30, 2020. Commercial loans were $123.4 million, compared with $71.3 million a year earlier, primarily reflecting the addition of PPP loans during fiscal 2020. Compared with commercial loan levels at September 30, 2020, commercial loans declined $16.2 million partially due to the repayment of $9.7 million in PPP loans carried in the commercial loan portfolio. Construction loans, spurred by continued residential and commercial construction activity, increased to $11.6 million at December 31, 2020 from $8.8 million a year earlier, and were essentially unchanged from fiscal year-end 2020.

Total deposits were $1.63 billion at December 31, 2020 up 6% compared with $1.54 billion at September 30, 2020. Core deposits (demand accounts, savings and money market) were $1.13 billion, or 69% of total deposits, at December 31, 2020. Noninterest bearing demand accounts were $256.2 million, up 6% from September 30, 2020, interest bearing demand accounts rose 15% to $314.5 million from September 30, 2020 levels, and money market accounts were $390.2 million, down $11.7 million or 2.9% from September 30, 2020. Total borrowings decreased $111.1 million to $14.7 million at December 31, 2020 from $125.9 million at September 30, 2020 as the Company shifted its wholesale funding to lower costing brokered deposits.

Nonperforming assets were $20.9 million, or 1.12% of total assets, at December 31, 2020, compared with $20.6 million, or 1.09% of total assets, at September 30, 2020 and $10.2 million, or 0.56% of total assets at December 31, 2019. Nonperforming assets include two nonperforming commercial real estate loans totaling $9.3 million. The Company notes these loans are well collateralized and carry personal guarantees.

For the three months ended December 31, 2020, the Company's return on average assets and return on average equity were 0.86% and 8.45%, compared with 0.76% and 7.09%, respectively, in the comparable period of fiscal 2020.

The Bank continued to demonstrate financial strength with a Tier 1 leverage ratio of 9.28% at December 31, 2020, exceeding regulatory standards for a well-capitalized institution.

Total stockholders' equity increased $2.8 million to $194.2 million at December 31, 2020, from $191.4 million at September 30, 2020, primarily reflecting net income growth and an increase in comprehensive income, offset in part by dividends paid to shareholders and an increase in treasury stock. Tangible book value per share at December 31, 2020 was $16.60 compared to $16.26 at September 30, 2020 and $15.64 at December 31, 2019.

About the Company: ESSA Bancorp, Inc. is the holding company for its wholly owned subsidiary, ESSA Bank & Trust, which was formed in 1916. Headquartered in Stroudsburg, Pennsylvania, the Company has total assets of $1.9 billion and has 22 community offices throughout the Greater Pocono, Lehigh Valley, Scranton/Wilkes-Barre, and suburban Philadelphia areas. ESSA Bank & Trust offers a full range of commercial and retail financial services, asset management and trust services, investment services through Ameriprise Financial Institutions Group and insurance benefit services through ESSA Advisory Services, LLC. ESSA Bancorp Inc. stock trades on the NASDAQ Global Market (SM) under the symbol "ESSA."

Forward-Looking Statements

Certain statements contained herein are "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements may be identified by reference to a future period or periods, or by the use of forward-looking terminology, such as "may," "will," "believe," "expect," "estimate," "anticipate," "continue," or similar terms or variations on those terms, or the negative of those terms. Forward-looking statements are subject to numerous risks and uncertainties, including, but not limited to, those related to the economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including compliance costs and capital requirements, changes in prevailing interest rates, acquisitions and the integration of acquired businesses, credit risk management, asset-liability management, the financial and securities markets and the availability of and costs associated with sources of liquidity, and the Risk Factors disclosed in our annual and quarterly reports. In addition, the COVID-19 pandemic continues to have an adverse impact on the Company, its customers and the communities it serves. The adverse effect of the COVID-19 pandemic on the Company, its customers and the communities where it operates will continue to adversely affect the Company's business, results of operations and financial condition for an indefinite period of time.

The Company wishes to caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. The Company wishes to advise readers that the factors listed above could affect the Company's financial performance and could cause the Company's actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake and specifically declines any obligation to publicly release the result of any revisions that may be made to any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

FINANCIAL TABLES FOLLOW

Contact: Gary S. Olson, President & CEO

Corporate Office: 200 Palmer Street, Stroudsburg, Pennsylvania 18360

Telephone: (570) 421-0531

SOURCE: ESSA Bancorp Inc.