Preliminary Results for the Year Ended 31 December 2024

April 11, 2025

Biodexa Pharmaceuticals PLC

("Biodexa" or the "Company" or, together with its subsidiaries, the "Group")

Preliminary Results for the Year Ended 31 December 2024

Biodexa Pharmaceuticals PLC (NASDAQ:BDRX), an acquisition-focused clinical stage biopharmaceutical company developing a pipeline of innovative products for the treatment of diseases with unmet medical needs, announces its audited preliminary results for the year ended 31 December 2024.

For more information, please contact:

Biodexa Pharmaceuticals PLC

Stephen Stamp, CEO, CFO

Tel: +44 (0)29 2048 0180

www.biodexapharma.com

About Biodexa

Biodexa Pharmaceuticals PLC (NASDAQ:BDRX) is a clinical stage biopharmaceutical company developing a pipeline of innovative products for the treatment of diseases with unmet medical needs. The Company's lead development programs include eRapa, under development for Familial Adenomatous Polyposis and Non-Muscle Invasive Bladder Cancer; tolimidone, under development for the treatment of type 1 diabetes; and MTX110, which is being studied in aggressive rare/orphan brain cancer indications.

eRapa is a proprietary oral formulation of rapamycin, also known as sirolimus. Rapamycin is an mTOR (mammalian Target Of Rapamycin) inhibitor. mTOR has been shown to have a significant role in the signalling pathway that regulates cellular metabolism, growth and proliferation and is activated during tumorgenesis.

Tolimidone is an orally delivered, potent and selective activator of Lyn kinase. Lyn is a member of the Src family of protein tyrosine kinases, which is mainly expressed in hematopoietic cells, in neural tissues, liver, and adipose tissue. Tolimidone demonstrates glycemic control via insulin sensitization in animal models of diabetes and has the potential to become a first in class blood glucose modulating agent.

MTX110 is a solubilised formulation of the histone deacetylase (HDAC) inhibitor, panobinostat. This proprietary formulation enables delivery of the product via convection-enhanced delivery (CED) at chemotherapeutic doses directly to the site of the tumor, by-passing the blood-brain barrier and potentially avoiding systemic toxicity.

Biodexa is supported by three proprietary drug delivery technologies focused on improving the bio-delivery and bio-distribution of medicines. Biodexa's headquarters and R&D facility is in Cardiff, UK. For more information visit www.biodexapharma.com.

Forward-Looking Statements

Certain statements in this announcement may constitute "forward-looking statements" within the meaning of legislation in the United Kingdom and/or United States. Such statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and are based on management's belief or interpretation. All statements contained in this announcement that do not relate to matters of historical fact should be considered forward-looking statements. In certain cases, forward-looking statements can be identified by the use of words such as "plans", "expects" or "does not anticipate", or "believes", or variations of such words and phrases or statements that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur" or "be achieved." Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.

Reference should be made to those documents that Biodexa shall file from time to time or announcements that may be made by Biodexa in accordance with the rules and regulations promulgated by the SEC, which contain and identify other important factors that could cause actual results to differ materially from those contained in any projections or forward-looking statements. These forward-looking statements speak only as of the date of this announcement. All subsequent written and oral forward-looking statements by or concerning Biodexa are expressly qualified in their entirety by the cautionary statements above. Except as may be required under relevant laws in the United States, Biodexa does not undertake any obligation to publicly update or revise any forward-looking statements because of new information, future events or events otherwise arising.

INTRODUCTION

Headquartered in Cardiff, UK, with its American Depositary Shares ("ADSs") quoted on the NASDAQ exchange in the US, Biodexa is a clinical-stage biotechnology company developing a pipeline of innovative products for the treatment of diseases with unmet medical needs including Familial Adenomatous Polyposis ("FAP"), Non-muscle Invasive Bladder Cancer ("NMIBC"), Type 1 Diabetes ("T1D") and rare/orphan brain cancers.

STRATEGY

The Company's transition from a drug delivery company to a therapeutics company is now complete with a pipeline of assets, all of which are at clinical stage and, we believe, offer significant potential to improve outcomes for patients.

Following the successful re-positioning of the Company in 2024, our priorities for 2025 reflect our new strategy as follows:

| Strategic Imperatives | Progress in 2024 | Priorities for 2025 |

| Advance our development assets through the clinic | We announced the following clinical milestones in 2024: February: results of a Phase 1 Investigator Initiated Trial at Columbia University of MTX110 in patients with Diffuse Midline Glioma ("DMG") May: Six month results of a Phase 2 study of eRapa in FAP presented at Digestive Disease Week June: 12 month results of a Phase 2 study of eRapa in FAP presented at InSIGHT 2024 October: an update of Cohort A of a Phase 1 study of MTX110 in patients with recurrent glioblastoma ("rGBM") | Initiate recruitment of a registrational Phase 3 study of eRapa in patients with FAP in the US and Europe Secure Orphan Drug Designation for eRapa in FAP in Europe Engage with FAP patient support groups in the US and Europe Initiate recruitment of a Phase 2a Investigator Initiated Trial dose confirmation study of tolimidone in T1D patients |

| Develop and broaden our drug development pipeline | We in-licensed eRapa, a proprietary formulation of rapamycin being developed for FAP and NMIBC. The six month and 12 month data from the Phase 2 study in FAP were presented at two prestigious scientific meetings during the year while the Phase 2 study in NMIBC remains ongoing We have initiated a series of preclinical experiments designed to identify potential indications for tolimidone in addition to T1D | Consolidate data in vitro and in vivo data to support additional potential, ideally orphan, indications for tolimidone Seek additional pre-IND and/or clinical-stage assets to acquire or in-license Expand further our patent portfolio to cover new inventions and divisionals to strengthen existing patent families |

| Secure long term, ideally non-dilutive financing for the Company | The in-licensing of eRapa included access to a $17 million grant from the Cancer Prevention and Research Institute of Texas ("CPRIT") with a 2 for 1 Company match In addition, we raised a total of $11.1 million from financings in May and July 2024 | Secure licensees and/or co-development partners for eRapa in Europe and Japan Investigate other potential sources of long-term capital to support the Company's development programmes |

BUSINESS MODEL

Having successfully transitioned to a therapeutics company and broadened our internal pipeline, our business model is to add value to our development programmes by advancing them through the clinic before seeking partners to complete late-stage studies and commercialise the products.

Development

Our intention is to build a balanced portfolio of clinical-stage development assets, ideally with a focus on rare/orphan indications. eRapa was in-licensed in April 2024 as Phase 3 ready in FAP with an ongoing Phase 2 study in NMIBC. Tolimidone, which was in-licensed in December 2023, is a Phase 2 ready asset being developed initially for T1D. MTX110 is currently in Phase I development for three rare/orphan brain cancers.

Manufacturing

We do not intend to establish our own manufacturing capabilities. For clinical trial material we utilise GMP-certified contract manufacturers.

Commercialisation

Once proof-of-concept has been established, we intend to out-license our products to a partner who would complete the clinical development and subsequently market and sell them in the licensed territory. In addition to reimbursement of development costs, the partner would be expected to make milestone payments based on sales targets and royalty payments.

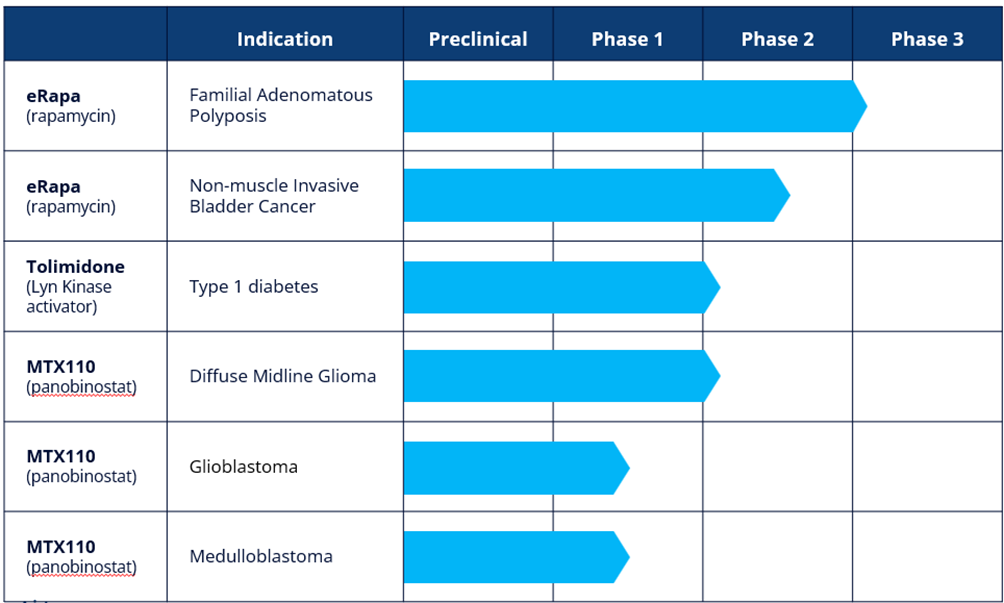

Our development pipeline now includes five projects, all which are at clinical stage, as follows:

CLINICAL-STAGE ASSETS

eRapa

eRapa is a proprietary oral tablet formulation of rapamycin, also known as sirolimus. Rapamycin is an mTOR (mammalian Target Of Rapamycin) inhibitor. mTOR has been shown to have a significant role in the signalling pathway that regulates cellular metabolism, growth and proliferation and is activated during tumorgenesis1. Rapamycin is approved in the US for organ rejection in renal transplantation as Rapamune® (Pfizer). Through the use of nanotechnology and pH sensitive polymers, eRapa is designed to address the poor bioavailability, variable pharmacokinetics and toxicity generally associated with the currently available forms of rapamycin.

