TSMC, Samsung Lead Recovery In Asia's Emerging Markets With AI And Chip Sector Growth

Following deep losses in 2022, many emerging market assets were at bargain valuations and the recovery began in late 2022, driven by tech stocks such as Taiwan Semiconductor Manufacturing Co (NYSE:TSM) and Samsung Electronics Co (OTC:SSNLF).

Emerging market equities — particularly in the manufactured goods sectors — are deeply tied to the cyclical performance of the U.S. economy, relying on exports to the world’s biggest consumer market.

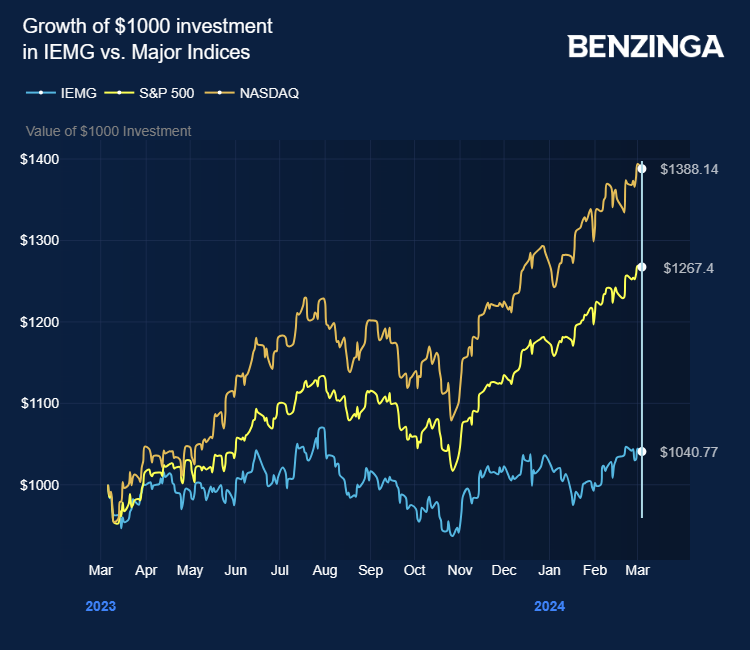

The iShares Core MSCI Emerging Markets ETF (NYSE:IEMG), an exchange traded fund that includes both TSMC and Samsung among its top holdings, hit a record-high close of $70 in February 2021 as the clamor for new tech from COVID-19 lockdown-restricted U.S. consumers drove domestic shares of both companies to all-time highs.

But, as the Federal Reserve embarked on its rate hike cycle in 2022 — that would eventually see U.S. rates hit 5.25-5.5% in mid 2023 — EM equity markets collapsed.

The IEMG ETF slumped 41% from its 2021 peak to an October 2022 trough of $41.44.

At this point, many emerging markets were seen as poisonous to investors. Growing trade tensions between the U.S. and China saw once-popular Chinese-listed stocks such as Alibaba Group Holdings (NYSE:BABA) and Tencent Holdings (OTC:TCEHY) tumble even further.

Also Read: Microsoft’s GenAI Advantage Is ‘Distancing It From The Competition,’ Says Analyst

Tech-Driven Recovery

But by October 2022, growing supply chain problems that limited exports of key supplies of semiconductors and other Asia-manufactured parts and goods drove a revival in emerging markets.

Wedded to this was the vast growth in artificial intelligence research and development that drove the U.S.-listed Magnificent Seven stocks such as Microsoft Corporation and Nvidia Corporation to new highs through 2023.

“All of this occurred despite the largest increase of interest rates in decades, wars in Ukraine and the Middle East, high energy prices, a regional banking crisis, and a recession in parts of the eurozone,” said analysts at Lazard Asset Management.

But, unlike in the U.S., where stock indices and the ETFs that track them, recovered to new record highs in 2023, emerging markets losses of 2022 have yet to rebound.

“We believe emerging markets remain one of the most mispriced asset classes globally,” Lazard said.

Its analysts added: “While absolute valuation levels have moved higher since they bottomed in the fourth quarter of 2022, relative to developed market equities, valuations remain generally inexpensive.

“Valuation discounts relative to developed markets and U.S. equities are hovering near 30% and 40%, respectively.”

Even as concerns mount that the valuations of some of the U.S. mega-cap stocks are becoming stretched, investors continue to gravitate towards them. Thus, if a U.S. market correction should occur in 2024, emerging market valuation discounts could present investors with alternatives.

Since its October 2024 trough, the IEMG ETF has regained 22.6% to $50.80.

Mitigating China Risk

While China remains a risk, its government has pledged support for its ailing markets, which saw the Shanghai Composite index drop 20% between May 2023 and February 2024. Since the February low, the index has recovered 12.8%.

Further news on these measures could come at this week’s National People’s Congress, China’s flagship annual political event, where the Communist party is expected to outline how it plans to deal with its geopolitical and economic challenges, including its ongoing real estate crisis.

If investors don’t like the China exposure in the IEMG ETF — which is minimal — iShares offers the MSCI Emerging Markets Ex-China ETF (NYSE:EMXC), which strips out Chinese-listed stocks, and has climbed 30% since its October 2022 low.

Photo: Shutterstock