Familial Adenomatous Polyposis (FAP)

FAP is characterized as a proliferation of polyps in the colon and/or rectum, usually occurring in mid-teens. There is no approved therapeutic option for treating FAP patients, for whom active surveillance and surgical resection of the colon and/or rectum remain the standard of care. If untreated, FAP typically leads to cancer of the colon and/or rectum. There is a significant hereditary component to FAP with a reported incidence of one in 5,000 to 10,000 in the US and one in 11,300 to 37,600 in Europe. eRapa has received Orphan Designation in the US and we are in the process of seeking such designation in Europe. Importantly, mTOR has been shown to be over-expressed in FAP polyps – thereby underscoring the rationale for using a potent and safe mTOR inhibitor like eRapa to treat FAP. ERapa received FDA Fast Track designation in February 2025.

The results of the Phase 2 study were presented at two leading scientific conferences in the second quarter of 2024. Following a positive end of Phase 2 meeting with the FDA, we have requested a Type C meeting with the FDA to finalize the protocol for a Phase 3 multi-centre, double-blind, placebo-controlled study in FAP. The Phase 3 study, which is expected to be registrational, plans to recruit approximately 168 patients across thirty or more sites, with a primary endpoint being time to a defined progression free survival event. The study is expected to recruit over 18 months and is supported by a non-dilutive grant of $17.0 million from CPRIT.

Non-muscle Invasive Bladder Cancer (NMIBC)

NMIBC refers to tumors found in the tissue that lines the inner surface of the bladder. The most common treatment is transurethral resection of the bladder tumour followed by intravesical Bacillus Calmette-Guerin ("BCG") with chemotherapy depending upon assessment of risk of recurrence. NMIBC is the fourth most common cancer in men with an incidence of 10.1 per 100,000 and 2.5 per 100,000 in women. Our ongoing multi-centre, double-blind, placebo-controlled Phase 2 study in NMIBC is expected to enrol up to 166 patients with primary endpoints of safety/tolerability and relapse free survival after 12 months of treatment. The Phase 2 study, which is supported by a $3.0 million non-dilutive grant from the National Cancer Institute, part of the National Institutes of Health, is expected to read out in the first half of 2025.

Tolimidone

Tolimidone was originally discovered by Pfizer Inc. ("Pfizer") and was developed through Phase 2 for the treatment of gastric ulcers. Pfizer undertook a broad pre-clinical programme to characterise the pharmacology, pharmacokinetics, metabolism and toxicology of tolimidone. Pfizer discontinued development of the drug due to lack of efficacy for that indication in Phase 2. Tolimidone is a selective activator of the enzyme Lyn kinase which increases phosphorylation of insulin substrate -1, thereby amplifying the signalling cascade initiated by the binding of insulin to its receptor.

Type 1 Diabetes (T1D)

We intend to develop tolimidone for the treatment of T1D. As a Lyn kinase activator, tolimidone has been shown in preclinical experiments to have a role in beta cell survival and proliferation. If replicated in clinical studies, tolimidone could have the potential to be disease modifying and change the treatment paradigm for T1D. T1D affects approximately 8.4 million people worldwide and there are approximately 500,000 new diagnoses per annum.

As a first step in the planned continued clinical development of tolimidone, we intend to initiate a Phase 2a dose confirmation study to establish the optimum dose of tolimidone in patients with T1D. The Phase 2a study will be open-label in approximately 15 patients with T1D treated over a period of three months with endpoints of change in C-peptide levels, HbA1c and number of hyperglycaemic events.

MTX110

Using our MidaSolve technology in combination with panobinostat, an otherwise insoluble drug, MTX110 is designed for direct-to-tumour administration via a catheter system (Convection Enhanced Delivery, or "CED") thereby bypassing the blood-brain barrier and allowing for high drug concentrations and broader drug distribution in and around the tumour while simultaneously minimising systemic toxicity and other side effects. Panobinostat is currently marketed under the brand Farydak® which is used orally in combination therapy for the treatment of multiple myeloma. We are currently researching the utility of MTX110 to proof-of-concept stage in three indications:

Glioblastoma Multiforme (GBM)

GBM is the most common and aggressive form of brain cancer in adults, usually occurring in the white matter of the cerebrum. Treatments include radiation, surgical resection and chemotherapy although, in almost all cases, tumours recur. There are approximately 2-3/100,000(1) population diagnoses of GBM per annum. Survival with standard of care treatment ranges from approximately 13 months in unmethylated MGMT patients to approximately 30 months in highly methylated MGMT patients(2). Once it has recurred, median survival is 6.5 months(3).

During 2023 we completed recruitment of patients in the first cohort of a Phase I study to assess the utility of MTX110 in recurrent GBM. The Phase I study is an open-label, dose escalation study designed to assess the feasibility and safety of intermittent infusions of MTX110 administered by convection enhanced delivery ("CED") via implanted refillable pump and catheter. The study aims to recruit two cohorts, each with a minimum of four patients; the first cohort received MTX110 only and the second cohort will also receive MTX110 but, at the option of the treating clinician, the catheter may be re-positioned once recurrence occurs.

Diffuse Midline Glioma (DMG)

DMG tumours are located in the pons (middle) of the brain stem and are diffusely infiltrating. Occurring mostly in children, approximately 1,000 patients(4) worldwide are diagnosed with DIPG per annum and median survival is approximately 10 months(5). There is no effective treatment since surgical resection is not possible. The standard of care is radiotherapy, which transiently improves symptoms and survival. Chemotherapy does not improve survival and one likely reason is that many anti-cancer drugs cannot cross the blood-brain barrier to access the tumour.

In October 2020, we reported the first-in-human study by the University of California, San Francisco ("UCSF") of MTX110 in DMG using a CED system. The Phase I study established a recommended dose range for Phase II, a good safety and tolerability profile but also encouraging median survival data of 26 months in the seven patients treated.

An additional Phase I Investigator Initiated Trial by Columbia University reported topline data in February 2024. Thereafter, we intend to explore the possibility of seeking an IND for a Phase II study of MTX110 in DMG.

Medulloblastoma

Medulloblastomas are malignant embryonal tumours that start in the cerebellum. They are invasive and, unlike most brain tumours, spread through the cerebrospinal fluid ("CSF") and frequently metastasise to different locations in the brain and spinal cord. Treatments include resection, radiation and chemotherapy. Approximately 350 patients(6) are diagnosed with medulloblastoma per annum and 3,800 people are living with the disease in the US. The cumulative survival rate is approximately 60%, 52%, and 47% at 5 years, 10 years and 20 years, respectively(7); however, recurrence is nearly always fatal with no established standard of care.

The University of Texas is undertaking a Phase I exploratory study in recurrent medulloblastoma patients using direct administration of MTX110 into the fourth ventricle, enabling it to circulate throughout the central spinal fluid.

(1) American Association of Neurosurgeons.

(2) Radke et al (2019). Predictive MGMT status in a homogeneous cohort of IDH wildtype glioblastoma patients. Acta Neuropathologica Communications 7:89 Online: https://doi.org/10.1186/s40478-019-0745-z.

(3) J Neurooncol. 2017; 135(1): 183–192.

(4) Louis DN, Ellison DW, et al. The 2016 World Health Organization Classification of Tumors of the Central Nervous System: a summary. Acta Neuropathol 2016; 131:803–820.

(5) Jansen et al, 2015. Neuro-Oncology 17(1):160-166.

(6) Aboian et al (2018). Neuro-Oncology Practice, Volume 5, Issue 4, December 2018.

(7) Smoll NR (March 2012). ‘Relative survival of childhood and adult medulloblastomas and primitive neuroectodermal tumors (PNETs)'. Cancer. 118 (5): 1313–22.

(8) https://my.clevelandclinic.org/health/diseases/22737-leptomeningeal-disease.

CHIEF EXECUTIVE'S REVIEW

Introduction

During 2024, we took significant steps to diversify and advance our development pipeline by adding late-phase eRapa to tolimidone and MTX110 R&D programmes. The addition of eRapa is expected to enhance the Company's news flow and provide catalysts for financing as the two indications advance through the clinic.

R&D update

eRapa

In April 2024 we licensed eRapa, a proprietary formulation of rapamycin, from Rapamycin Holdings, Inc. d/b/a Emtora Biosciences, Inc. ("Emtora"). Rapamycin is an mTOR inhibitor. As a central regulator of cell metabolism, growth, proliferation and survival, the mTOR pathway is activated during various cellular processes including tumour formation and angiogenesis. Through the use of nanotechnology and pH sensitive polymers, eRapa is designed to address the poor bioavailability, variable pharmacokinetics and toxicity generally associated with the currently available forms of rapamycin.

On May 21, 2024, we announced six month results of the Phase 2 clinical trial of eRapa in FAP (NCT04230499) which were presented at the 2024 Digestive Disease Week annual meeting in Washington D.C. In the duodenum, 14/18 (78%) patients were non-progressors with 11/18 (61%) of these patients with PR. In the colorectum, 25/29 (86%) patients were non progressors including all with an intact colon; of these 15/29 (67%) patients demonstrated PR including 4 with an intact colon (see Figure 1 below). Only two drug-related Grade 3 Serious Adverse Events occurred during the trial (with no Grade 4 or 5 reported), and 97% of patients remained on treatment at six months. In summary, after six months' treatment, eRapa appeared safe and well-tolerated with a significant 24% reduction in the total polyp burden at six months compared with baseline (p=0.04) and an overall 83% non-progression rate.

On June 24, 2024, we announced 12 month results of the Phase 2 clinical trial which were presented at the 2024 InSIGHT bi-annual meeting in Barcelona. Overall, 21 of 28 (75%) patients were deemed to be non-progressors at 12 months with a median reduction in polyp burden of 17%. Over the course of 12 months, there were four related Grade 3 or higher and one related Serious Adverse Event reported during the trial and 95% compliance rate at 12 months. One patient was removed from the trial due to non-compliance. In summary, after 12 months' treatment, eRapa appeared safe and well-tolerated with a median 17% reduction in the total polyp burden at 12 months compared with baseline and an overall 75% non-progression rate. The 89% non-progression rate and 29% median reduction in polyp burden observed in Cohort 2 will be the dosage regimen for Phase 3.

The open-label Phase 2 study was conducted in seven U.S. centres of excellence in 30 adult patients with median age of 43 years with intact colon (n=6) or post-colectomy and ileo-rectal anastomosis and at least 10 adenomas in the rectal remanent (n=24). Patients were sequentially enrolled into three dosing cohorts of 10 patients each for a 12-month treatment period: 0.5mg every other day (Cohort 1), 0.5mg daily every other week (Cohort 2), and 0.5mg daily (Cohort 3). Upper and lower endoscopic surveillance occurred at baseline and after six months. Primary endpoints were the safety and tolerability of eRapa and percentage change from baseline in polyp burden, as measured by the aggregate of all polyp diameters. In February 2025, we announced that the FDA had granted Fast Track designation to eRapa in FAP.

An ongoing Phase 2 study of eRapa in NMIBC is scheduled to report results in mid-2025.

Tolimidone

In December 2023, we secured the global rights to develop and commercialise tolimidone. The Phase II ready product is supported by very substantial preclinical data, has been exposed to more than 700 patients and has demonstrated compelling preclinical data to support our chosen indication of T1D.

In T1D, the body's immune system attacks pancreatic beta cells such that they can no longer produce insulin which is required to regulate plasma glucose levels. The causes of T1D are not fully understood and there is currently no cure. Patients with T1D are dependent on daily administration of insulin (via injection or infusion).

Tolimidone is a Lyn kinase activator and its potential utility in T1D was first demonstrated by several ground-breaking preclinical studies conducted at the University of Alberta, where Lyn kinase was identified as a key factor for beta cell survival and proliferation in vitro and in vivo models. Tolimidone was shown to both prevent beta cell degradation and to stimulate beta cell proliferation.

The Phase 2a study will be open-label and include three doses with approximately 15 patients studied over three months with a follow up period. End points are expected to include C-peptide levels (a marker for insulin), HbA1c levels (a marker for plasma glucose) and a number of severe hyperglycaemic events. Thereafter, we expect to follow up by a double-blind, placebo-controlled Phase IIb study in approximately 40-45 patients with similar clinical endpoints.

MTX110

In October 2023, we announced completion of recruitment of Cohort A of our ongoing open-label Phase I dose-escalation study, which is designed to assess the feasibility and safety of intermittent infusions of MTX110 administered by CED via implanted refillable pump and catheter. Because no drug-related adverse events were observed within the first 30 days from the start of treatment, the minimum number of four patients were recruited into Cohort A. Patient #1 received weekly infusions of 60µM of MTX110 and Patients # 2, 3 and 4 each received 90µM, the expected optimum dose. The study site reported 12 months of survival from the start of the treatment in the 1st patient (OS=12 months).

We initially began developing MTX110 for DMG, the ultra-rare, highly aggressive and inoperable form of childhood brain cancer. In February 2024 we announced the results of a Phase I study conducted by Columbia University Irving Medical Center. As this was the first ever study of repeated infusions to the pons via an implanted CED catheter, the primary objective of the study was safety and tolerability and, accordingly, the number of infusions was limited to two, each of 48 hours, 7 days apart. Nine patients were treated in the study (30 µM group, n=3; 60 µM group, n=4; 90 µM group (optimal dose), n=2). One patient in the 60 µM group suffered a severe adverse event assessed by the investigators as not related to the study drug but related to the infusion and tumour anatomy. Although the study was not powered to reliably demonstrate efficacy, median overall survival ("OS") of patients in the study was 16.5 months.

In October 2023, we announced completed recruitment of four patients into cohort A of its Phase 1 study of MTX110 (also known as MAGIC-G1 study) (NCT 05324501) in patients with rGBM. MAGIC-G1 is an open-label, dose escalation study designed to assess the feasibility and safety of intermittent infusions of MTX110 administered by convection enhanced delivery (CED) via implanted refillable pump and catheter. Patients received MTX110 via intermittent repeated CED infusions. The status of patients in Cohort A was as follows: Patients #1 and #2 had deceased with overall survival (OS) since start of treatment of 12 months and 13 months, respectively. Patients #3 and #4 remained in post-study follow-up. Patient #3 had progression free survival (PFS) of six months and OS at that time of 13 months since start of treatment. Patient #4 has not yet had confirmed progression and had PFS and OS of 12 months since start of treatment.

We are also evaluating the utility of MTX110 in medulloblastoma in a pilot study at the University of Texas.

Financings

Warrant Inducement

In May 2024, we entered into agreements with certain investors that were holders of 1,572,674 of our outstanding Series E Warrants exercisable for $2.20 per Depositary Share and an aggregate of 2,463,477 of our Series F Warrants exercisable for $2.20 per Depositary Share, or Series F Warrants. The holders agreed to exercise the Series E Warrants and Series F Warrants, as applicable, at a reduced exercise price of $1.50 per Depositary Share. Upon closing of the transaction we issued 3,104,566 Depositary Shares to the Holders, with the remaining 931,585 Depositary Shares remaining unissued but held in abeyance until we receive notice from the holders that the remaining shares may be issued in compliance with the beneficial ownership limitation. In consideration for the immediate exercise of the Series E Warrants and/or Series F Warrants for cash, we issued one replacement Series G Warrant for each Series E Warrant exercised, and one replacement Series H Warrant for each Series F Warrant exercised. The Series G and Series H Warrants were exercisable immediately and expire after five years and one year, respectively. We received gross proceeds of approximately $6.05 million from the warrant exercise, prior to deducting the warrant inducement agent fees and other expenses.

Registered Direct Offering and Concurrent Private Placement

In July 2024, we closed a Registered Direct Offering and Private Placement with certain institutional investors for the sale of (i) an aggregate of 5,050,808 Depositary Shares, and (ii) an aggregate of 278,975 pre-funded warrants exercisable for Depositary Shares at a price per Depositary Share of $0.94, and a price per Pre-Funded Warrant of $0.9399. The Pre-Funded Warrants were exercisable immediately. In addition, in a concurrent Private Placement, we issued and sold to the Investors (i) Series J Warrants exercisable for 5,329,783 Depositary Shares, and (ii) Series K Warrants, exercisable for 5,329,783 Depositary Shares. The Series J and Series K Warrants are exercisable immediately and expire after one year and five years respectively and are all exercisable at an exercise price of $25.00 per Depositary Share. We received aggregate gross proceeds of $5.0 million before deducting the placement agent's fees and related offering expenses.

Promissory Note

In December 2024 we issued an unsecured promissory note to C/M Capital Master Fund LP in the principal amount of $600,000 at a 10% original issue discount. The Note is an unsecured obligation of the Company and bears interest at an annual rate of 5% and has a maturity date of one year. The Note includes a monthly repayment schedule, with the entire principal amount of the Note, plus interest, being repaid by December 2025. We received the $540,000 pursuant to the Note in December 2024.

Outlook

We expect two major clinical milestones in 2025; the initiation of our Phase 3 registrational study of eRapa in FAP and, the initiation of an IIT of tolimidone in T1D at the University of Alberta.

As has been the case for the past three years, financing for small- and micro-cap biotech companies remains challenging. The $35 million Equity Line of Credit ("ELOC") we put in place in February 2025 provides a welcome backstop source of capital as we seek non-dilutive sources of capital from out-licensing territorial rights to our development assets and/or additional grant funding.

FINANCIAL REVIEW

Introduction

Biodexa Pharmaceuticals PLC was incorporated as a company on 12 September 2014 and is domiciled in England and Wales.

Financial analysis

Key performance indicators

| 2024 | 2023 | Change | ||

| Total gross revenue(1) | £Nil | £0.38m | n/m | |

| R&D expenditure | £5.44m | £4.07m | 34% | |

| R&D as % of operating costs | 59% | 48% | n/a | |

| Net cash (outflow)/inflow for the year | (£4.30m) | £3.14m | n/m | |

| ============ | ============ | ============ | ||

| (1) | Total gross revenue represents collaboration income. | |||

Revenue

In the year ended 31 December 2024, Biodexa did not generate any gross revenue (2023: £0.38 million). Customer revenue in 2023 was derived entirely from the Group's R&D collaboration agreements with Janssen which ceased in September 2023.

Research and development expenditure

Research and development costs were £5.44 million, an increase of £1.37 million, or 34% on 2023 (2023: £4.07 million). The percentage of R&D costs as a percentage of operating costs also increased to 59% from 48% in the prior year. The increase in the year reflects the Directors decisions to acquire licenses for clinical stage assets, tolimidone in December 2023 and eRapa in April 2024, resulting in clinical expenditure of £1.09 million and £1.91 million respectively, this is offset by reduced spend of £1.10 million on the MAGIC-G1 study in rGBM. As a result of the re-focus on clinical stage assets there was a reduction in pre-clinical expense of £0.31 million. Personnel costs also reduced by £0.25 million in the year.

Administrative costs

Administrative costs in the year reduced by £0.55 million to £3.79 million (2023: £4.34 million), a decrease of 13%. The decrease in administrative costs in the year is driven by a positive reversal in foreign exchange of £0.26 million, a reduction in professional fees of £0.55 million offset by an increase in share-based payments of £0.22 million.

In 2024 the Company expensed £0.88 million on legal and professional fees in connection with the successful financing transactions in the year, the acquisition of the eRapa licence in April 2024 and aborted acquisitions, this compares to £1.31m spent in 2023 on similar transactions.

Staff costs

During the year, the average number of staff decreased to 13 (2023: 21), reflecting the cost reduction program undertaken in March 2023. Total staff cost increased 4% to £2.15 million (2023: £2.06 million), driven by the increase in share-based payment charge of £0.22 million.

Taxation

During 2024 and 2023 we recognised U.K research and development tax credits of £0.25 million and £0.41million in respect of R&D expenditure incurred.

Capital expenditure

Purchase of tangible fixed assets in 2024 was £0.01 million (2023: £0.03 million) and related to investment in laboratory equipment. In addition, in April 2024, the Company purchased an intangible asset being the global rights to develop and commercialise eRapa for total consideration of £2.71 million, this was satisfied £0.77 million in cash, £0.22 million by the issue of ordinary shares and deferred consideration of £1.72 million yet to be paid.

Cash flow

Net cash outflow from operating activities in 2024 was £12.26 million (2023: outflow £6.83 million) driven by a net loss of £5.73 million (2023: loss £7.08 million) and after negative movements in working capital of £3.74 million (2023: negative £0.05 million), taxes received of £0.13 million (2023: £0.84 million), and other net negative adjustments for non-cash items totalling £2.93 million (2023: negative £0.54 million).

Investing activities outflow in 2024 of £0.60 million (2023: outflow of £0.27 million) included purchases of property, plant and equipment of £0.01 million (2023: £0.03 million), purchase of eRapa licence for total consideration of £2.71 million including cash of £0.77 million. These cash outflows are offset by interest income from bank deposits of £0.18 million (2023: £0.07 million).

Financing activities inflow in 2024 of £8.56 million (2023: inflow of £10.23 million) was driven by receipts from share issues of £8.31 million (2023: £10.43 million) and receipt from issuance of promissory note £0.43 million (2023: £Nil). The other principal outflows related payments on lease liabilities of £0.19 million (2023: £0.19 million and interest paid of £Nil (2023: £0.01million).

As a result of the foregoing, net cash outflow for the year was £4.30 million (2023: inflow of £3.14 million).

Regained Compliance with NASDAQ

In August 2024, we received a letter from the Listing Qualifications Department of The Nasdaq Stock Market LLC notifying us that NASDAQ had determined to delist our securities from the NASDAQ Capital Market because our securities had a closing bid price below $1.00 for 30 consecutive business days, We requested a hearing, which automatically stayed any suspension or delisting action pending the hearing. The hearing took place on 8 October 2024 and on 7 November 2024, we were notified that the Hearings Panel had determined that we had regained compliance with the Minimum Bid Price Requirement.

Change in ADS Ratio and Nominal Value of Ordinary Shares

On 4 October 2024 the Company effected a change in the ratio of the Company's Ordinary Shares from each ADS representing 400 Ordinary Shares to each ADS representing 10,000 Ordinary Shares.

At a General Meeting on 22 November 2024, shareholders approved the subdivision and redesignation of the Company's Issued Ordinary Shares of £0.001 each into to one Ordinary Share of £0.00005 each and 19 ‘C' Deferred Shares of £0.00005 each. The ‘C' Deferred Shares have limited rights and are effectively valueless.

January 2025 Committed Equity Financing – Equity Line of Credit ("ELOC")

On 17 January, 2025, we entered into an ELOC with C/M Capital Master Fund LP ("C/M") pursuant to which we have the right, but not the obligation, to sell to C/M, and C/M is obligated to purchase, up to $35.0 million of newly issued ADSs for a period of 36 months from Commencement Date. As consideration for the Seller Shareholder's execution and delivery of the Purchase Agreement, we have agreed to pay to the Selling Shareholder a Commitment Fee of $875,000 in cash or in ADSs.

At any time after the Commencement Date, we may direct C/M to purchase a specified number of ADSs, or a Fixed Purchase, not to exceed $200,000, at a purchase price equal to the lesser of 95% of (i) the daily volume weighted average price, or VWAP, of the Depositary Shares for the five trading days immediately preceding the applicable Purchase Date for such Fixed Purchase and (ii) the lowest sale price of an ADS Share on the trading day immediately preceding the Purchase Date.

In addition, we may also direct C/M to purchase an additional number of ADSs in an amount up to the VWAP Purchase Maximum Amount (as defined in the Purchase Agreement), or a VWAP Purchase, at a purchase price equal to the lesser of 95% of (i) the closing price of an ADS on the trading day immediately preceding the applicable VWAP Purchase Date and (ii) the VWAP during the period on the applicable VWAP Purchase Date beginning at the opening of trading and ending at the VWAP Purchase Termination Time (as defined in the Purchase Agreement).

Lastly, we may also direct C/M to purchase an Additional VWAP Purchase at a purchase price equal to the lesser of 95% of (i) the closing price of an ADS on the trading day immediately preceding the applicable Additional VWAP Purchase Date and (ii) the VWAP during the Additional VWAP Purchase Period (as defined in the Purchase Agreement) on the applicable Additional VWAP Purchase Date.

Under the Purchase Agreement, the aggregate amount of Purchase Shares submitted in any single or combination of VWAP Purchase notices and/or Additional VWAP Purchase notices on a particular date require a payment from C/M to us not exceeding $2.5 million.

C/M is not obligated to purchase any ADSs pursuant to the Purchase Agreement if, when aggregated with all other securities then beneficially owned by C/M would result in C/M beneficially owning Ordinary Shares (represented by Depositary Shares) in excess of 9.99% of the then-outstanding Ordinary Shares.

The net proceeds under the Purchase Agreement to us will depend on the frequency and prices at which we sell Depositary Shares to the Selling Shareholder. We expect that any proceeds received by us from such sales to the Selling Shareholder will be used to fund our development programs, for working capital and other general corporate purposes.

Going Concern – material uncertainty

The Group and Company has experienced net losses and significant cash outflows from cash used in operating activities over the past years as it develops its portfolio. For the year ended 31 December 2024, the Group incurred a consolidated loss for the year of £5.73 million and negative cash flows from operations of £12.26 million. As of 31 December, 2024, the Group had an accumulated deficit of £150.42 million.

The Group's future viability is dependent on its ability to raise cash from financing activities to finance its development plans until milestones and/or royalties can be secured from partnering the Company's assets. The Group's failure to raise capital as and when needed could have a negative impact on its financial condition and ability to pursue its business strategies.

The Directors believe there are adequate options and time available to secure additional financing for the Company and after considering the uncertainties, the Directors consider it is appropriate to continue to adopt the going concern basis in preparing these financial statements. The Group's consolidated financial statements have therefore been presented on a going concern basis, which contemplates the realisation of assets and the satisfaction of liabilities in the normal course of business.

As at 31 December 2024, the Group had cash and cash equivalents of £1.67 million. The Directors have prepared cash flow forecasts and considered the cash flow requirement for the Group for the next three years including the period 12 months from the date of approval of the consolidated financial statements. These forecasts show that further financing will be required before Q4 2025 assuming, inter alia, that certain development programs and other operating activities continue as currently planned. Pursuant to its $35 million Equity Line of Credit, or ELOC, as described above, the Company may direct C/M to purchase ADSs (subject to certain limitations) and receive proceeds in accordance with a formula price for up to 36 months from the Commencement Date. There is no guarantee that the Company will be able to use the ELOC to the extent necessary to finance the Company's operations.

In the Directors' opinion, the environment for financing of small and micro-cap biotech companies remains challenging. While this may present acquisition and/or merger opportunities with other companies with limited or no access to financing, as noted above, any attendant financings by Biodexa are likely to be dilutive. The Directors continue to evaluate financing options, including those connected to acquisitions and/or mergers, potentially available to the Group. Any alternatives considered are contingent upon the agreement of counterparties and accordingly, there can be no assurance that any alternative courses of action to finance the Company would be successful.

This requirement for additional financing in the short term represents a material uncertainty that may cast significant doubt upon the Group and Parent Company's ability to continue as a going concern. Should it become evident in the future that there are no realistic financing options available to the Company which are actionable before its cash resources run out then the Company will no longer be a going concern. In such circumstances, we would no longer be able to prepare financial statements under paragraph 25 of IAS 1. Instead, the financial statements would be prepared on a liquidation basis and assets would be stated at net realizable value and all liabilities would be accelerated to current liabilities.

Macro-economic environment

The invasion by the Russian Federation military in Ukraine in early 2022 and the ongoing Israeli/Palestinian conflict in the Middle East has had a destabilising impact on the global economy. Although there has been no immediate impact on the Group, it is not possible to assess the medium- and long-term impact of these conflicts on the Group and the global economy generally.

In addition, U.S. President Trump has increased, and has indicated his willingness to continue to increase, the use of tariffs by the U.S. to accomplish certain U.S. policy goals. Such tariffs and any countermeasures could increase the cost of raw materials and components necessary for our operations, disrupt our supply chain and create additional operational challenges. Further, it is possible that government policy changes and related uncertainty about policy changes could increase market volatility. Because of these dynamics, we cannot predict the impact of any future changes to the U.S.'s or other countries' trading relationships or the impact of new laws or regulations adopted by the U.S. or other countries on our business. Such changes in tariffs and trade regulations could have a material adverse effect on our financial condition, results of operations and cash flows.

Environmental matters, community, human rights issues and employees

As at 31 December 2024 the Group had 11 employees, of whom 5 were routinely based at its offices in Cardiff, Accordingly the Company believes it has a relatively modest environmental impact. All materials imported into the Company's laboratories are assessed for safety purposes and appropriate handling and storage safeguards imposed as necessary. Any small quantities of hazardous materials are removed by licensed waste management contractors. A number of policies and procedures governing expectations of ethical standards and the treatment of employees and other stakeholders are set out in the Company's Employee Handbook. The Company has also established an anti-slavery policy pursuant to the Modern Slavery Act 2015.

The Company strives to be an equal opportunity employer, irrespective of race or gender. At 31 December 2024, the number of male/female employees was 27%/73%, the number of male/female senior managers was 60%/40% and the number of male/female Directors was 80%/20%.

Annual greenhouse gas emissions

We measure our environmental performance by reporting our carbon footprint in terms of tonne CO2 equivalent. We report separately on our indirect emissions from consumption of electricity (Scope 2) and emissions consisting of employee travel in cars on Group business estimated on the basis of miles travelled (Scope 3). The Group have elected to monitor and report its energy efficiency using tonnes of CO2 per employee as an intensity ratio.

Methodology

In calculating the reported energy usage and equivalent greenhouse gas emissions the Group have referred to the HM Government Environment Reporting Guidelines and the GHG Reporting Protocol. A location-based allocation methodology was used to calculate electricity usage.

| Tonnes CO2e | 2024 | 2023 |

| Scope 2 | 17 | 18 |

| Scope 3 | 3 | 3 |

| Total | 20 | 21 |

| Intensity ratio (tonnes of CO2 per employee) | 0.9 | 1.0 |

The Group's electricity costs for 2024 were approximately £25,000 (2023: £30,000). The kWh usage in the year was 81,933 (2023: 87,780). The Group has no immediate plans to improve energy efficiency.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

For the year ended 31 December

| Note | 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Revenue | – | 381 | 699 | |

| Other income | 31 | 14 | 22 | |

| Research and development costs | (5,437) | (4,067) | (5,111) | |

| Administrative costs | (3,793) | (4,342) | (4,542) | |

| Loss from operations | (9,199) | (8,014) | (8,932) | |

| Finance income | 3 | 3,385 | 570 | 497 |

| Finance expense | 3 | (165) | (41) | (53) |

| Loss before tax | (5,979) | (7,485) | (8,488) | |

| Taxation | 4 | 250 | 406 | 832 |

| Loss for the year attributable to the owners of the parent | (5,729) | (7,079) | (7,656) | |

| Other comprehensive income: | ||||

| Items that will or may be reclassified subsequently to profit or loss: | ||||

| Total other comprehensive income net of tax | – | – | – | |

| Total comprehensive loss attributable to the owners of the parent | (5,729) | (7,079) | (7,656) | |

| Loss per share | ||||

| Continuing operations | ||||

| Basic and diluted loss per ordinary share - pence | 5 | (0.1)p | (2)p | (155) p |

The notes form an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

At 31 December

| Company number 09216368 | Note | 2024 £'000 | 2023 £'000 | 2022 £'000 |

| Assets | ||||

| Non-current assets | ||||

| Property, plant and equipment | 324 | 571 | 831 | |

| Intangible assets | 6 | 5,646 | 2,941 | 6 |

| 5,970 | 3,512 | 837 | ||

| Current assets | ||||

| Trade and other receivables | 6,568 | 637 | 1,006 | |

| Current taxation receivable | 573 | 422 | 846 | |

| Cash and cash equivalents | 1,669 | 5,971 | 2,836 | |

| 8,810 | 7,030 | 4,688 | ||

| Total assets | 14,780 | 10,542 | 5,525 | |

| Liabilities | ||||

| Non-current liabilities | ||||

| Deferred consideration | 7 | 1,306 | – | – |

| Borrowings | 8 | 118 | 295 | 463 |

| 1,424 | 295 | 463 | ||

| Current liabilities | ||||

| Trade and other payables | 3,504 | 1,240 | 1,447 | |

| Deferred consideration | 7 | 538 | – | – |

| Borrowings | 8 | 609 | 169 | 161 |

| Provisions | – | – | 207 | |

| Derivative financial liability | 9 | 383 | 4,160 | 85 |

| 5,034 | 5,569 | 1,900 | ||

| Total liabilities | 6,458 | 5,864 | 2,363 |

| CONSOLIDATED STATEMENTS OF FINANCIAL POSITION(CONTINUED) At 31 December | ||||

| Note | 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Issued capital and reserves attributable to owners of the parent | ||||

| Share capital | 10 | 11,725 | 6,253 | 1,108 |

| Share premium | 10 | 93,124 | 86,732 | 83,667 |

| Merger reserve | 10 | 53,003 | 53,003 | 53,003 |

| Warrant reserve | 10 | 894 | 3,457 | 720 |

| Accumulated deficit | 10 | (150,424) | (144,767) | (135,336) |

| Total equity | 8,322 | 4,678 | 3,162 | |

| Total equity and liabilities | 14,780 | 10,542 | 5,525 | |

The notes form an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS

For the year ended 31 December

| Note | 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Cash flows from operating activities | ||||

| Loss for the year | (5,729) | (7,079) | (7,656) | |

| Adjustments for: | ||||

| Depreciation of property, plant and equipment | 117 | 143 | 174 | |

| Depreciation of right of use asset | 135 | 137 | 166 | |

| Amortisation of intangible fixed assets | 6 | 2 | 3 | 3 |

| Loss/(Profit) on disposal of property, plant and equipment | 4 | 2 | 14 | |

| Impairment of loan | – | 79 | 207 | |

| Finance income | 3 | (3,385) | (570) | (497) |

| Finance expense | 3 | 165 | 41 | 53 |

| Share-based payment charge | 283 | 28 | 123 | |

| Taxation | 4 | (250) | (406) | (832) |

| Foreign exchange loss/(gains) | 4 | – | (1) | |

| Cash flows from operating activities before changes in working capital | (8,654) | (7,622) | (8,246) | |

| Decrease/(Increase) in trade and other receivables | (5,975) | 365 | 7 | |

| (Decrease)/Increase in trade and other payables | 2,239 | (207) | 356 | |

| (Decrease)/Increase in provisions | – | (207) | 157 | |

| Cash used in operations | (12,390) | (7,671) | (7,726) | |

| Taxes received | 4 | 129 | 845 | 678 |

| Net cash used in operating activities | (12,261) | (6,826) | (7,048) |

CONSOLIDATED STATEMENTS OF CASH FLOWS(CONTINUED)

For the year ended 31 December

| Note | 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Investing activities | ||||

| Purchases of property, plant and equipment | (9) | (26) | (62) | |

| Proceeds from disposal of fixed assets | – | 4 | 20 | |

| Purchase of intangible asset | 6 | (765) | (237) | – |

| Loan granted | – | (79) | (207) | |

| Interest received | 176 | 73 | 29 | |

| Net cash (used in)/generated from investing activities | (598) | (265) | (220) | |

| Financing activities | ||||

| Interest paid | – | (13) | (18) | |

| Amounts paid on lease liabilities | (186) | (188) | (178) | |

| Proceeds from promissory note | 8 | 431 | – | – |

| Share issues including warrants, net of costs | 8,312 | 10,427 | 243 | |

| Net cash generated from financing activities | 8,557 | 10,226 | 47 | |

| Net increase/(decrease) in cash and cash equivalents | (4,302) | 3,135 | (7,221) | |

| Cash and cash equivalents at beginning of year | 5,971 | 2,836 | 10,057 | |

| Exchange (losses)/gains on cash and cash equivalents | – | – | – | |

| Cash and cash equivalents at end of year | 1,669 | 5,971 | 2,836 |

The notes form an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

For the year ended 31 December

| Note | Share capital £'000 | Share premium £'000 | Merger reserve £'000 | Warrant reserve £'000 | Accumulated deficit £'000 | Total equity £'000 | |

| At 1 January 2024 | 6,253 | 86,732 | 53,003 | 3,457 | (144,767) | 4,678 | |

| Loss for the year | – | – | – | – | (5,729) | (5,729) | |

| Total comprehensive loss | – | – | – | – | (5,729) | (5,729) | |

| Transactions with owners | |||||||

| Shares issued on 22 May 2024 | 10 | 1,614 | 5,048 | – | – | – | 6,662 |

| Costs associated with share issue on 22 May 2024 | 10 | – | (487) | – | – | – | (487) |

| Shares issued on 22 July 2024 | 10 | 2,105 | 79 | – | 2 | – | 2,186 |

| Costs associated with share issue on 22 July 2024 | 10 | – | (55) | – | – | (297) | (352) |

| Exercise of warrants during the year | 10 | 1,602 | 1,739 | – | (2,565) | – | 776 |

| Issue of shares to purchase intangible asset | 11 | 151 | 68 | – | – | – | 219 |

| Share-based payment charge | – | – | – | – | 369 | 369 | |

| Total contribution by and distributions to owners | 5,472 | 6,392 | – | (2,563) | 72 | 9,373 | |

| At 31 December 2024 | 11,725 | 93,124 | 53,003 | 894 | (150,424) | 8,322 |

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY(CONTINUED)

| Note | Share capital £'000 | Share premium £'000 | Merger reserve £'000 | Warrant reserve £'000 | Accumulated deficit £'000 | Total equity £'000 | |

| At 1 January 2023 | 1,108 | 83,667 | 53,003 | 720 | (135,336) | 3,162 | |

| Loss for the year | – | – | – | – | (7,079) | (7,079) | |

| Total comprehensive loss | – | – | – | – | (7,079) | (7,079) | |

| Transactions with owners | |||||||

| Exercise of warrants on 22 March 2022 | 10 | – | – | – | – | – | – |

| Shares issued on 15 February 2023 | 10 | 1,956 | 3,013 | – | – | – | 4,969 |

| Costs associated with share issue on 15 February 2023 | 10 | – | (903) | – | – | – | (903) |

| Shares issued on 26 May 2023 | 10 | 2,380 | – | – | – | (355) | 2,025 |

| Costs associated with share issue on 26 May 2023 | 10 | – | – | – | – | (527) | (527) |

| Shares issued on 21 December 2023 | 10 | 485 | – | – | 1,315 | (1,273) | 527 |

| Costs associated with share issue on 21 December 2023 | 10 | – | – | – | – | (441) | (441) |

| Issue of shares to purchase intangible asset | 11 | 324 | 955 | – | 1,422 | – | 2,701 |

| Share-based payment charge | – | – | – | – | 244 | 244 | |

| Total contribution by and distributions to owners | 5,145 | 3,065 | – | 2,737 | (2,352) | 8,595 | |

| At 31 December 2023 | 6,253 | 86,732 | 53,003 | 3,457 | (144,767) | 4,678 |

NOTES FORMING PART OF THE FINANCIAL STATEMENTS

For the year ended 31 December 2024

1. Basis of preparation

The consolidated financial statements have been prepared in accordance with international accounting standards in conformity with the requirements of the Companies Act 2006, and they are prepared in accordance with international financial reporting standards. The consolidated financial statements have been prepared on a historical cost basis except that the following assets and liabilities are stated at their fair value: certain financial assets and financial liabilities measured at fair value, and liabilities for cash-settled share-based payments.

The financial information contained in this final announcement does not constitute statutory financial statements as defined in Section 435 of the Companies Act 2006. The financial information has been extracted from the financial statements for the year ended 31 December 2024 which have been approved by the Board of Directors, and the comparative figures for the year ended 31 December 2023 and 31 December 2022 are based on the financial statements for that year.

The financial statements for 2023 and 2022 have been delivered to the Registrar of Companies and the 2024 financial statements will be delivered after the Annual General Meeting.

The auditor's report for the Company's 2024 Annual Report and Accounts was unqualified but did draw attention to the material uncertainty relating to going concern. The auditor's report did not contain statements under s498(2) or (3) of the Companies Act 2006.

Whilst the financial information included in this results announcement has been prepared in accordance with International Financial Reporting Standards (IFRSs) this announcement does not itself contain sufficient information to comply with IFRSs. The information in this results announcement was approved by the board on 10 April 2025.

Going concern – material uncertainty

The Group and Company has experienced net losses and significant cash outflows from cash used in operating activities over the past years as it develops its portfolio. For the year ended 31 December 2024, the Group incurred a consolidated loss for the year of £5.73 million and negative cash flows from operations of £12.26 million. As of 31 December 2024, the Group had an accumulated deficit of £150.42 million.

The Group's future viability is dependent on its ability to raise cash from financing activities to finance its development plans until milestones and/or royalties can be secured from partnering the Company's assets. The Group's failure to raise capital as and when needed could have a negative impact on its financial condition and ability to pursue its business strategies.

The Directors believe there are adequate options and time available to secure additional financing for the Company and after considering the uncertainties, the Directors consider it is appropriate to continue to adopt the going concern basis in preparing these financial statements. The Group's consolidated financial statements have therefore been presented on a going concern basis, which contemplates the realisation of assets and the satisfaction of liabilities in the normal course of business.

As at 31 December 2024, the Group had cash and cash equivalents of £1.67 million. The Directors have prepared cash flow forecasts and considered the cash flow requirement for the Group for the next three years including the period 12 months from the date of approval of the consolidated financial statements. These forecasts show that further financing will be required before Q4 2025 assuming, inter alia, that certain development programs and other operating activities continue as currently planned. Pursuant to its $35 million Equity Line of Credit, or ELOC, as described in the Finance Review, the Company may direct C/M to purchase ADSs (subject to certain limitations) and receive proceeds in accordance with a formula price for up to 36 months from the Commencement Date. There is no guarantee that the Company will be able to use the ELOC to the extent necessary to finance the Company's operations.

In the Directors' opinion, the environment for financing of small and micro-cap biotech companies remains challenging. While this may present acquisition and/or merger opportunities with other companies with limited or no access to financing, as noted above, any attendant financings by Biodexa are likely to be dilutive. The Directors continue to evaluate financing options, including those connected to acquisitions and/or mergers, potentially available to the Group. Any alternatives considered are contingent upon the agreement of counterparties and accordingly, there can be no assurance that any alternative courses of action to finance the Company would be successful.

This requirement for additional financing in the short term represents a material uncertainty that may cast significant doubt upon the Group and Parent Company's ability to continue as a going concern. Should it become evident in the future that there are no realistic financing options available to the Company which are actionable before its cash resources run out then the Company will no longer be a going concern. In such circumstances, we would no longer be able to prepare financial statements under paragraph 25 of IAS 1. Instead, the financial statements would be prepared on a liquidation basis and assets would be stated at net realizable value and all liabilities would be accelerated to current liabilities.

2. Accounting for eRapa and CPRIT grant

On 25 April 2024 the Company entered into a License and Collaboration Agreement (LCA) with Rapamycin Holdings, Inc. (d/b/a Emtora Biosciences). The LCA entered into with Emtora meets the definition of a Joint Arrangement under IFRS 11, specifically related to the FAP program.

A jointly controlled escrow account was established on completion of the LCA. All FAP program transactions are processed through the escrow account, including the Company's deposits of matching funds, as set out in the agreement, the receipt of grant funding from CPRIT and the payment of eligible R&D expenses. Although the CPRIT grant and R&D supplier contracts are with Emtora, the joint arrangement nature of the LCA results in Emtora being deemed to be acting as the Company's agent. Accordingly, the Company recognises 100% of the grant and 100% of the R&D expenditure. The CPRIT grant recognised is on a 1 for 2 match over the period of the grant, but can vary between periods. In accordance with the Company's accounting policy, the grant, as it is the re-imbursement of directly related costs, is credited to R&D costs in the same period in the Statements of Comprehensive Income. The escrow account is recognised within prepayments, CPRIT grant received in advance is recognised within deferred revenue and any grant not yet received is recognised in accrued income.

In 2024 the Company recognised R&D costs of £1.24 million on the FAP project, this was made up of expenditure of £2.45 million netted against CPRIT grant income of £1.21 million.

The balances as at 31 December 2024 were as follows in relation to the FAP project:

Prepayments £6.11 million

Deferred revenue £1.47 million

3. Finance income and expense

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Finance income | |||

| Interest received on bank deposits | 166 | 73 | 29 |

| Other interest receivable | 1 | 10 | – |

| Gain on equity settled derivative financial liability | 3,218 | 487 | 468 |

| Total finance income | 3,385 | 570 | 497 |

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Finance expense | |||

| Interest expense on lease liabilities | 19 | 28 | 43 |

| Interest expense on deferred consideration | 144 | – | – |

| Other loans | 2 | 13 | 10 |

| Total finance expense | 165 | 41 | 53 |

The gain on the equity settled derivative financial liability in 2024, 2023 and 2022 arose as a result of the movement in share price.

4. Taxation

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Current tax credit | |||

| Current tax credited to the income statement | 241 | 407 | 825 |

| Adjustment in respect of prior year | 9 | (1) | 7 |

| 250 | 406 | 832 | |

| Deferred tax credit | |||

| Reversal of temporary differences | – | – | – |

| Total tax credit | 250 | 406 | 832 |

The reasons for the difference between the actual tax credit for the year and the standard rate of corporation tax in the United Kingdom applied to losses for the year are as follows:

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Loss before tax | (5,979) | (7,485) | (8,488) |

| Expected tax credit based on the standard rate of United Kingdom corporation tax at the domestic rate of 25% (2023: 25.52%; 2022: 19%) | (1,495) | (1,764) | (1,613) |

| Expenses not deductible for tax purposes | 1,069 | 408 | 392 |

| Income not taxable | (809) | (5) | (4) |

| Adjustment in respect of prior period | (9) | 1 | (7) |

| Effect of R&D relief | 100 | 26 | (357) |

| Deferred tax not recognised | 894 | 928 | 757 |

| Total tax credited to the income statement | (250) | (406) | (832) |

The taxation credit arises on the enhanced research and development tax credits accrued for the respective periods.

5. Loss per share

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Numerator | |||

| Loss used in basic EPS and diluted EPS: | |||

| Continuing operations | (5,729) | (7,079) | (7,656) |

| Denominator | |||

| Weighted average number of ordinary shares used in basic EPS: | 4,952,784,179 | 315,849,600 | 4,941,793 |

| Basic and diluted loss per share: | |||

| Continuing operations – pence | (0.1)p | (2)p | (155) p |

At a General Meeting on 22 November 2024, shareholders approved the subdivision and redesignation of the Company's Issued Ordinary Shares of £0.001 each into to one Ordinary Share of £0.00005 each and 19 ‘C' Deferred Shares of £0.00005 each. The ‘B' Deferred Shares have limited rights and are effectively valueless. The share sub-division and redesignation did not impact the calculation of the denominator as the number of Issued Ordinary Shares did not change.

During the year the Company issued warrants that were accounted through the Warrant Reserve as detailed in note 10.

The Company has considered the guidance set out in IAS 33 in calculating the denominator in connection with the issuance of Pre-Funded warrants and abeyance shares as disclosed in note 10. Management have recognised the warrants from the date of grant rather than the date of issue of the corresponding Ordinary Shares when calculating the denominator.

The Group has made a loss in the current and previous periods presented, and therefore the options and warrants are anti-dilutive. As a result, diluted loss per share is presented on the same basis as basic loss per share.

6. Intangible Assets

| In-process research and development £'000 | Goodwill £'000 | IT/Website costs £'000 | Total £'000 | |

| Cost | ||||

| At 1 January 2022 | 13,378 | 2,291 | – | 15,669 |

| Transfer from property, plant and equipment | – | – | 122 | 122 |

| Disposal | – | – | (12) | (12) |

| At 31 December 2022 | 13,378 | 2,291 | 110 | 15,779 |

| Acquisition | 2,938 | – | – | 2,938 |

| At 31 December 2023 | 16,316 | 2,291 | 110 | 18,717 |

| Acquisition | 2,707 | – | – | 2,707 |

| Disposals | – | – | (22) | (22) |

| At 31 December 2024 | 19,023 | 2,291 | 88 | 21,402 |

| In-process research and development £'000 | Goodwill £'000 | IT/Website Costs £'000 | Total £'000 | |

| Accumulated amortisation and impairment | ||||

| At 1 January 2022 | 13,378 | 2,291 | – | 15,669 |

| Amortisation charge for the year | – | – | 3 | 3 |

| Transfer from property, plant and equipment | – | – | 113 | 113 |

| Disposal | – | – | (12) | (12) |

| At 31 December 2022 | 13,378 | 2,291 | 104 | 15,773 |

| Amortisation charge for the year | – | – | 3 | 3 |

| Disposal | – | – | – | – |

| At 31 December 2023 | 13,378 | 2,291 | 107 | 15,776 |

| Amortisation charge for the year | – | – | 2 | 2 |

| Disposal | – | – | (22) | (22) |

| At 31 December 2024 | 13,378 | 2,291 | 87 | 15,756 |

| Net book value | ||||

| At 31 December 2024 | 5,645 | – | 1 | 5,646 |

| At 31 December 2023 | 2,938 | – | 3 | 2,941 |

| At 31 December 2022 | – | – | 6 | 6 |

The individual intangible asset which is material to the financial statements is as follows:

| Carrying amount | Remaining amortisation period | |||||

| 2024 £'000 | 2023 £'000 | 2022 £'000 | 2024 (years) | 2023 (years) | 2022 (years) | |

| MTX228 tolimidone acquired IPRD* | 2,938 | 2,938 | –_ | n/a | n/a | n/a |

| MTX230 eRapa acquired IPRD* | 2,707 | – | – | n/a | n/a | n/a |

*asset is not yet in use and has not started amortising

On 25 April 2024 the Company entered into a LCA with Emtora, relating to the license of eRapa. In consideration for the License, the Company made an upfront payment of 15,1261 ADSs (equal to five percent of our then outstanding Ordinary Shares, calculated on a fully-diluted basis). In addition, a promissory note previously issued by Emtora in favour of the Company in the amount of $0.25 million was forgiven and certain historical liabilities relating to their on-going FAP and NMIBC programs were settled. The Company is also obligated to make quarterly payments to Emtora of $0.25 million less 75% of any research sales by Emtora until the handover trigger event occurs. The obligation meets the definition of a financial liability in accordance with IAS32 and is measured at fair value in accordance with IFRS9. Management have estimated the expected liability to be $3.1 million and the present value as $2.5 million.

| $'000 | £'000 | |

| 15,1261 ADSs issued at market value | 274 | 219 |

| Promissory note forgiven | 250 | 197 |

| Historical liabilities settled | 366 | 294 |

| Quarterly payment obligation | 2,494 | 1,997 |

| Recognised as intangible asset purchase | 3,384 | 2,707 |

In addition, the Company is also responsible for up to $31.5 million in sales milestones within the first six months of commercial sale of a first-approved indication of eRapa in certain markets, with decreasing milestones for subsequent approvals for additional indications. There is also a one-time $10.0 million milestone payable upon cumulative net sales of $1.0 billion. Further, the Company is also obligated to pay Emtora single digit tiered royalties on net sales of eRapa, in addition to honouring Emtora's legacy royalty obligations and paying Emtora fees related to income derived from sublicensing and partnering of eRapa.

The LCA also provides the Company with the exclusive option to acquire all of the capital stock of Emtora on commercially reasonable terms in the 90 days after acceptance of the filing of an NDA by the U.S. Food and Drug Administration (the "FDA"). If the Company does not exercise the option, it would be required to make additional quarterly payments until the first commercial sale of the product.

1 Number of ADSs have been adjusted to reflect the ADS ratio change on 4 October 2024

7. Deferred Consideration

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Current | |||

| Opening provision at 1 January | – | – | – |

| On acquisition of licence | 1,997 | – | – |

| Payments | (274) | – | – |

| Interest expense | 144 | – | – |

| Foreign exchange | (23) | – | – |

| 1,844 | – | – | |

| Less: non-current portion | 1,306 | – | – |

| Current portion | 538 | – | – |

The Company is obligated to make quarterly payments to Emtora of $0.25 million less 75% of any research sales by Emtora until the handover trigger event occurs. The obligation meets the definition of a financial liability in accordance with IAS32 and is measured at fair value in accordance with IFRS9. Management have estimated the expected liability to be $3.1 million and the present value as $2.5 million.

This financial liability is measured on Level 3, the fair value is derived using a discounted cash flow approach. The discount rate applied to the obligation was 11.64% (2023: n/a).

A 1% increase or decrease in the discount rate would decrease or increase the liability by approximately £0.03 million (2023: n/a) and £0.03 million (2023: n/a), respectively. An increase in the liability would result in a loss in the revaluation of financial instruments, while a decrease would result in a gain.

There were no transfers between Level 1 and 2 in the period.

8. Borrowings

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Current | |||

| Promissory note | 430 | – | – |

| Lease liabilities | 179 | 169 | 161 |

| Total | 609 | 169 | 161 |

| Non-current | |||

| Lease liabilities | 118 | 295 | 463 |

| Total | 118 | 295 | 463 |

Book values approximate to fair value at 31 December 2024, 2023 and 2022.

Promissory note

In December 2024 the Company issued a Promissory Note to C/M Capital Master Fund, LP in the aggregate principal amount of $600,000 at a 10% original issue discount. The Note is an unsecured obligation of the Company and bears interest at an annual rate of 5%, which may be increased under certain circumstances, and has a maturity date of one year from the Issuance Date. The Note includes a monthly repayment schedule, with the entire principal amount of the Note, plus accrued and unpaid interest, due and payable by the Company on the date that is twelve months from the Issuance Date. The Note may be prepaid prior to the Maturity Date without penalty. Additionally, prior to the Maturity Date and while the Note remains outstanding, upon the occurrence of each and every bona fide transaction or series of transactions conducted by the Company wherein the principal purpose of the Company is to raise capital, pursuant to which the Company issues and sells securities for an amount of gross proceeds equal to or greater than $500,000, the Company shall be obligated to utilize 25% of the gross proceeds from such Financing Event to prepay the Note, which repayment shall be due concurrently or immediately following the closing of such Financing Event.

The Company received $540,000 pursuant to the Promissory Note on 24 December 2024.

9. Derivative financial liability – current

| 2024 £'000 | 2023 £'000 | 2022 £'000 | |

| Equity settled derivative financial liability | |||

| At 1 January | 4,160 | 85 | 553 |

| Warrants issued | 3,059 | 4,562 | – |

| Transfer to share premium on exercise of warrants | (3,618) | – | – |

| Gain recognised in finance (income)/expense within the consolidated statement of comprehensive income | (3,218) | (487) | (468) |

| At 31 December | 383 | 4,160 | 85 |

Equity settled derivative financial liability is a liability that is not to be settled for cash.

The Company issues warrants in the ADSs of the Company as part of registered direct offerings and private placements in the US. The number of ADSs to be issued when exercised is fixed, however the exercise price is denominated in US Dollars being different to the functional currency of the Company. Therefore, the warrants are classified as equity settled derivative financial liabilities recognised at fair value through the profit and loss account (‘FVTPL'). The financial liability is valued using the Black-Scholes model in 2024 and 2023, in previous periods the Monte Carlo model was used. The change in methodology is as result of the Company de-listing from AIM in 2023 and no longer needing to consider foreign exchange movements in the fair value calculation. Financial liabilities at FVTPL are stated at fair value, with any gains or losses arising on re-measurement recognised in profit or loss. The net gain or loss recognised in profit or loss incorporates any interest paid on the financial liability and is included in the ‘finance income' or ‘finance expense' lines item in the income statement. A key input in the valuation of the instrument is the Company share price.

Details of the warrants are as follows:

July 2024 warrants

In July 2024 the Company issued 213,188 Series J ADS Warrants and 213,188 Series K warrants as part of the Registered Direct Offering and Concurrent Private Placement in the US.

May 2024 warrants

In May 2024 the Company issued 94,358 Series G ADS Warrants and 147,805 Series H warrants as part of the Warrant Inducement in the US.

December 2023 warrants

In December 2023 the Company issued 119,998 Series E ADS Warrants and 119,996 Series F ADS Warrants as part of the Registered Offering in the US. The Series F warrants expired on 23 December 2024.

May 2023 warrants

In June 2023 the Company issued 11,059 Series D ADS Warrants as part of a registered direct offering and private placement in the US after securing shareholder approval.

May 2020 warrants

In May 2020 the Company issued 30 ADS warrants as part of a registered direct offering in the US.

October 2019 warrants

In October 2019 the Company issued 15 ADS warrants as part of a registered direct offering in the US.

Warrant re-price

On 22 July 2024 the Company agreed to reduce the exercise price of the Company's existing Series E warrants, Series G warrants and Series H warrants held by those investors who participated in the Registered Direct Offering and Concurrent Private Placement to $25.00 per ADS.

*Number and original price of warrants have been adjusted to reflect the share consolidation and ratio change of ADS's to ordinary shares that occurred on 24 March 2023 and the ratio change of ADS's to ordinary shares on 26 September 2022, 5 July 2023 and 4 October 2024.

DARA warrants and share options

The Group also assumed fully vested warrants and share options on the acquisition of DARA Biosciences, Inc. (which took place in 2015). The number of ordinary shares to be issued when exercised is fixed, however the exercise prices are denominated in US Dollars. The warrants are classified equity settled derivative financial liabilities and accounted for in the same way as those detailed above. The financial liability is valued using the Black-Scholes option pricing model. The exercise price of the outstanding options is $8,771,300.00.

The following table details the outstanding warrants over ADSs and ordinary shares as at 31 December and also the movement in the year:

| At 1 January 2022 | Lapsed | At 31 December 2022 | Lapsed | Granted | At 31 December 2023 | Lapsed | Granted | Exercised | At 31 December 2024 | |

| ADSs | ||||||||||

| July 2024 grant | – | – | – | – | – | – | – | 426,376 | – | 426,376 |

| May 2024 grant | – | – | – | – | – | – | – | 242,163 | – | 242,163 |

| December 2023 grant | – | – | – | – | 239,994 | 239,994 | (16,027) | (171,309) | 52,658 | |

| May 2023 grant | – | – | – | – | 11,059 | 11,059 | – | – | – | 11,059 |

| May 2020 grant | 30 | – | 30 | – | – | 30 | – | – | – | 30 |

| October 2019 grant | 15 | – | 15 | – | – | 15 | – | – | – | 15 |

| Ordinary shares | ||||||||||

| Dara warrants | 204 | (204) | – | – | – | – | – | – | – | – |

| Dara options | 138 | – | 138 | (10) | – | 128 | (29) | – | – | 99 |

*Number and original price of warrants have been adjusted to reflect the share consolidation and ratio change of ADS's to ordinary shares that occurred on 24 March 2023 and the ratio change of ADS's to ordinary shares on 26 September 2022, 5 July 2023 and 4 October 2024.

10. Share capital and reserves

| Authorised, allotted and fully paid – classified as equity | 2024 Number | 2024 £ | 2023 Number | 2023 £ | 2022 Number | 2022 £ |

| At 31 December | ||||||

| Ordinary shares of £0.00005 each | 6,685,918,922 | 334,296 | 1,189,577,722 | 1,189,578 | 5,417,137 | 108,343 |

| ‘A' Deferred shares of £1 each | 1,000,001 | 1,000,001 | 1,000,001 | 1,000,001 | 1,000,001 | 1,000,001 |

| ‘B' Deferred shares of £0.001 each | 4,063,321,418 | 4,063,321 | 4,063,321,418 | 4,063,321 | – | – |

| ‘C' Deferred shares of £0.00005 each | 126,547,389,518 | 6,327,370 | – | – | – | – |

| Total | 11,724,988 | 6,252,900 | 1,108,344 |